Background: I continue the previous post of joint work with my undergraduate student Angel Piotrowski. Consider my work arXiv:1905.04603. We wrote about this in yet another post. In a GitHub/asarantsev repository we updated our code and data.

Let

where innovations

As discussed before, the difference between our research and arXiv:1905.04603 is that we take December CPI data instead of January to compute inflation, and end-of-year S&P index data instead of average January close level. Also, we consider 10-year instead of 5-year trailing window for real earnings.

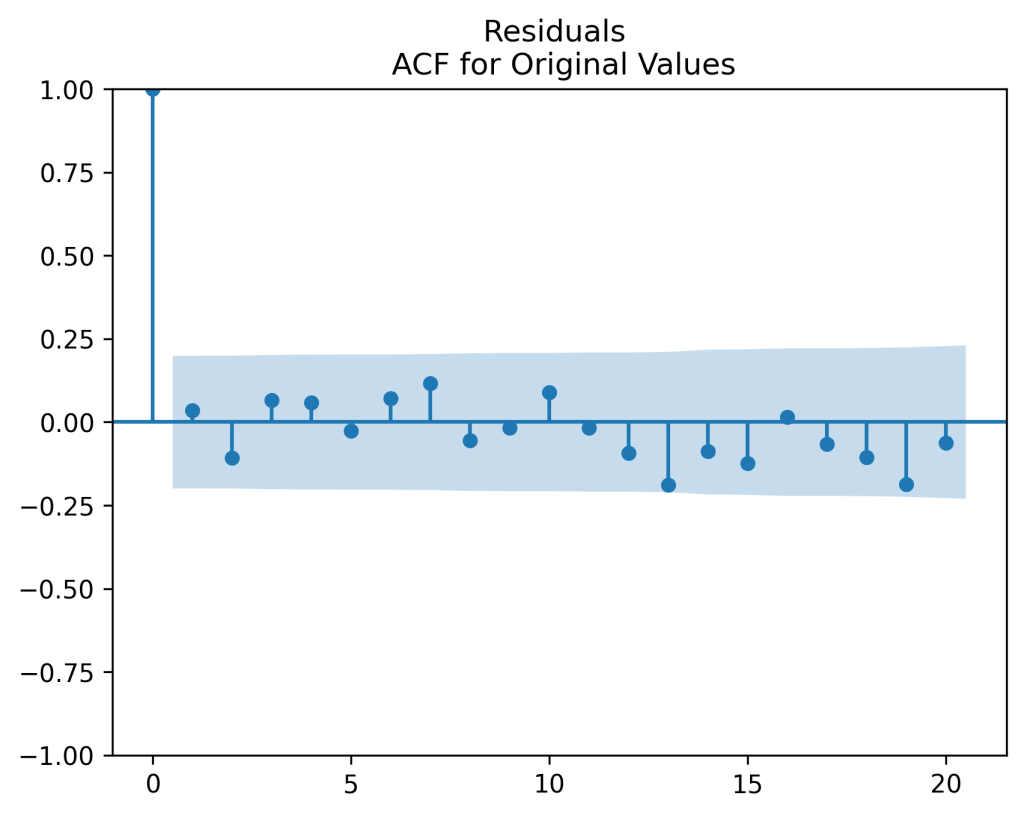

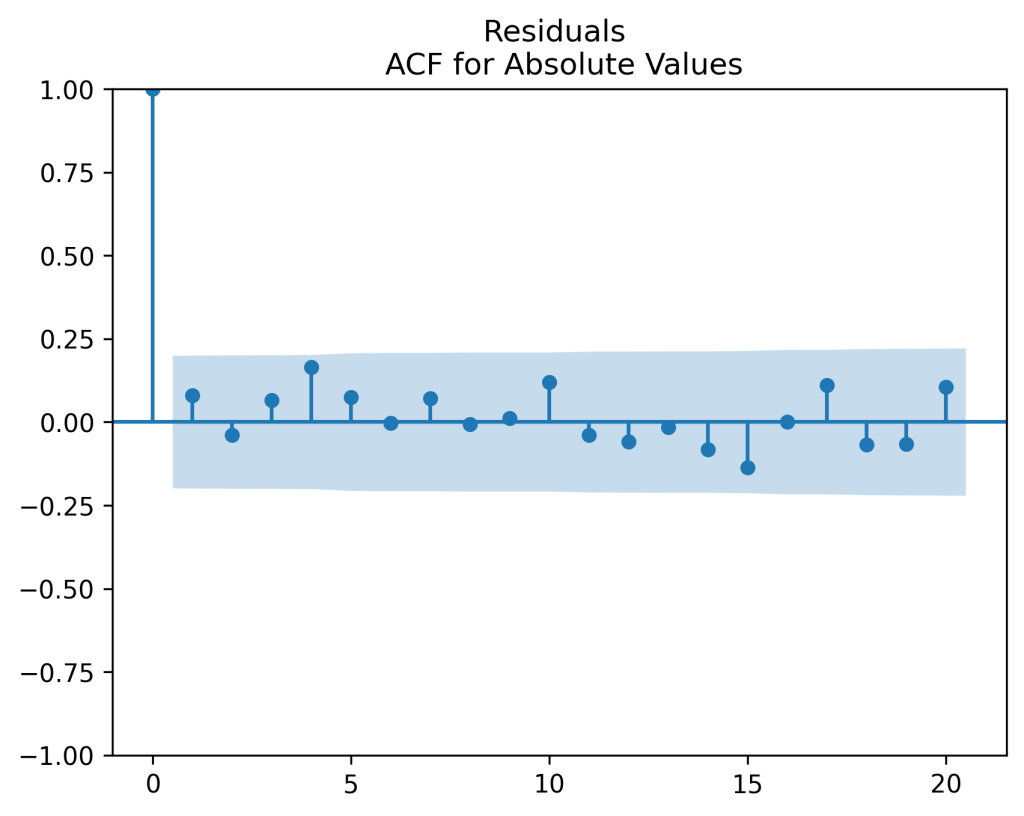

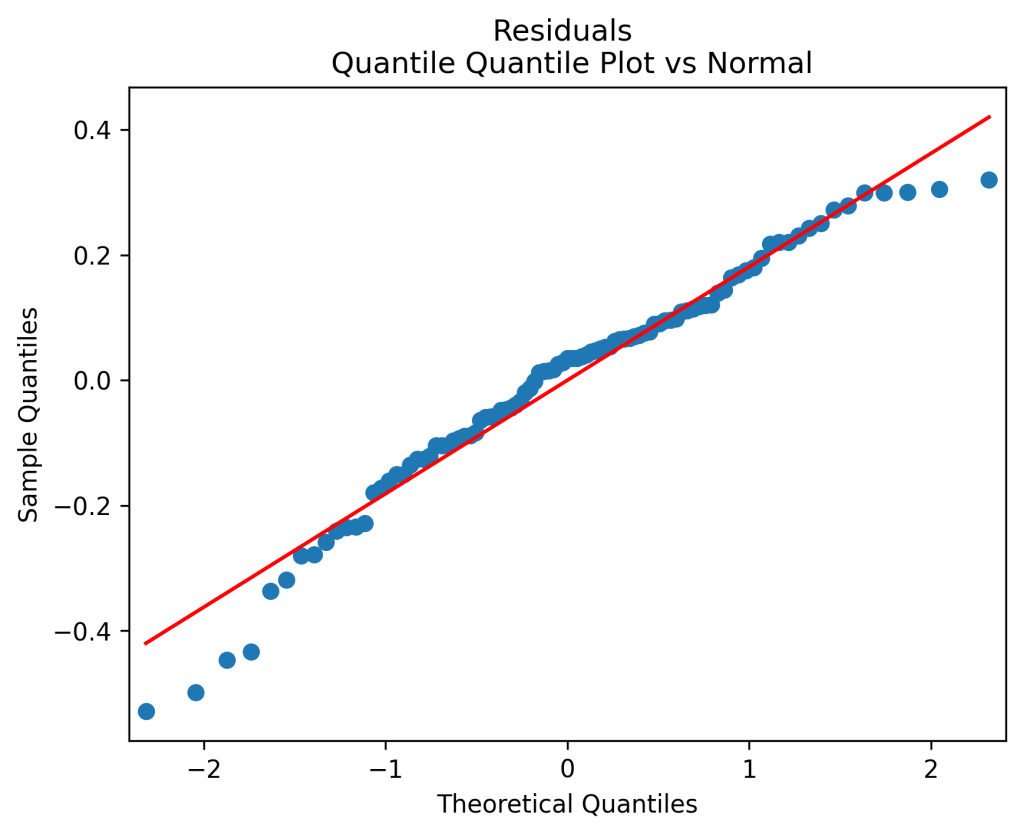

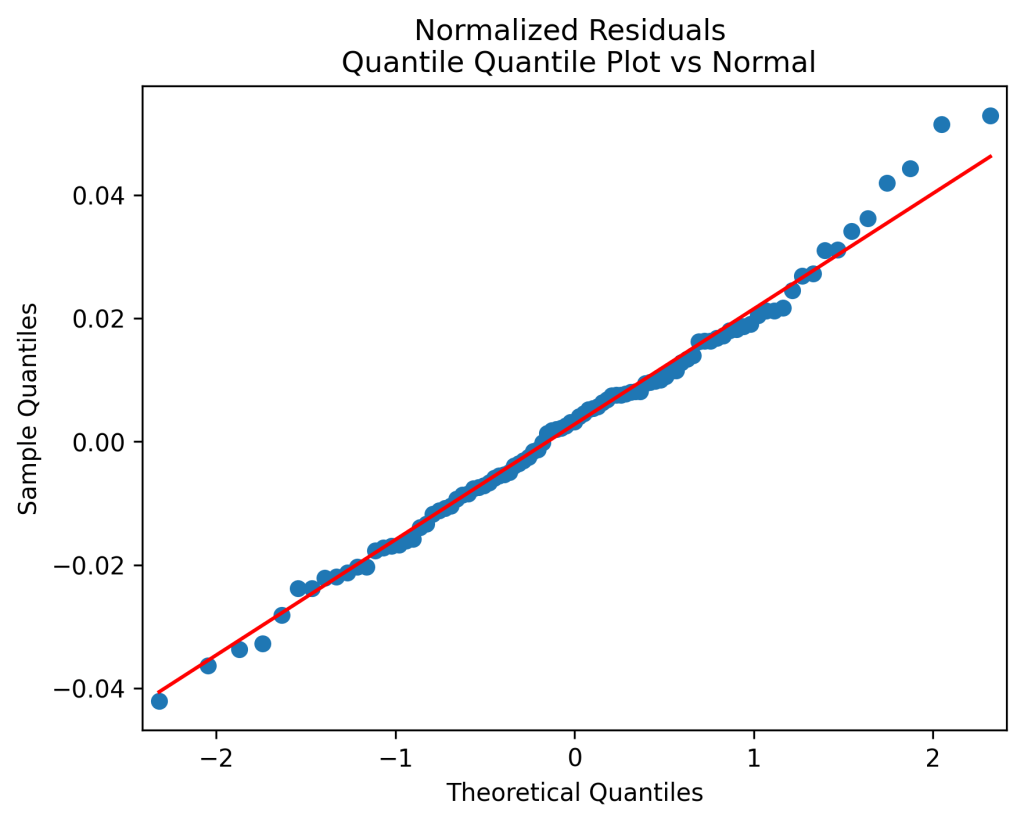

Original model fit: We get innovations which are IID but not quite Gaussian. See plots below. Also, the Shapiro-Wilk and Jarque-Bera tests give us

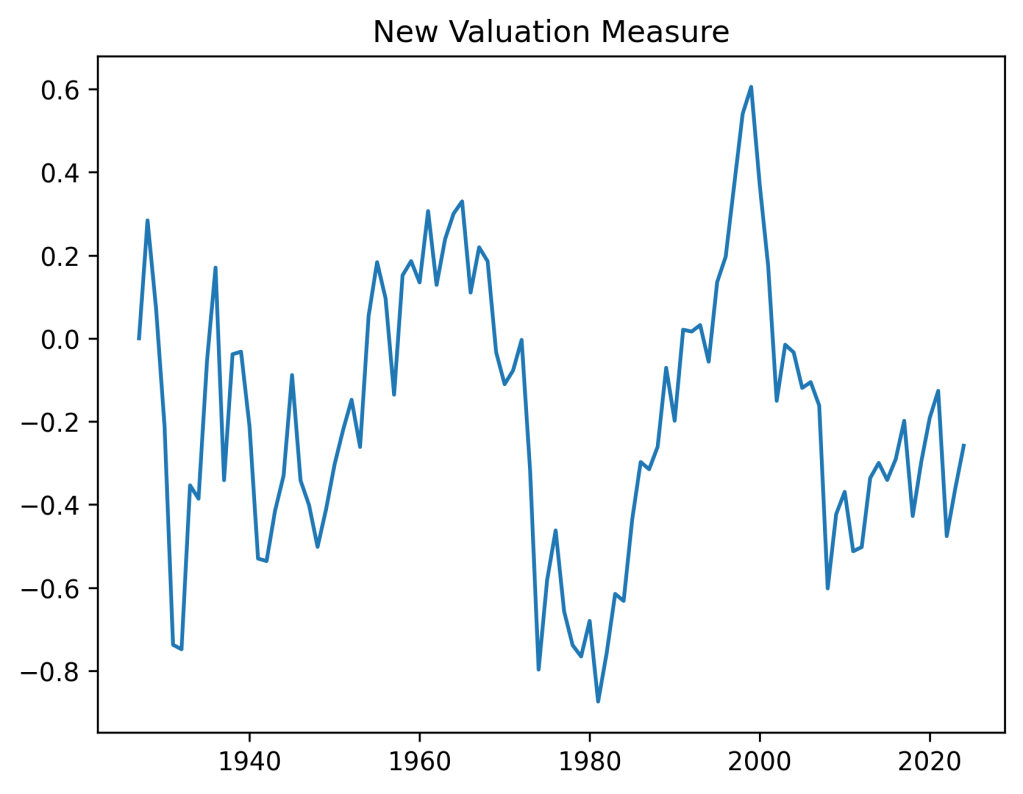

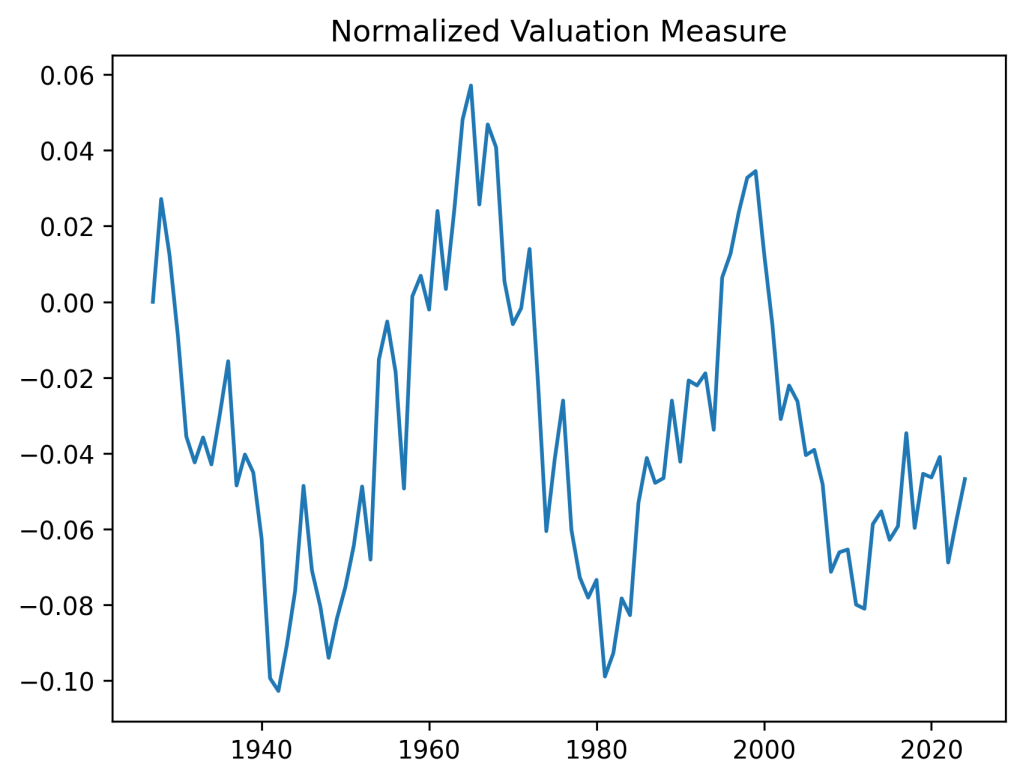

Bubbles and busts: The valuation measure has plot shown below. It is clear that the current valuation measure is well below the historical average. This is in contrast with the classic price-earnings ratio and Shiller CAPE. Both show that the S&P is currently overvalued. However, on the graph below we can see the overvaluation right before the Great Depression, in the 1960s, and at the start of the 21st century (the dotcom bubble). This graph is quite similar to the one in arXiv:1950.04603.

Normalize innovations: Next, let us divide innovations

In other words, it is reasonable to model

Normalize regression, not residuals: Alternatively, we can divide implied dividend yield by volatility and perform this autoregression for the new terms: Consider

Again, the Student T-test gives us

The

Update: We used the new regression in the financial simulator. We use the version without the volatility factor, which after division becomes the intercept of the ordinary least squares new regression. This makes the innovations multiplied by this volatility, but does not introduce any new factors in this model. We only compare total returns and earnings growth.

Leave a reply to To Do List – My Finance Cancel reply