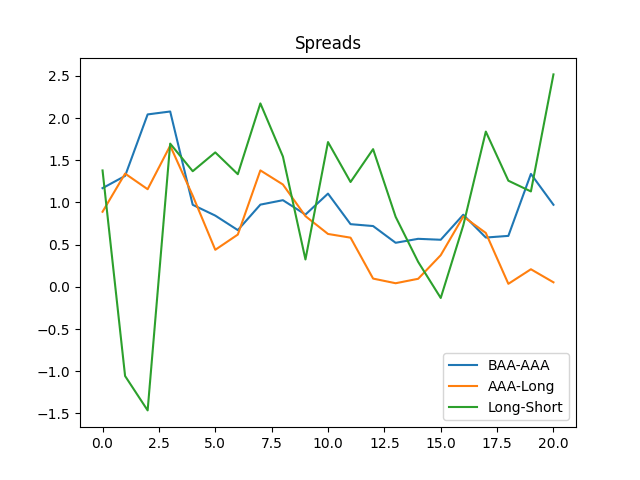

This is the continuation of the research in this main post and addendum post. We remove earnings yield from regression for stock index returns. The rates-only.py code is from GitHub/asarantsev repository 3spreads-CAPE-simulator

Consider annual S&P returns

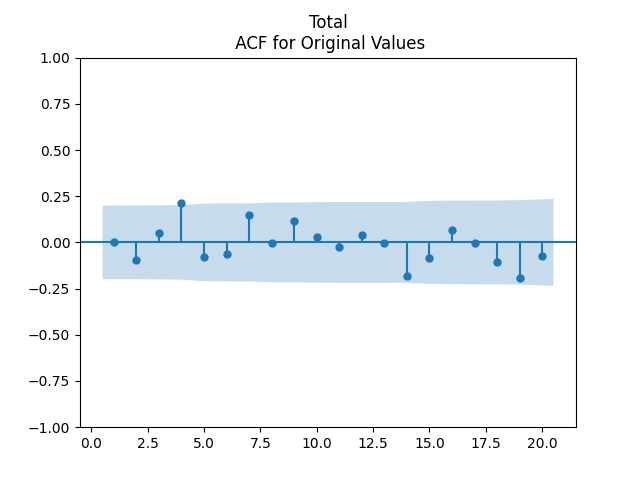

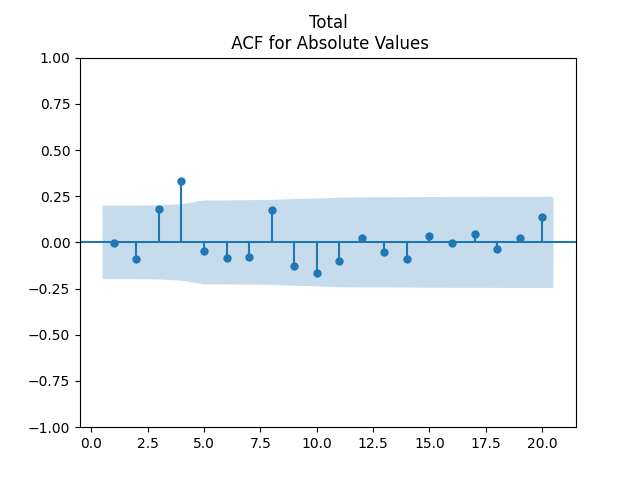

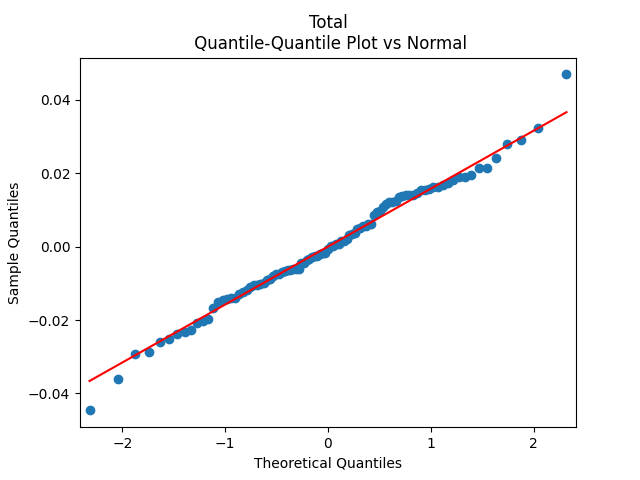

Standard analysis of residuals

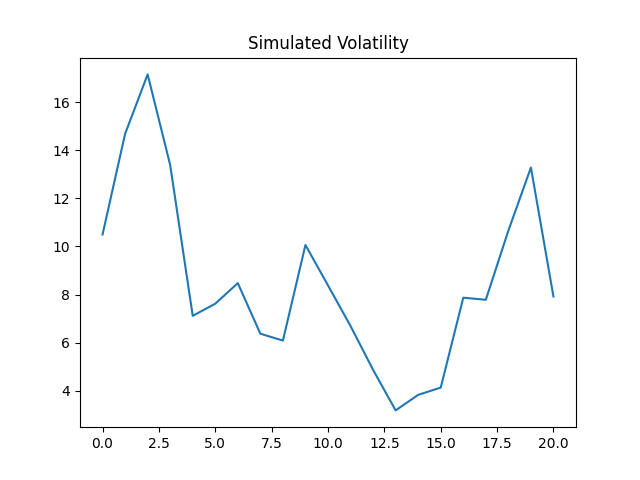

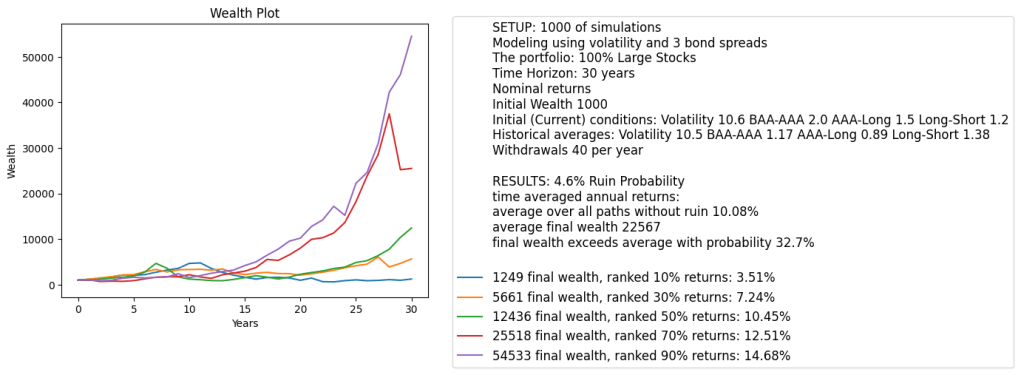

We added to this GitHub repository the entire simulator for the rates-only model (with annual volatility, of course). It is done in Python file rates-only-sim.py in the same repository. See below the graph.

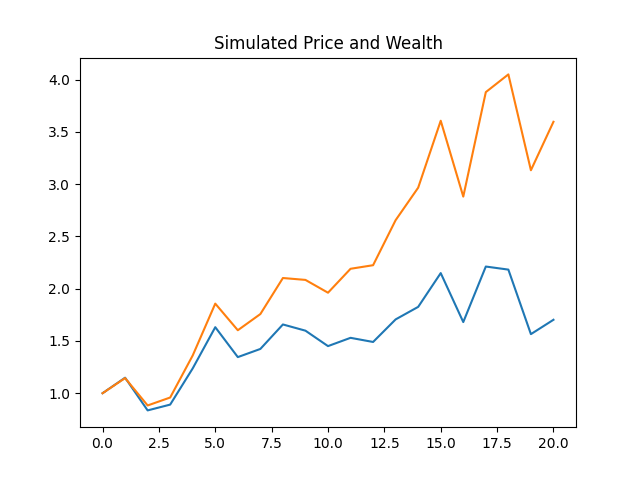

Below we show one simulated path of prices and wealth. This simulation is for the case of real (inflation-adjusted) version and 20-year horizon.

Finally, pick

As before, we have this strange value at lag 4 for autocorrelation. This presents no problem, since other values are low.

Leave a comment