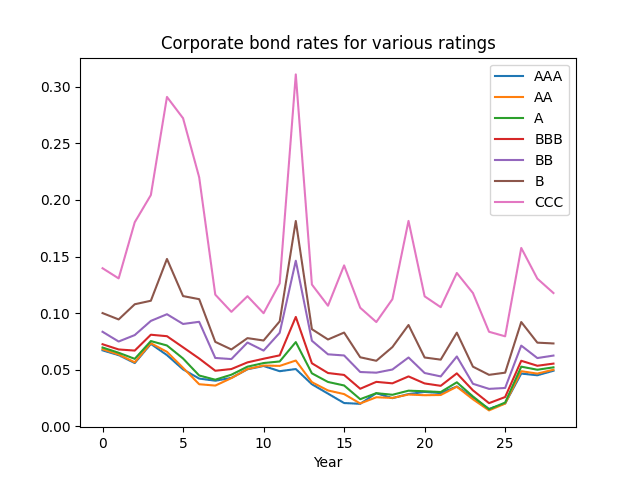

A continuation of research in github.com/asarantsev repository Annual-Bank-of-America-Rated-Bond-Data from my previous post. Consider total returns

If these were Treasury bonds and there were no risk of default, and if these were zero-coupon bonds (with only principal payment at maturity) then total returns would be equal to the rate minus maturity times rate change. See my manuscript arXiv:2411.03699. The equation is:

The maturity is given in the following table, together with analysis of residuals: skewness, kurtosis, Shapiro-Wilk and Jarque-Bera normality test

| Rating |  | Skewness | Kurtosis | Shapiro-Wilk | Jarque-Bera | ACF of  | ACF of  |

| AAA | 6.03 | -2.049 | 5.173 | 0.014% | <0.001% | 0.539 | 0.687 |

| AA | 4.89 | -0.941 | 1.154 | 2.549% | 5.831% | 0.944 | 0.874 |

| A | 4.94 | -0.894 | 1.307 | 7.877% | 5.726% | 0.977 | 0.704 |

| BBB | 5.17 | -0.573 | 0.027 | 25% | 46% | 0.38 | 0.604 |

| BB | 3.81 | -1.75 | 3.64 | 0.054% | <0.001% | 0.83 | 0.245 |

| B | 3.12 | -2.036 | 4.323 | 0.003% | <0.001% | 1.17 | 0.653 |

| CCC | 2.55 | -2.304 | 5.34 | 0.001% | <0.001% | 0.9 | 0.716 |

The autocorrelation function plots for

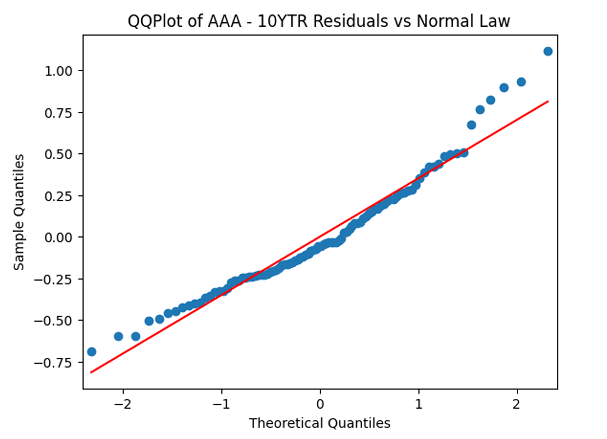

This is confirmed by the results of Shapiro-Wilk and Jarque-Bera tests, shown in the table above.

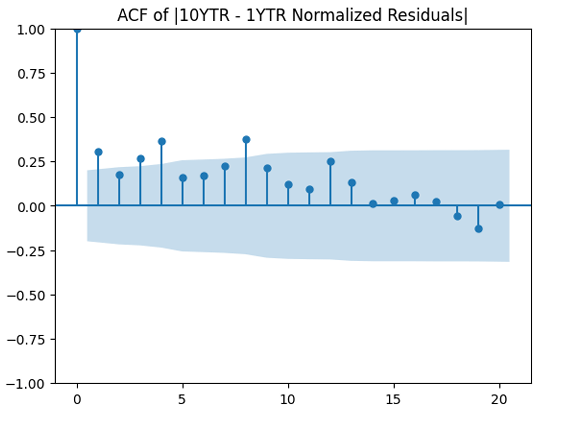

Apply the same technique as in the previous post: Normalize residuals by dividing them by annual average VIX. We get:

Coefficient estimates and analysis of innovations

| Rating |  | |  | Skewness | Kurtosis | Shapiro-Wilk | Jarque-Bera | ACF of | ACF of |

| AAA | 0.0661 | 7.0787 | -0.0034 | -0.737 | 0.576 | 28% | 23% | 0.922 | 0.361 |

| AA | 0.0453 | 5.3226 | -0.0023 | 0.126 | -0.039 | 46% | 96% | 0.57 | 0.761 |

| A | 0.0423 | 5.3423 | -0.0022 | -0.181 | 0.02 | 35% | 93% | 0.73 | 0.459 |

| BBB | 0.0293 | 5.6074 | -0.0016 | -0.232 | -0.775 | 67% | 62% | 0.875 | 0.498 |

| BB | 0.0422 | 3.6671 | -0.0024 | -0.894 | 1.426 | 19% | 6.3% | 0.574 | 0.888 |

| B | 0.0682 | 2.9970 | -0.0050 | -1.562 | 3.479 | 0.397% | <0.001% | 0.998 | 0.354 |

| CCC | 0.0712 | 2.6532 | -0.0075 | -1.588 | 2.649 | 0.072% | 0.005% | 0.835 | 0.723 |

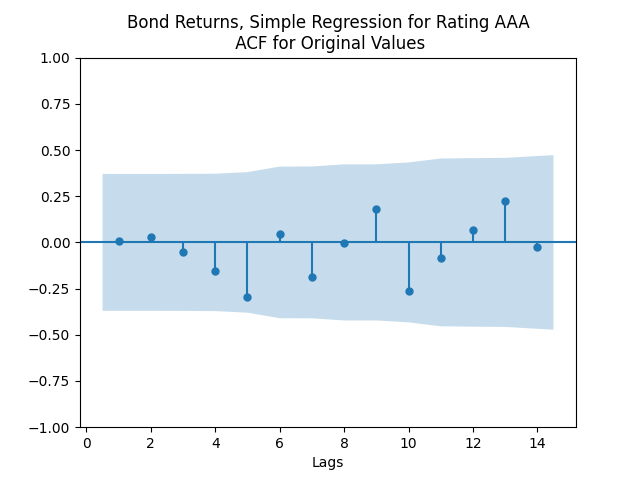

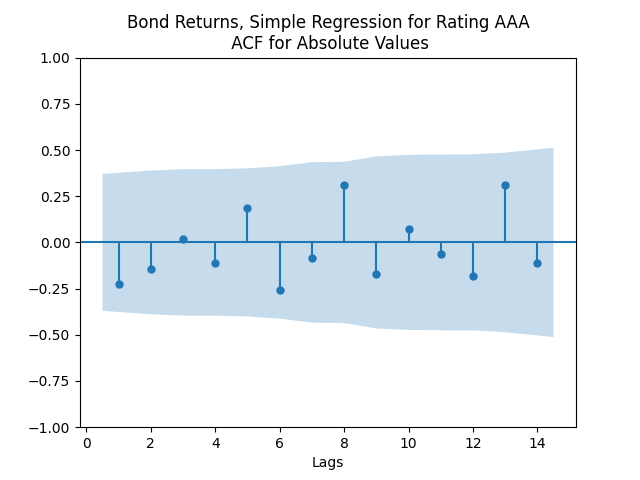

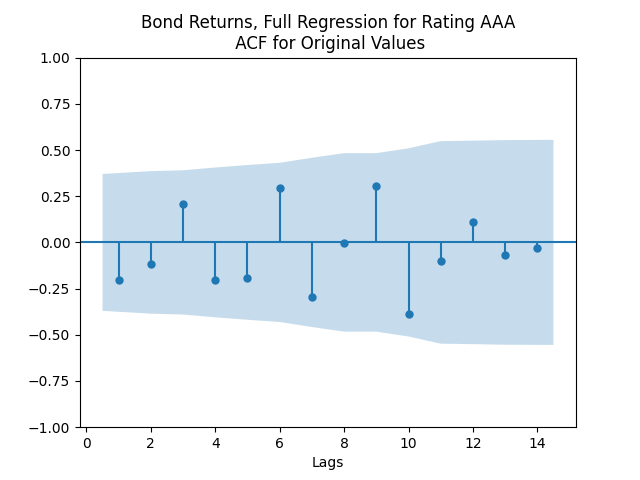

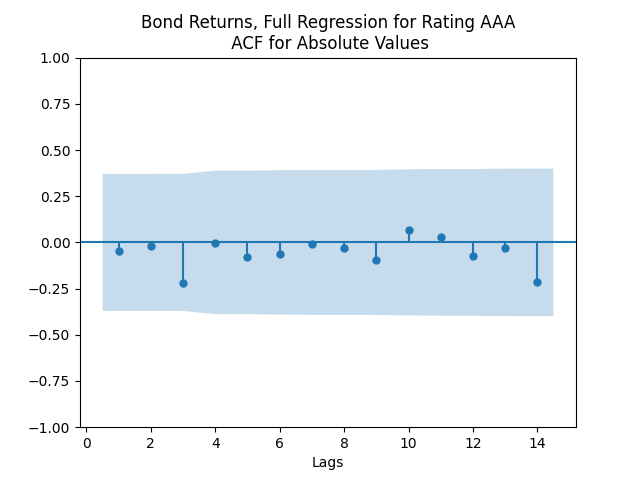

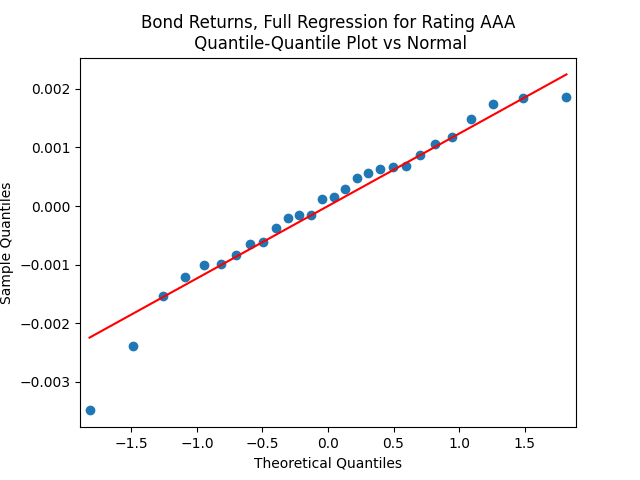

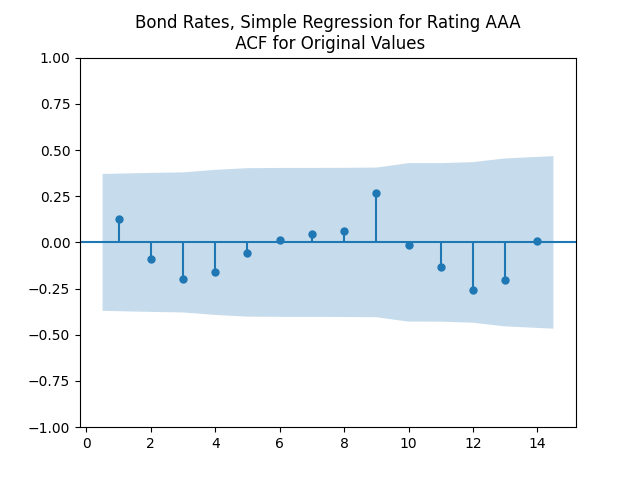

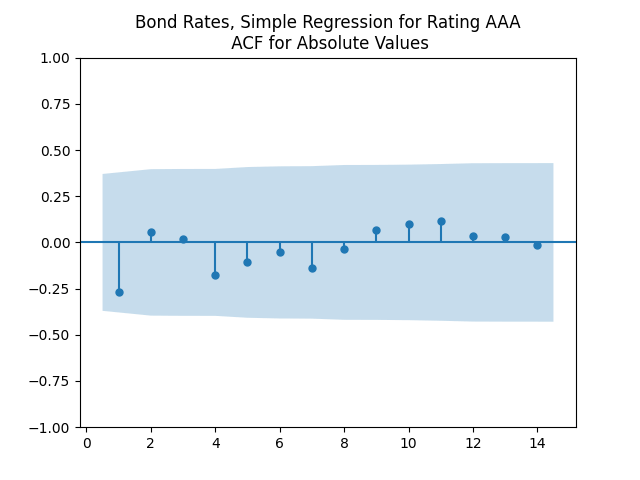

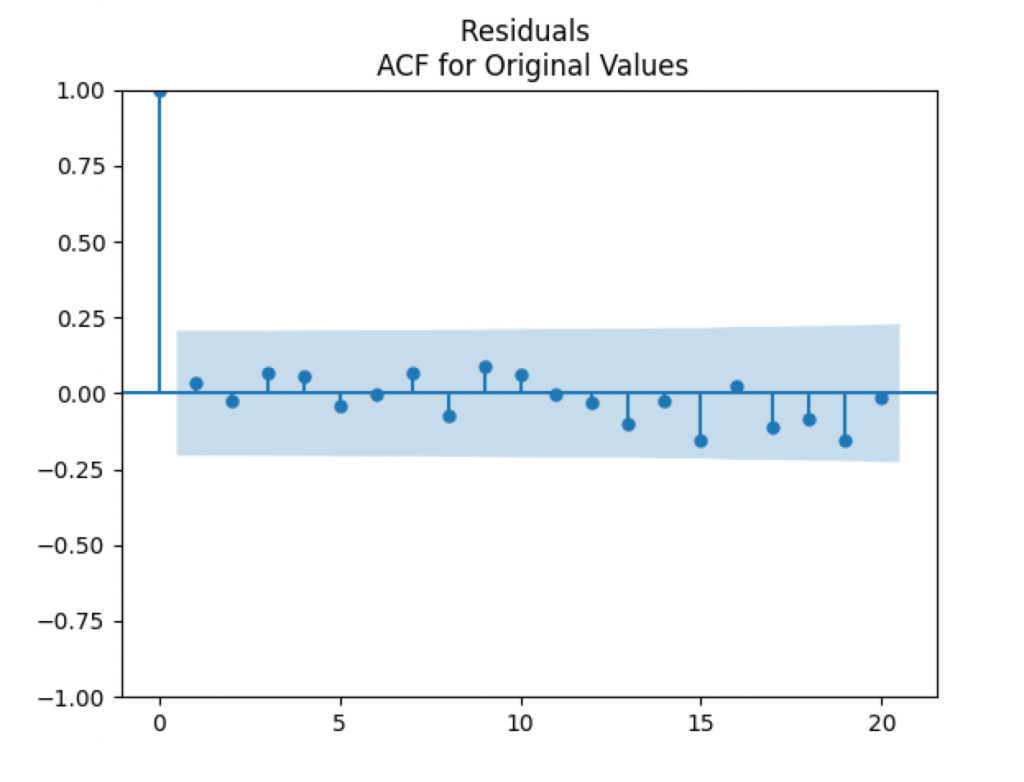

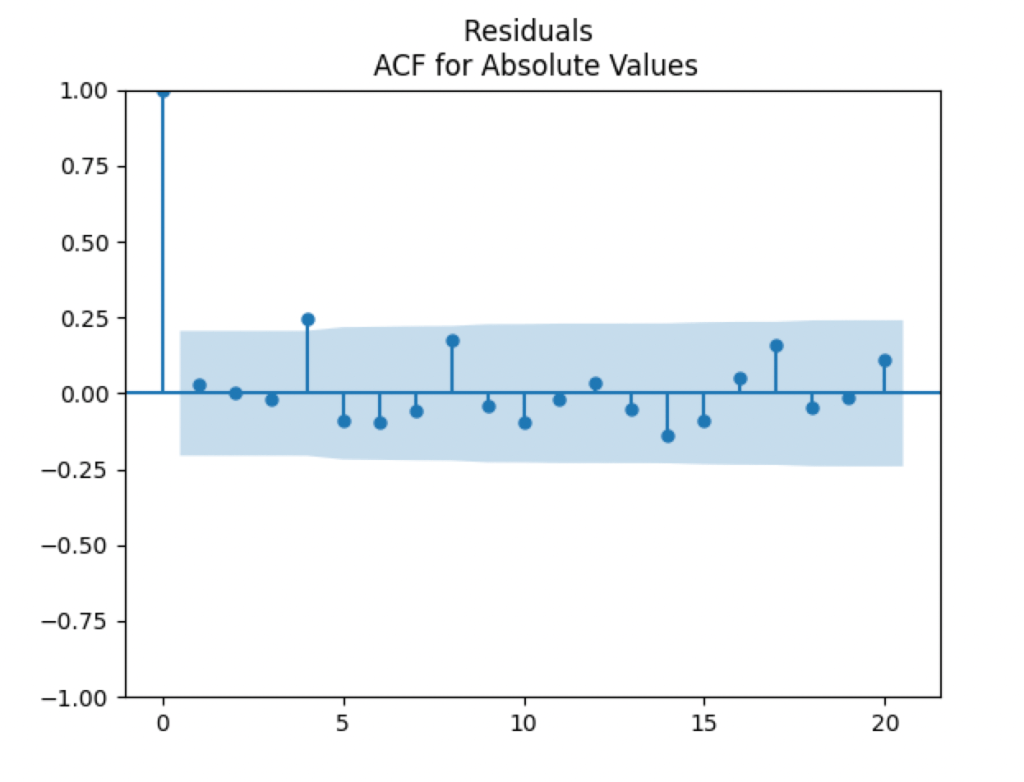

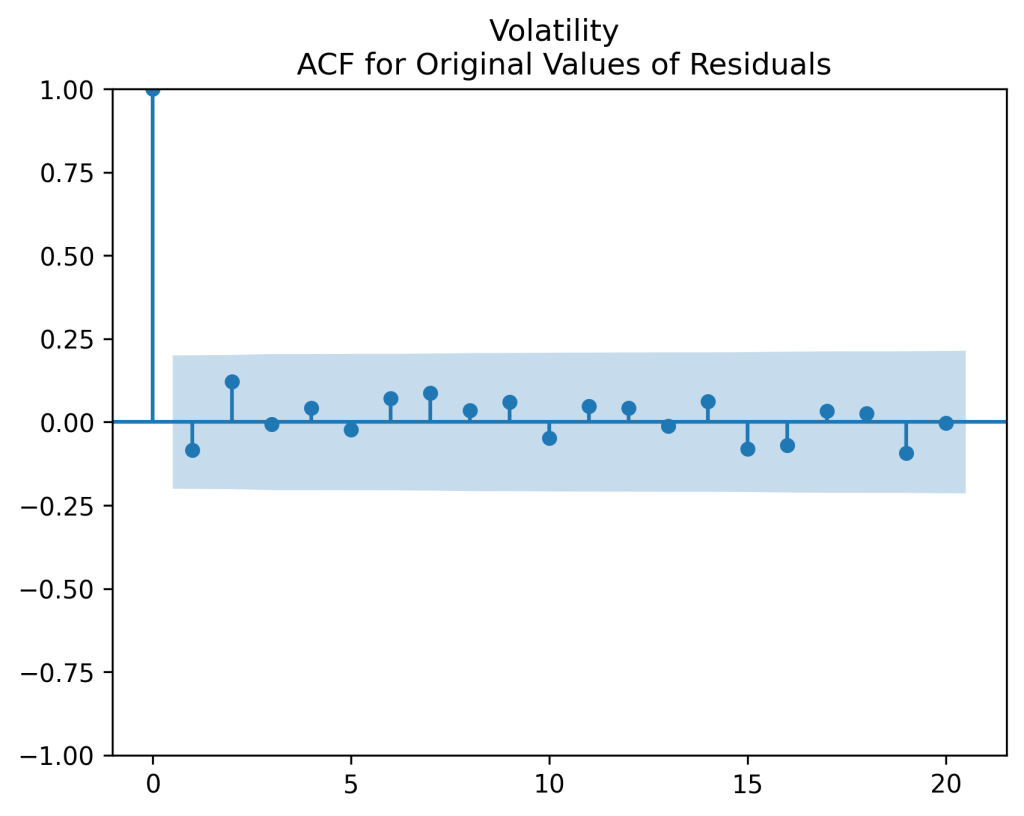

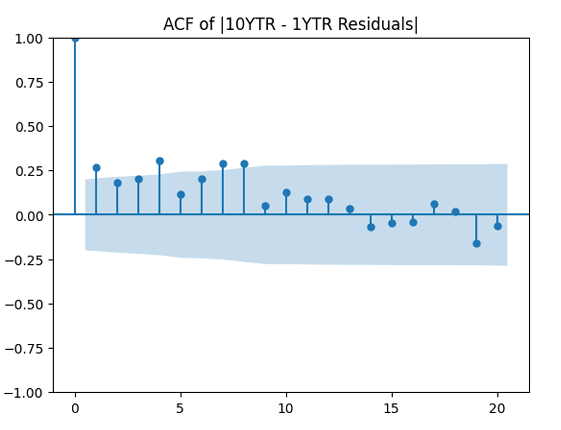

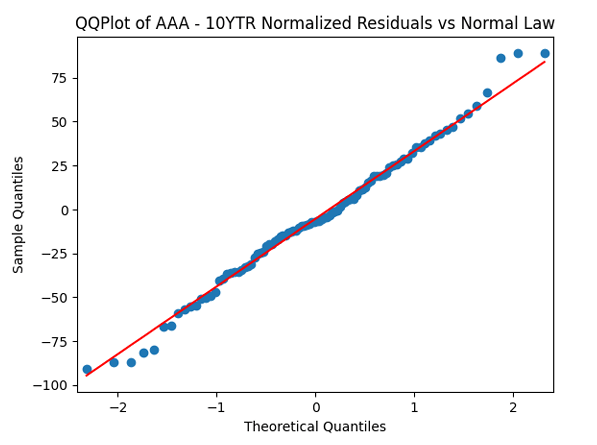

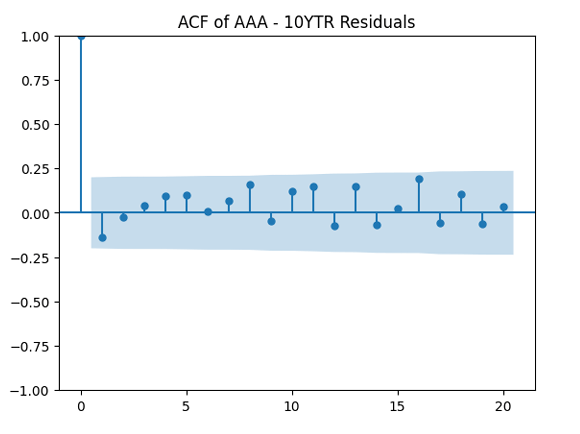

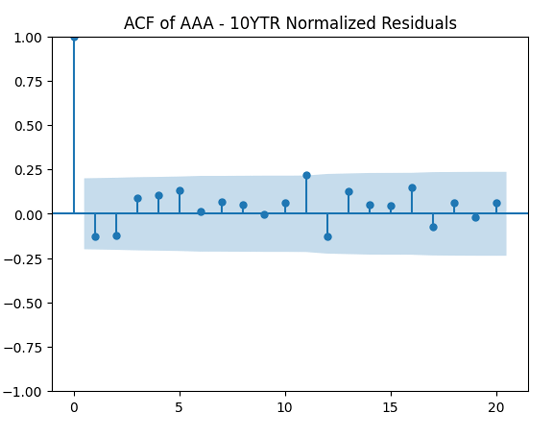

We see the residuals can be well described as Gaussian white noise for ratings BB and higher, especially well for investment-grade bonds. But for B and CCC ratings, not so much. However, judging by the ACF, new residuals (see the second table) are comparable to old residuals (see the first table) in being close to independent identically distributed. See also the following plots for AAA rated bonds:

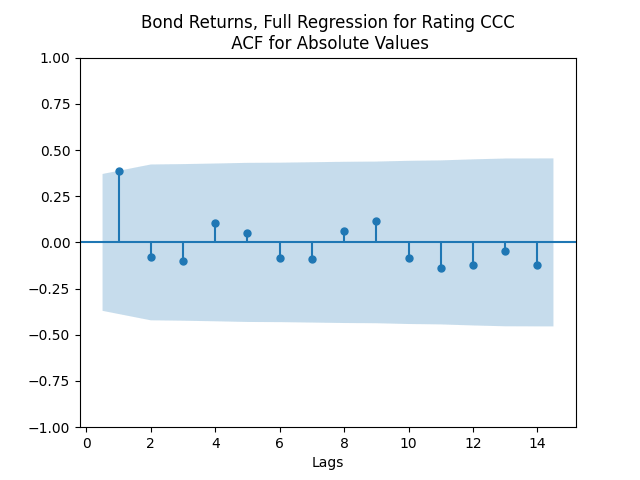

And for the lowest-rated CCC bonds the situation is different: We see that the first lag is quite significant for both version of the autocorrelation function.

Combining the model above with the results of the previous post, we get the trivariate model:

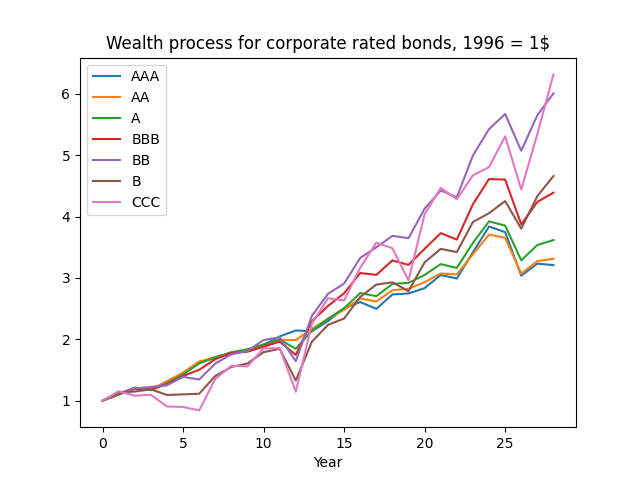

And the wealth process is given by

Next, for ratings BB and above, the trivariate innovations sequence

be this rate at end of year

be this rate at end of year  Model as an autoregression:

Model as an autoregression:

shows that this is well explained by independent identically distributed random variables (white noise). But these are not necessarily normal, judging by the Shapiro-Wilk and Jarque-Bera normality tests. Especially for junk-rated bonds (BB, B, CCC) but also sometimes for investment-grade bonds. The random walk hypothesis could be rejected (using low

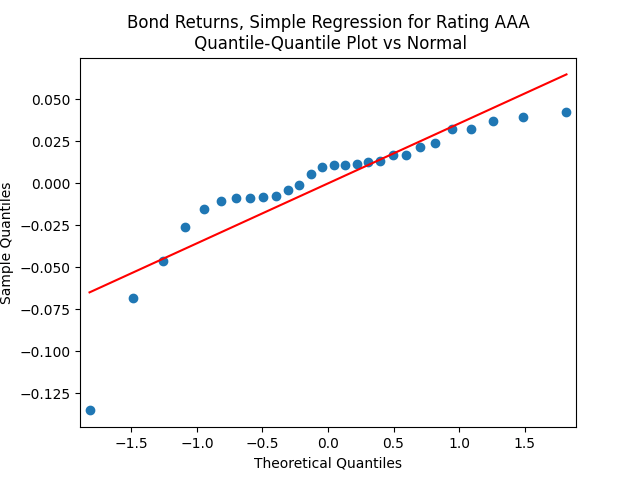

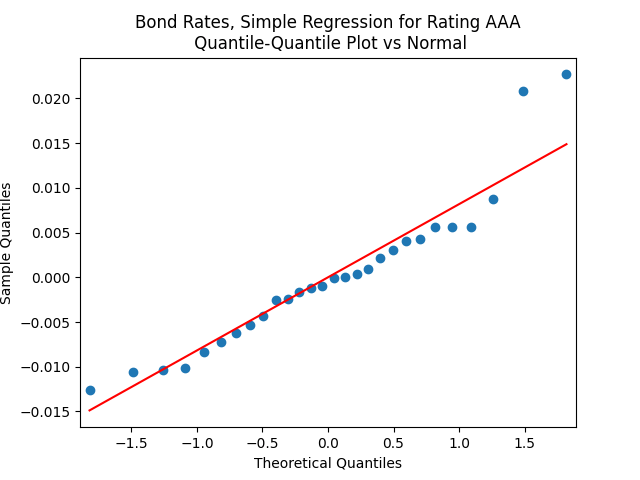

shows that this is well explained by independent identically distributed random variables (white noise). But these are not necessarily normal, judging by the Shapiro-Wilk and Jarque-Bera normality tests. Especially for junk-rated bonds (BB, B, CCC) but also sometimes for investment-grade bonds. The random walk hypothesis could be rejected (using low  ). See also the plots below. We present only the plots for AAA, other ratings are similar. One can generate these graphs by running the code from the GitHub repository mentioned above.

). See also the plots below. We present only the plots for AAA, other ratings are similar. One can generate these graphs by running the code from the GitHub repository mentioned above.

and

and  Next,

Next,  and

and  for Student

for Student  test for

test for  The standard deviation for

The standard deviation for  is

is  The normality tests for innovations

The normality tests for innovations  for Shapiro-Wilk and

for Shapiro-Wilk and  for Jarque-Bera. The plots for ACF of

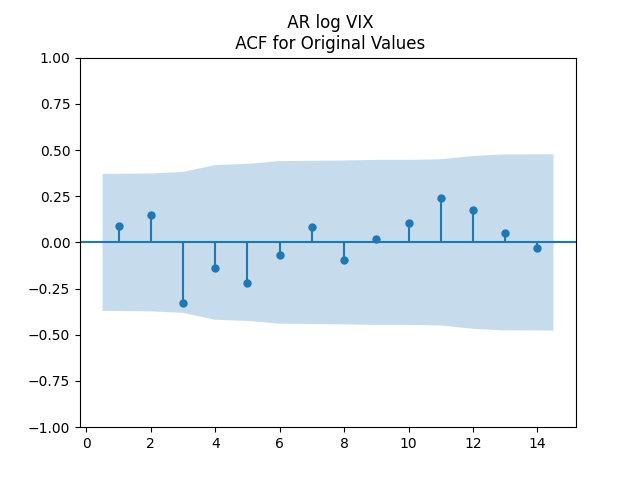

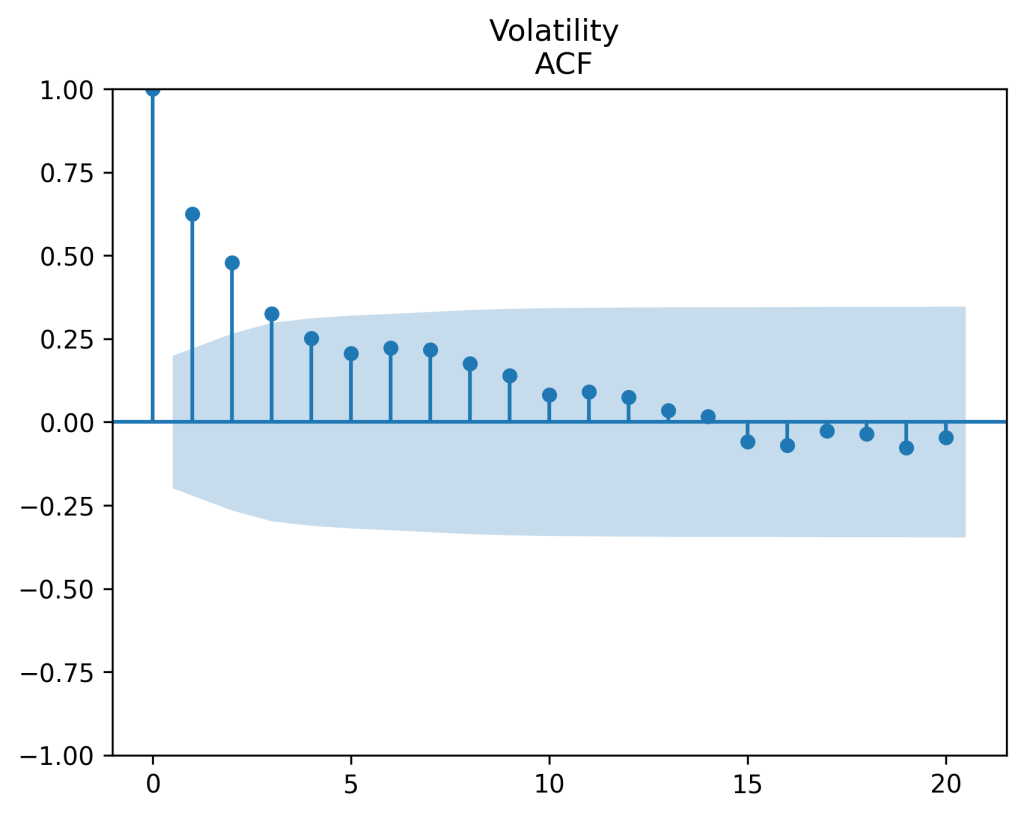

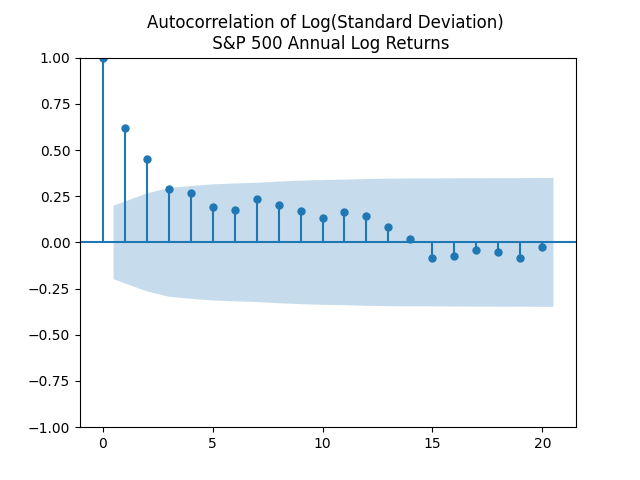

for Jarque-Bera. The plots for ACF of  show independent identically distributed. See below. Thus the log volatility is indeed modeled by the autoregression of order 1, statistically significantly mean-reverting, with Gaussian innovations. This is similar to Angel Piotrowski’s research.

show independent identically distributed. See below. Thus the log volatility is indeed modeled by the autoregression of order 1, statistically significantly mean-reverting, with Gaussian innovations. This is similar to Angel Piotrowski’s research.

We have then

We have then

without intercepts. Let us add intercepts:

without intercepts. Let us add intercepts:

for

for  Next,

Next,  for linear regression with

for linear regression with  for most ratings is much higher than without it. So we need to include this term.

for most ratings is much higher than without it. So we need to include this term.  and

and  we get:

we get:

![(W(t), \varepsilon(t)) \sim \mathcal N_2([0, 0], \Sigma)](https://s0.wp.com/latex.php?latex=+%28W%28t%29%2C+%5Cvarepsilon%28t%29%29+%5Csim+%5Cmathcal+N_2%28%5B0%2C+0%5D%2C+%5CSigma%29+&bg=ffffff&fg=000&s=0&c=20201002) IID

IID to be the diagonal matrix, but might as well make it a complete matrix. This model fits very well. A disadvantage is that we have only ~30 years of data. We do need to normalize innovations of rates by dividing these by VIX. We do need the term

to be the diagonal matrix, but might as well make it a complete matrix. This model fits very well. A disadvantage is that we have only ~30 years of data. We do need to normalize innovations of rates by dividing these by VIX. We do need the term

of earnings for the last 5 years. This is similar to the classic

of earnings for the last 5 years. This is similar to the classic  at end of year

at end of year

must be 4-5%. This equation shows that after detrending, this is the classic autoregression of order 1. We can rewrite this in the more standard ordinary least squares regression form:

must be 4-5%. This equation shows that after detrending, this is the classic autoregression of order 1. We can rewrite this in the more standard ordinary least squares regression form:

and

and  and

and  All three coefficients are significantly different from zero: Student T-test gives

All three coefficients are significantly different from zero: Student T-test gives  values

values  But the Jarque-Bera test shows that innovations are not Gaussian:

But the Jarque-Bera test shows that innovations are not Gaussian:  This is confirmed by the following quantile-quantile plot below. But the autocorrelation function plots for

This is confirmed by the following quantile-quantile plot below. But the autocorrelation function plots for

is ~2% per year, and total market returns

is ~2% per year, and total market returns  and it is much higher than 4-5% per year for a few years, then the stock market starts to be overvalued. We formally can write this as an autoregression of order 1 for the cumulative sum

and it is much higher than 4-5% per year for a few years, then the stock market starts to be overvalued. We formally can write this as an autoregression of order 1 for the cumulative sum  after subtracting the trend

after subtracting the trend  where

where  . Our bubble measure is

. Our bubble measure is  and it is high when the market is overvalued. Let us write linear regression:

and it is high when the market is overvalued. Let us write linear regression:

We can see that the estimate for

We can see that the estimate for  gives

gives  so we can reject the random walk hypothesis: The model is stationary after detrending. Moreover, we can apply the Student test, since the residuals (innovations)

so we can reject the random walk hypothesis: The model is stationary after detrending. Moreover, we can apply the Student test, since the residuals (innovations)  with

with  This is shown by the autocorrelation function plot for

This is shown by the autocorrelation function plot for

Angel did this by making the autocorrelation function plots for

Angel did this by making the autocorrelation function plots for

and

and  so there is mean-reversion. She did not test for unit root but I am very sure this hypothesis (that

so there is mean-reversion. She did not test for unit root but I am very sure this hypothesis (that  ) would be rejected.

) would be rejected.  is Gaussian with mean -4.68 and variance 0.218. Using the moment generating function for the normal distribution, we can compute

is Gaussian with mean -4.68 and variance 0.218. Using the moment generating function for the normal distribution, we can compute ![\mathbb E[V(\infty)] = 0.0104](https://s0.wp.com/latex.php?latex=+%5Cmathbb+E%5BV%28%5Cinfty%29%5D+%3D+0.0104+&bg=ffffff&fg=000&s=0&c=20201002) and variance

and variance

is shown on the right. It is clear there is significant autocorrelation with lag 1. Both plots seem to be for white noise, no autocorrelation.

is shown on the right. It is clear there is significant autocorrelation with lag 1. Both plots seem to be for white noise, no autocorrelation.

and December Consumer Price Index

and December Consumer Price Index  We take the price

We take the price  . Price returns are computed as

. Price returns are computed as  and total returns are

and total returns are  for nominal versions. But for real versions, we need to subtract

for nominal versions. But for real versions, we need to subtract  from each of these. You see that all returns are logarithmic (geometric), so there is no problem of compound interest. If wealth at end of year

from each of these. You see that all returns are logarithmic (geometric), so there is no problem of compound interest. If wealth at end of year  then

then  where

where

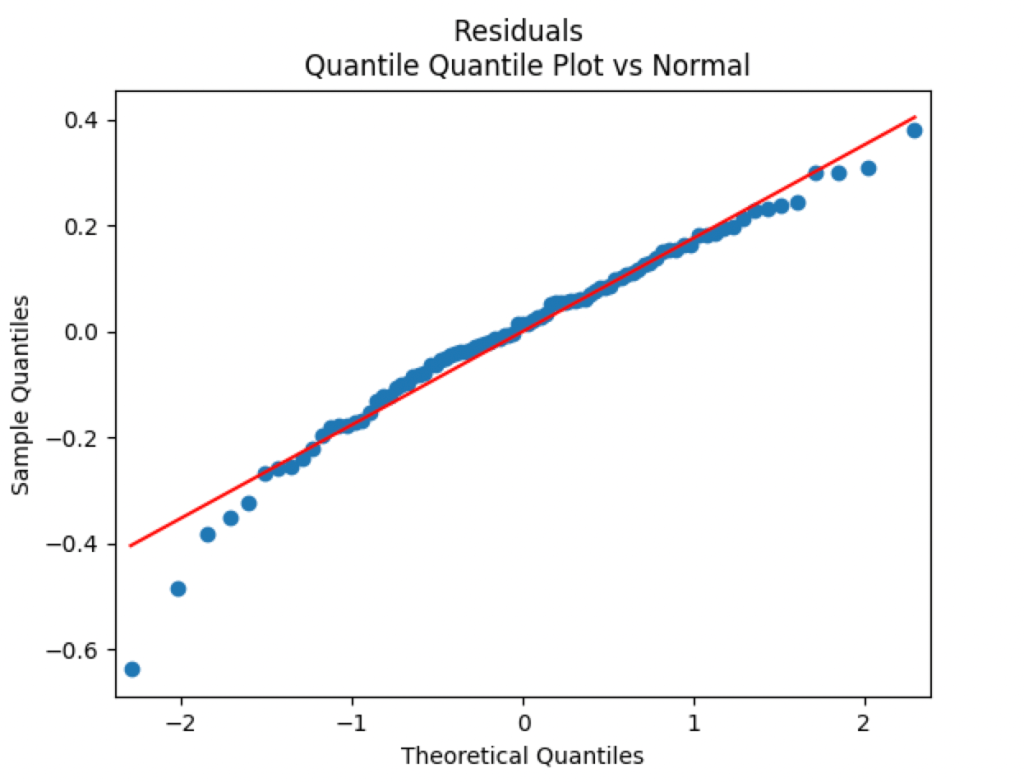

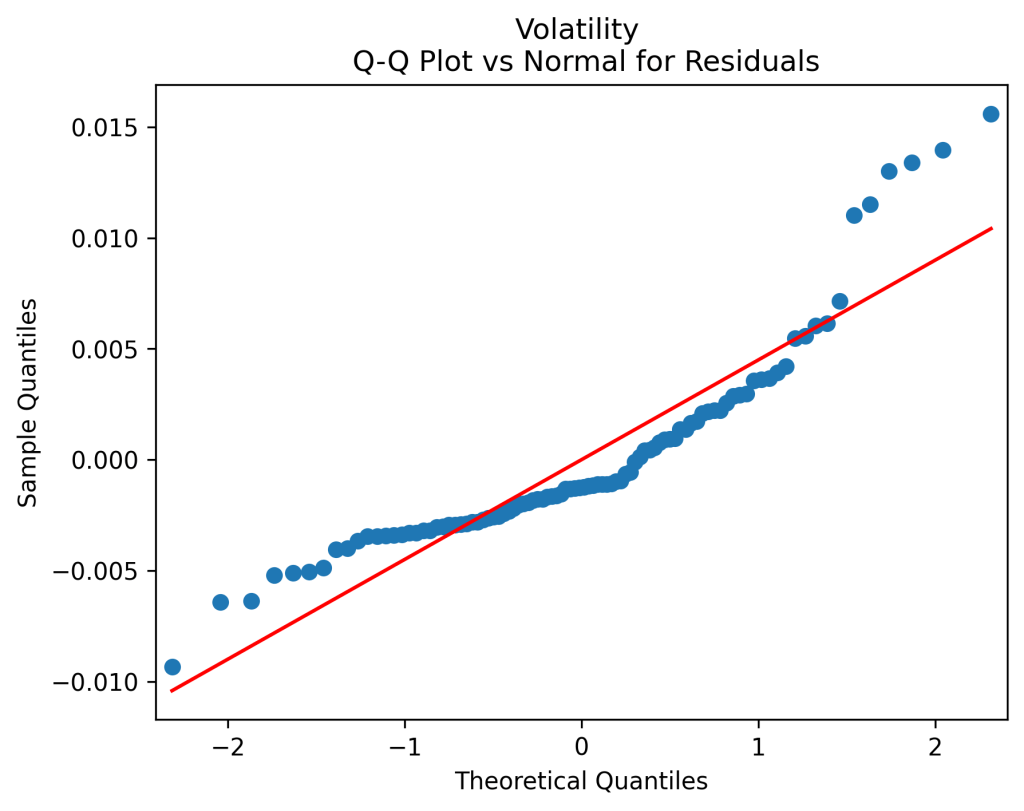

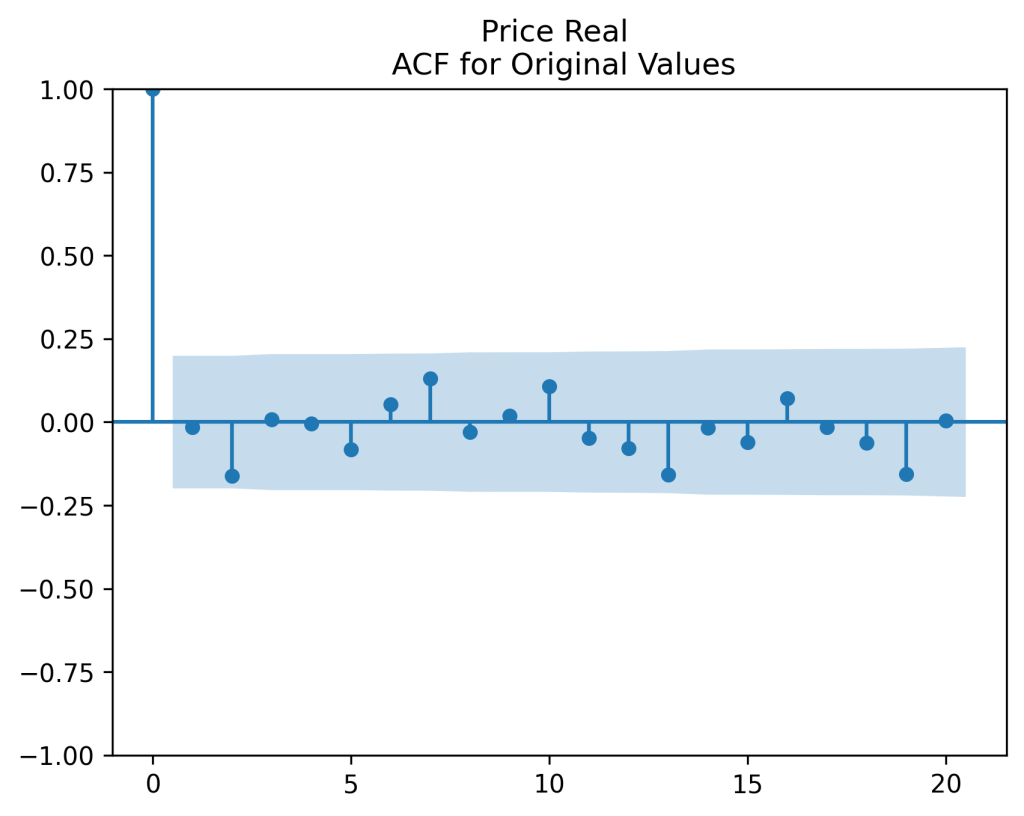

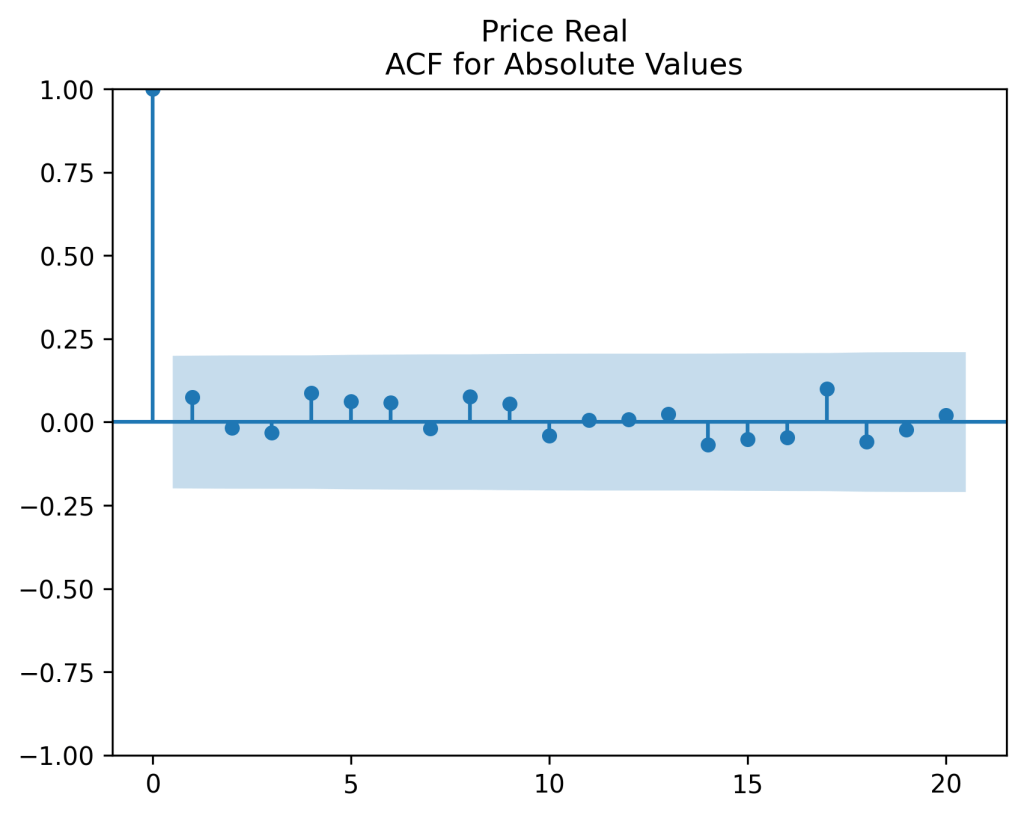

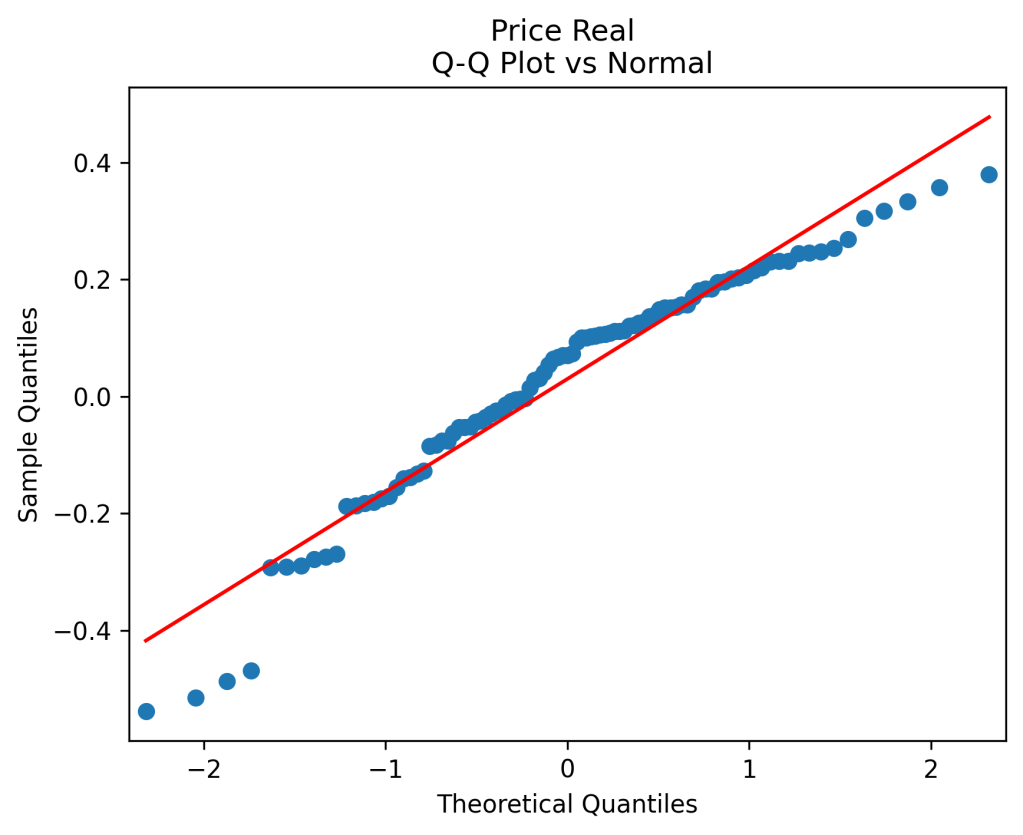

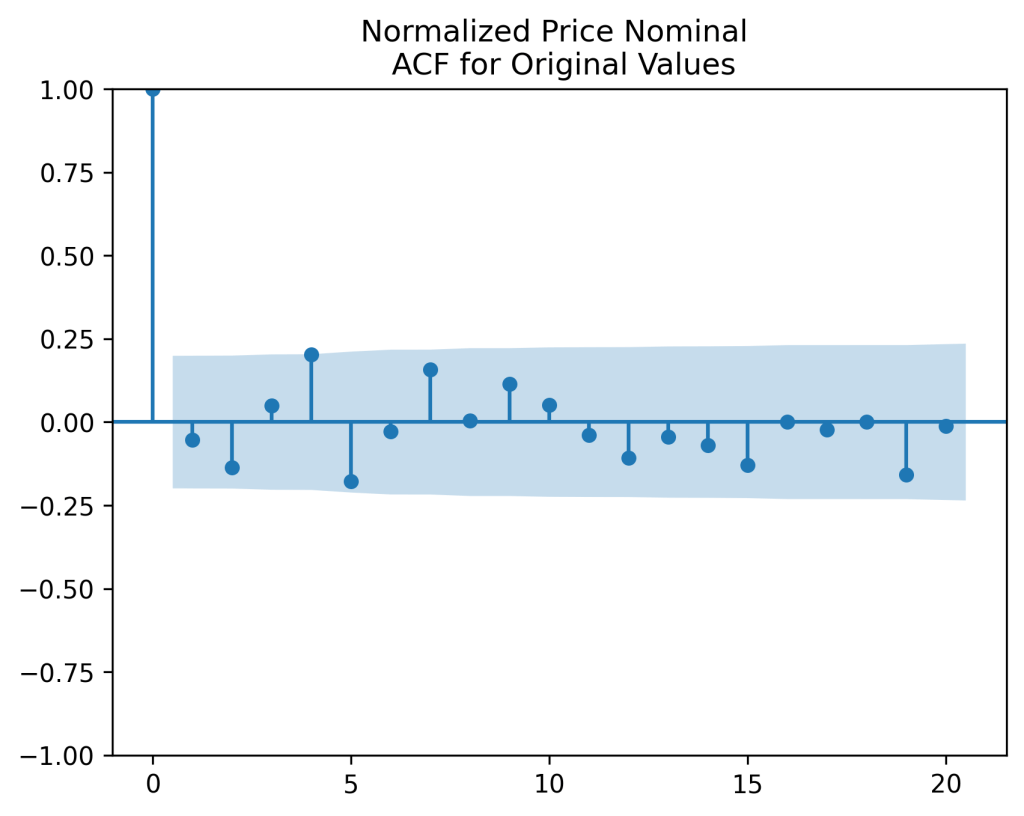

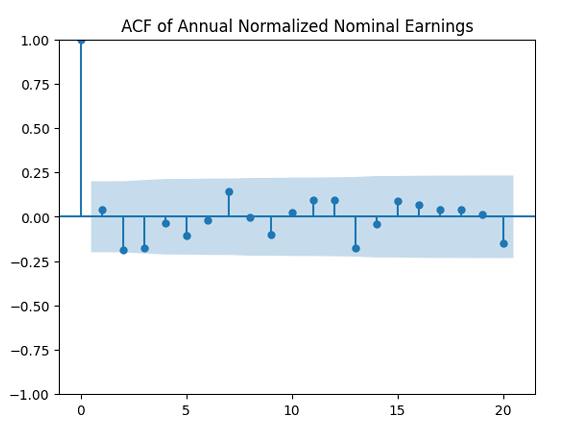

(right panel) show these are close to zero. So it is reasonable to model these as independent identically distributed random variables. However, the below quantile-quantile plot versus the normal distribution shows these are not normal.

(right panel) show these are close to zero. So it is reasonable to model these as independent identically distributed random variables. However, the below quantile-quantile plot versus the normal distribution shows these are not normal.

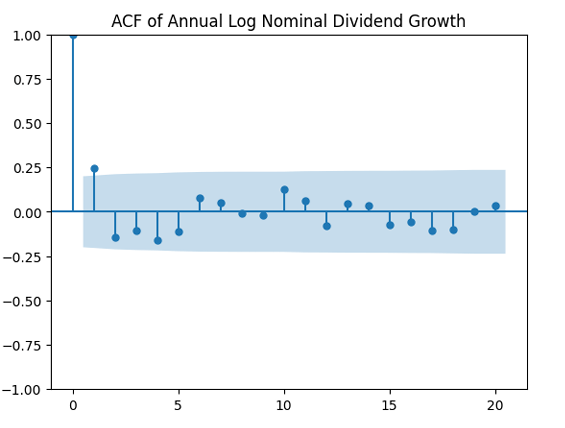

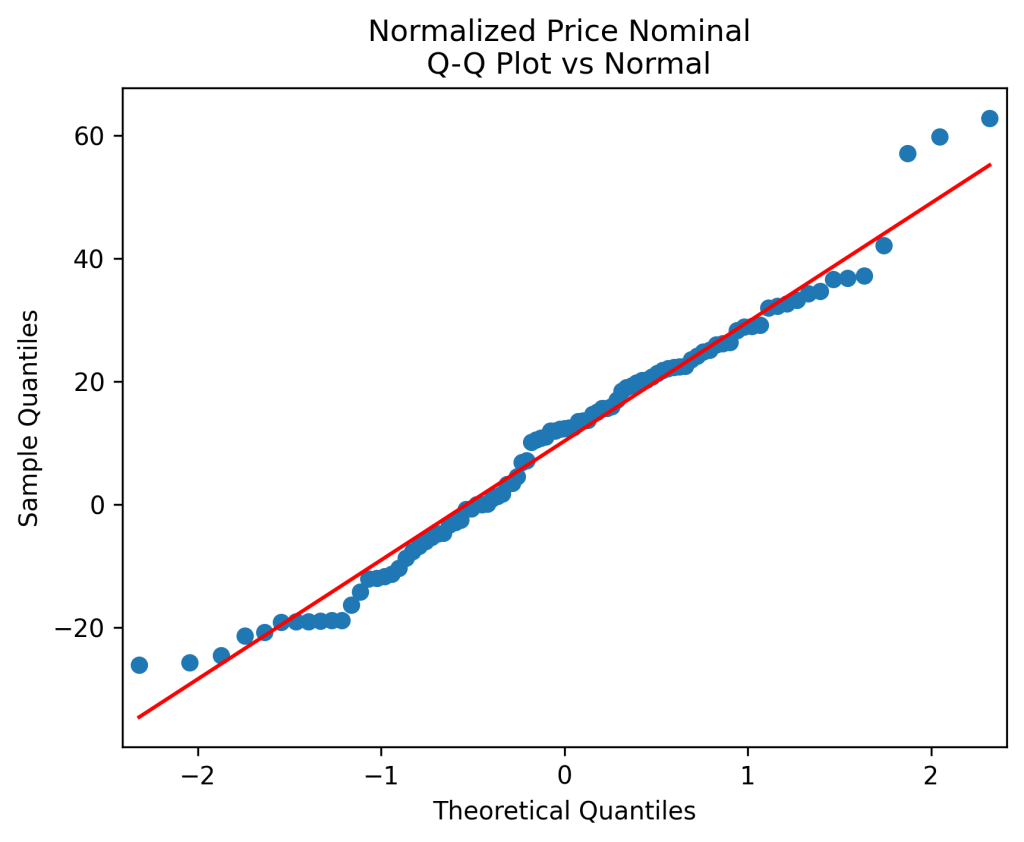

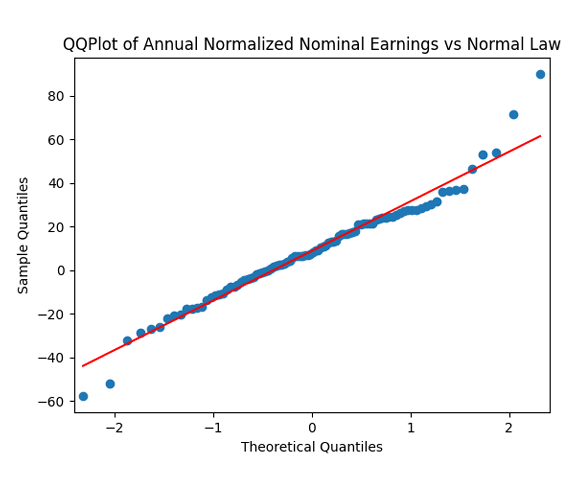

We do this first for nominal earnings, without adjustment for inflation. We analyze

We do this first for nominal earnings, without adjustment for inflation. We analyze  whether it is Gaussian independent identically distributed. We make the quantile-quantile (QQ) plot versus the normal distribution.

whether it is Gaussian independent identically distributed. We make the quantile-quantile (QQ) plot versus the normal distribution.

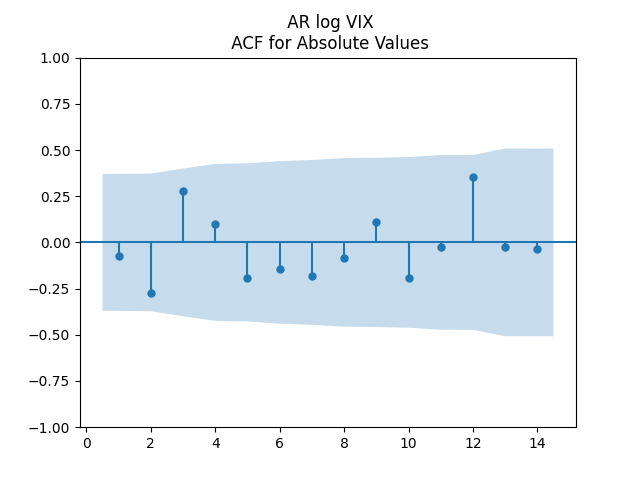

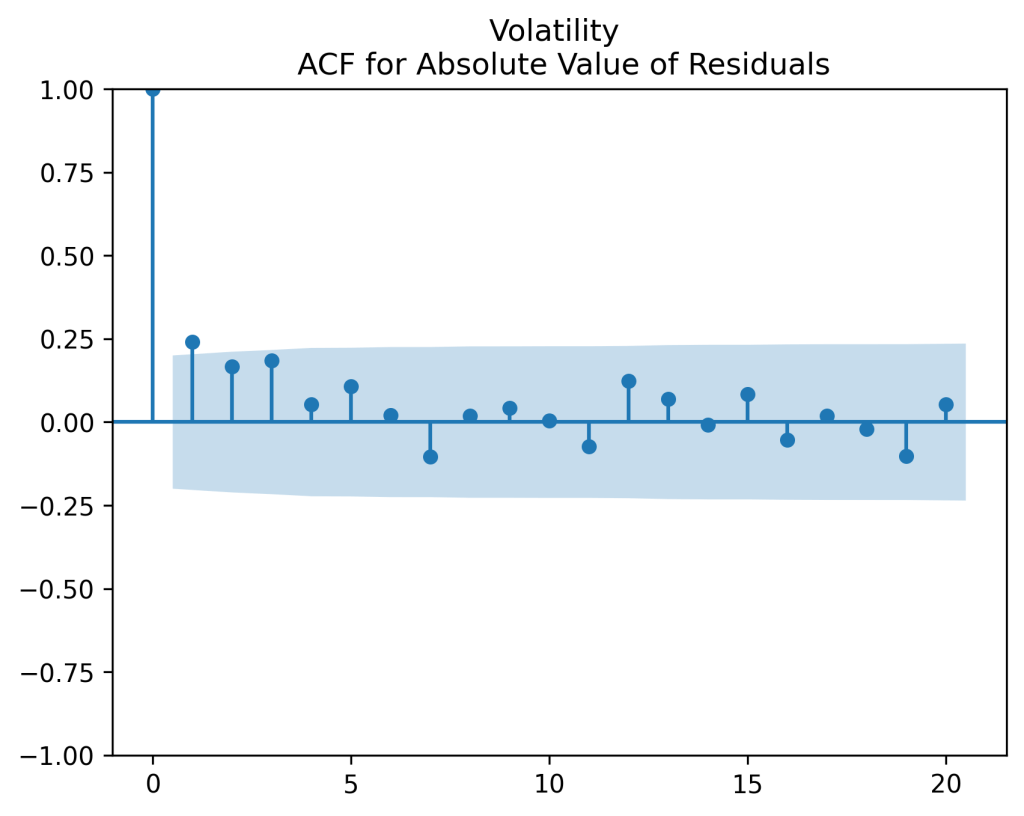

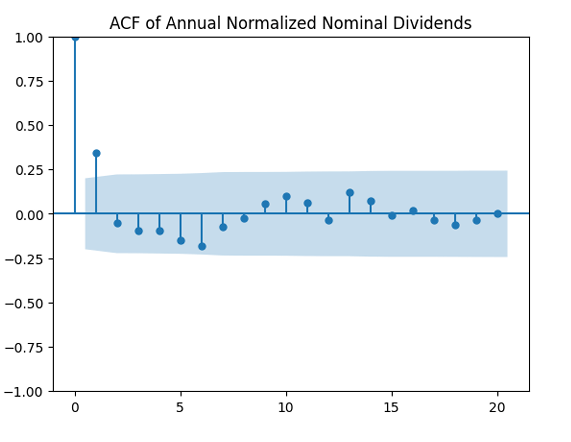

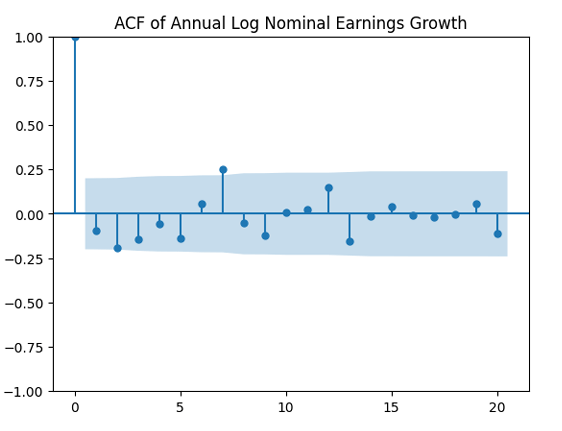

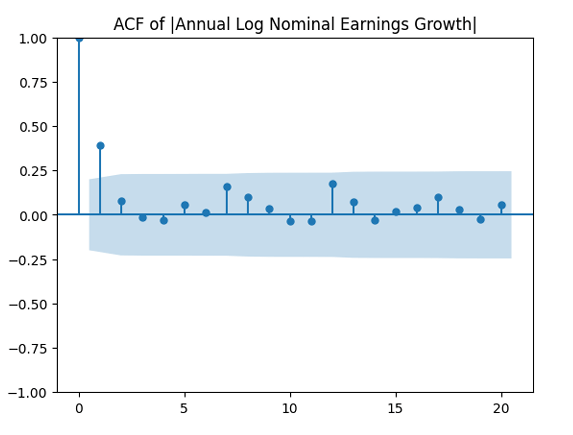

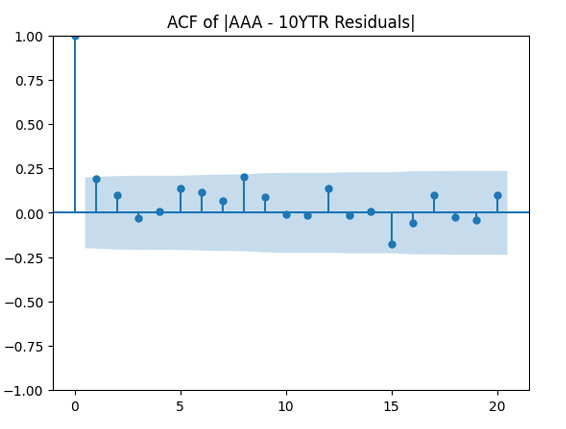

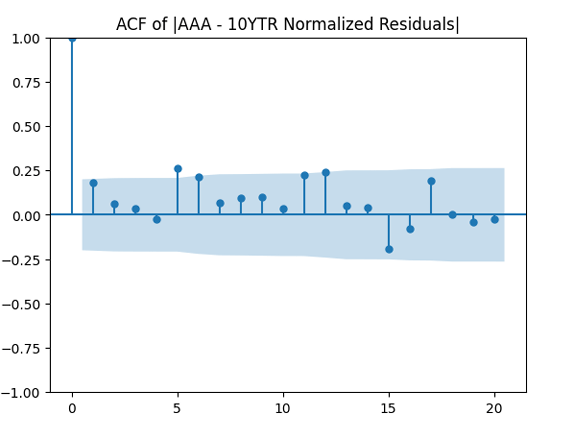

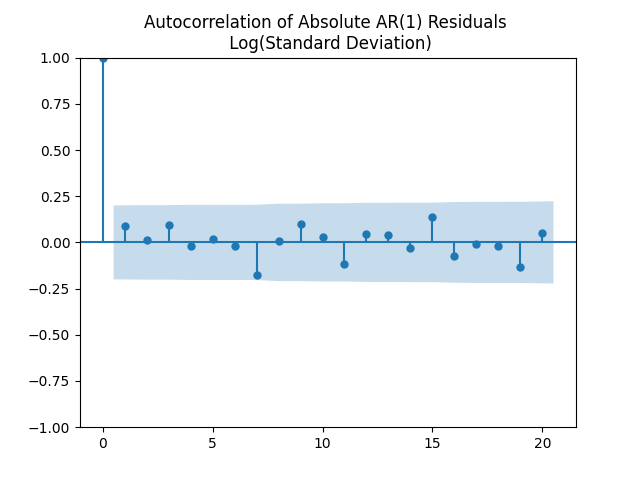

are uncorrelated. But with absolute values, this is not true. There is a significant autocorrelation of lag 1:

are uncorrelated. But with absolute values, this is not true. There is a significant autocorrelation of lag 1:

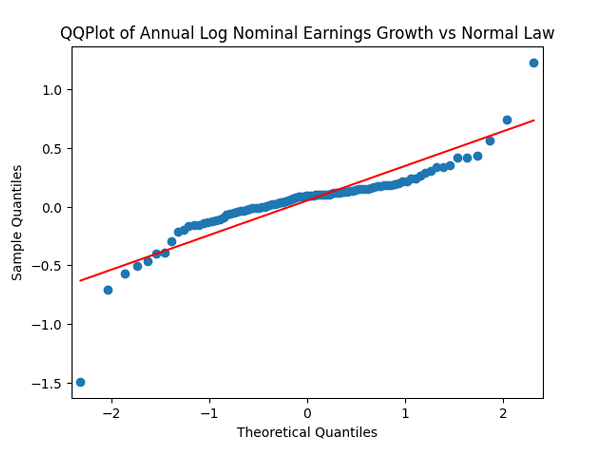

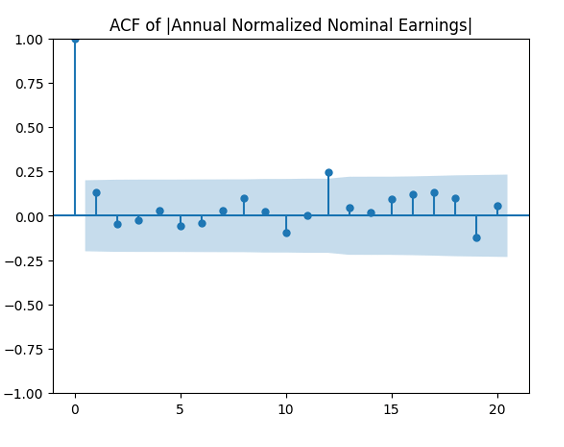

Does this division improve these terms to make them closer to Gaussian independent identically distributed? In fact, yes!

Does this division improve these terms to make them closer to Gaussian independent identically distributed? In fact, yes!

as independent identically distributed Gaussian.

as independent identically distributed Gaussian.

![(W(t), Z(t)) \sim \mathcal N_2([0, 0], \Sigma)](https://s0.wp.com/latex.php?latex=+%28W%28t%29%2C+Z%28t%29%29+%5Csim+%5Cmathcal+N_2%28%5B0%2C+0%5D%2C+%5CSigma%29+&bg=ffffff&fg=000&s=0&c=20201002) are independent identically distributed bivariate normal, with mean zero and covariance 2×2 matrix

are independent identically distributed bivariate normal, with mean zero and covariance 2×2 matrix  Apply an autoregression of order 1:

Apply an autoregression of order 1:  We expect mean reversion for this spread, which is true for

We expect mean reversion for this spread, which is true for  This is different from

This is different from  where this process is a random walk, when future movements are independent of the past.

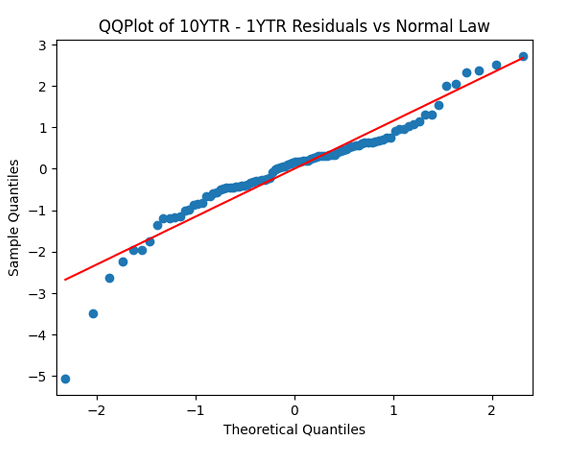

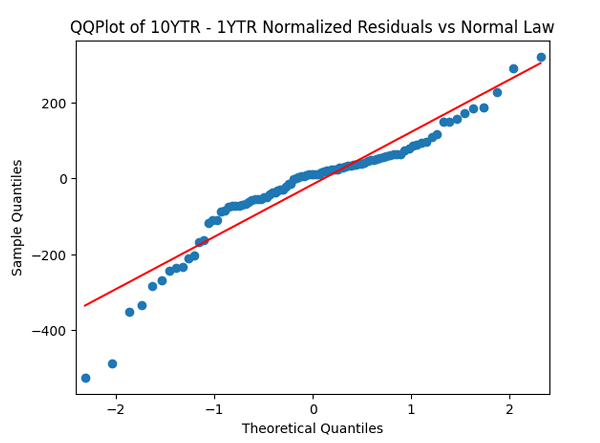

where this process is a random walk, when future movements are independent of the past.  Apply the quantile-quantile plot versus the normal distribution. Next, divide these innovations by annual volatility and make the quantile-quantile plot again.

Apply the quantile-quantile plot versus the normal distribution. Next, divide these innovations by annual volatility and make the quantile-quantile plot again.

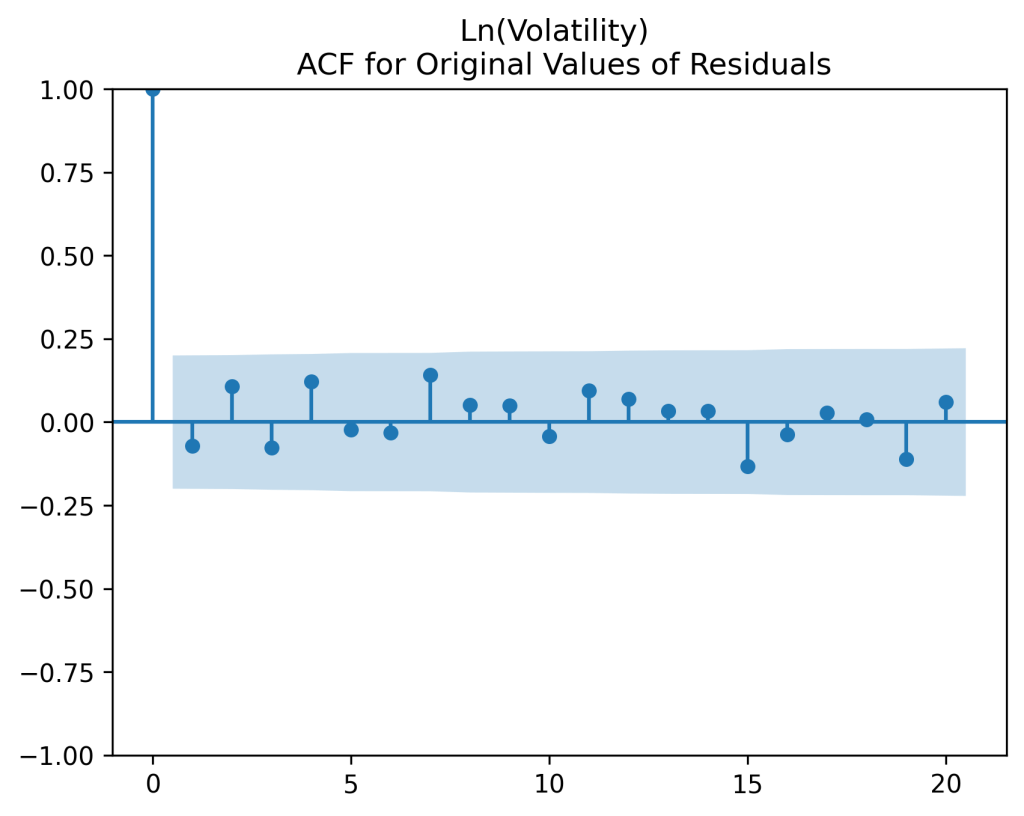

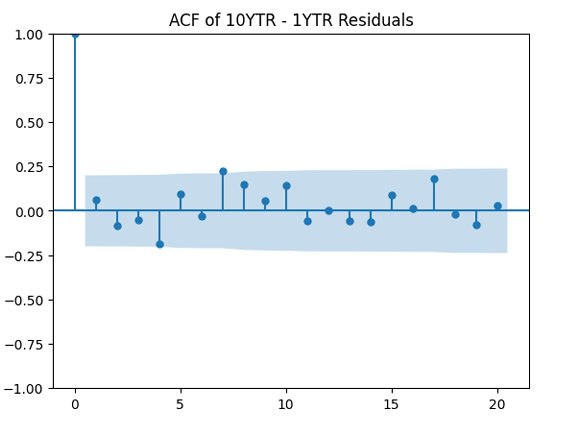

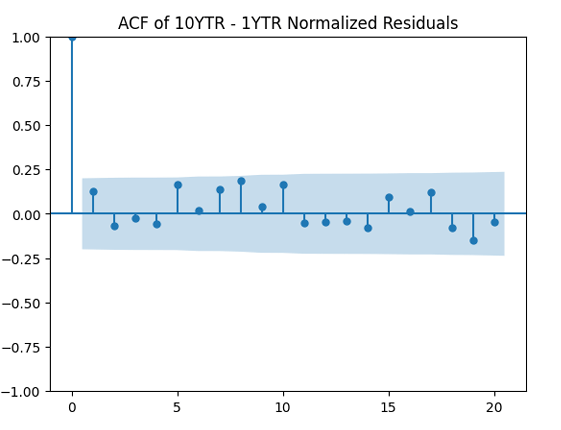

Next, divide by the volatility and plot the autocorrelation function again, now for

Next, divide by the volatility and plot the autocorrelation function again, now for  Both plots seem to be for white noise, no autocorrelation.

Both plots seem to be for white noise, no autocorrelation.

to see whether it improves the result. It does not, in fact!

to see whether it improves the result. It does not, in fact!

Then she computed standard deviation of these log returns for day

Then she computed standard deviation of these log returns for day  be this standard deviation, usually called volatility, for year

be this standard deviation, usually called volatility, for year

It is defined as

It is defined as  This looks like an autocorrelation function for an autoregression of order 1.

This looks like an autocorrelation function for an autoregression of order 1.

with

with  and

and  Let us test whether the innovations

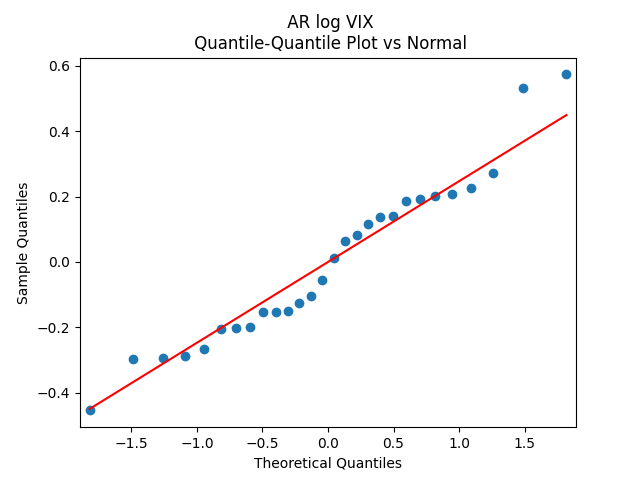

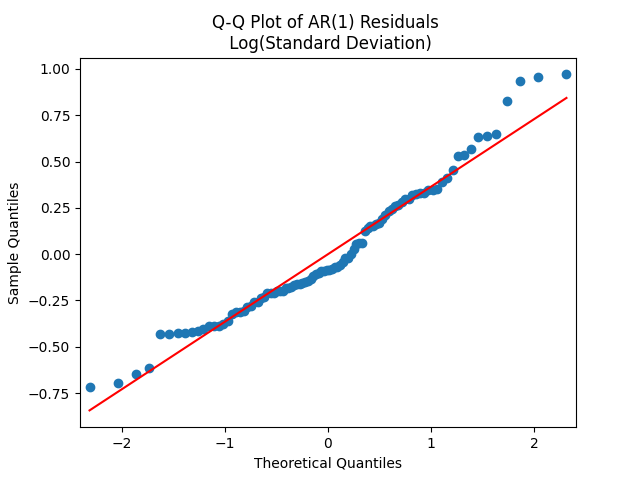

Let us test whether the innovations  are Gaussian. Apply the quantile-quantile plot versus the normal distribution. This looks like pretty close to a Gaussian law!

are Gaussian. Apply the quantile-quantile plot versus the normal distribution. This looks like pretty close to a Gaussian law!

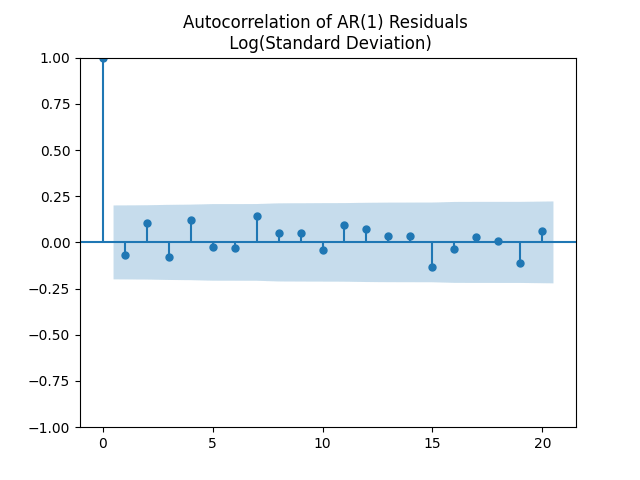

to see that they correspond to white noise.

to see that they correspond to white noise.

We have numerical estimates

We have numerical estimates  Therefore, this autoregression has a stationary distribution, or an invariant probability measure,

Therefore, this autoregression has a stationary distribution, or an invariant probability measure,  such that

such that  Angel has computed that mean and variance of this stationary distribution.

Angel has computed that mean and variance of this stationary distribution.