See https://github.com/asarantsev/growth-spread for code and data.

Model explanation: Continuing research by Ian Anderson with updated data, 1927-2024, consider the following model for

As usual, this can unfortunately lead to ordinary least squares for regression fitting not applicable. Let us first divide each question by annual volatility, and add an intercept (constant) for completeness (because usually, linear regression includes an intercept). We get:

In the vector form, we can write this as

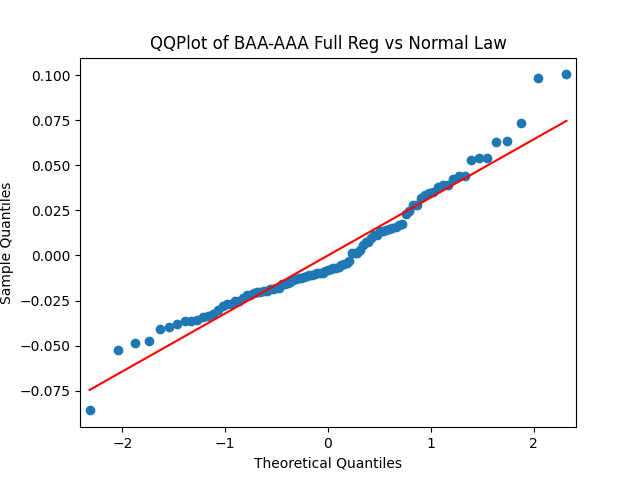

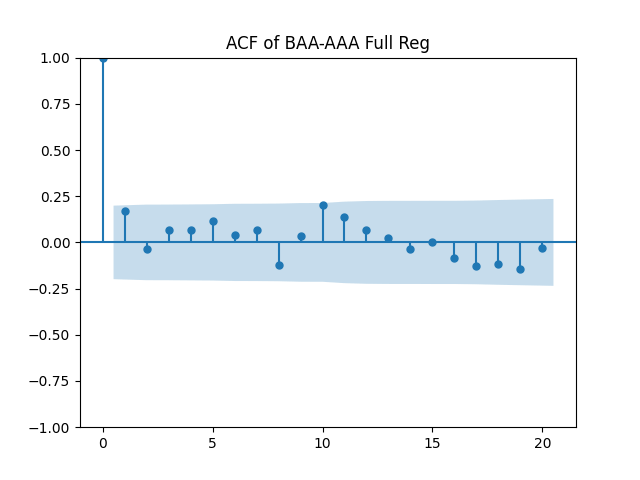

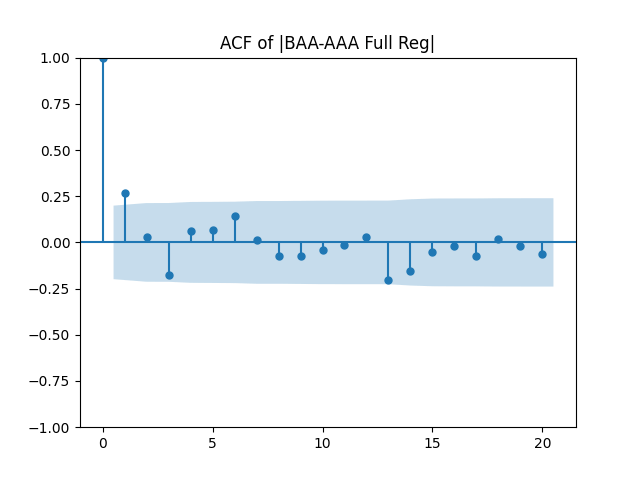

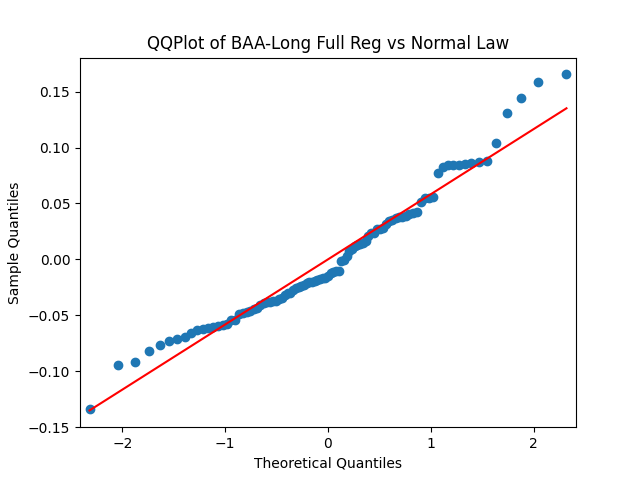

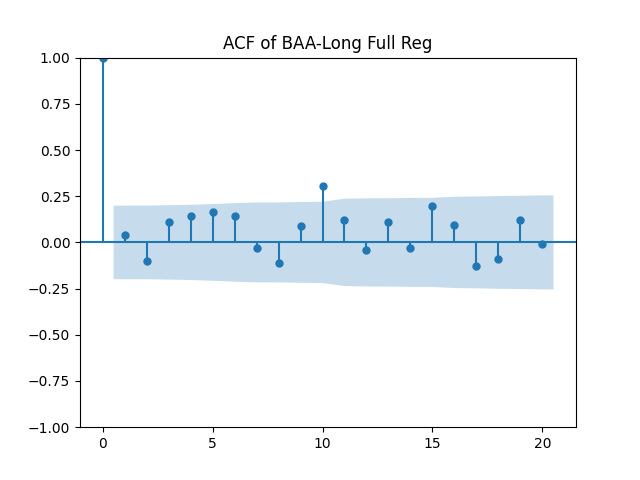

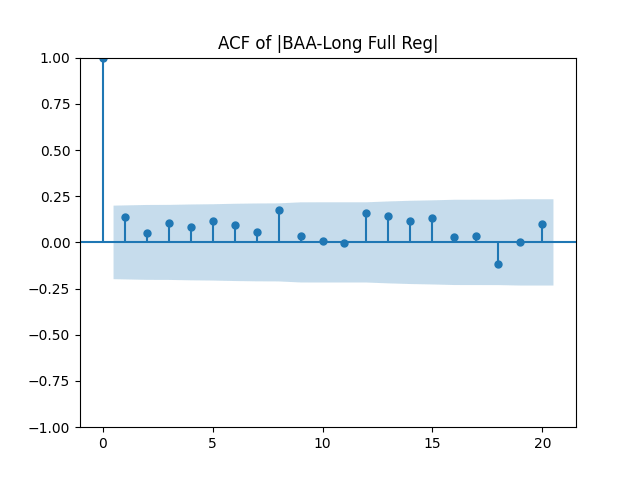

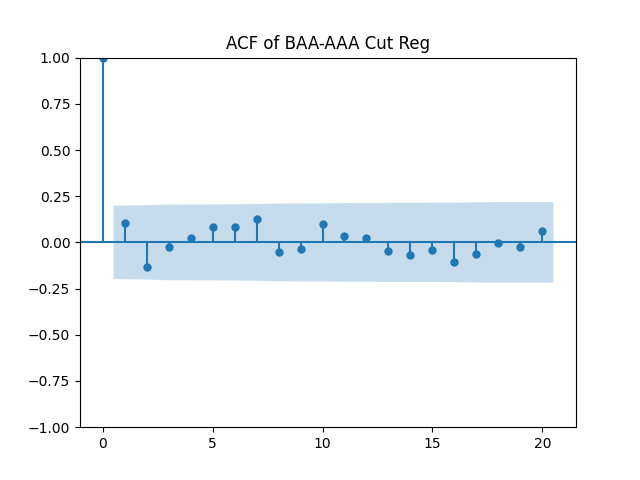

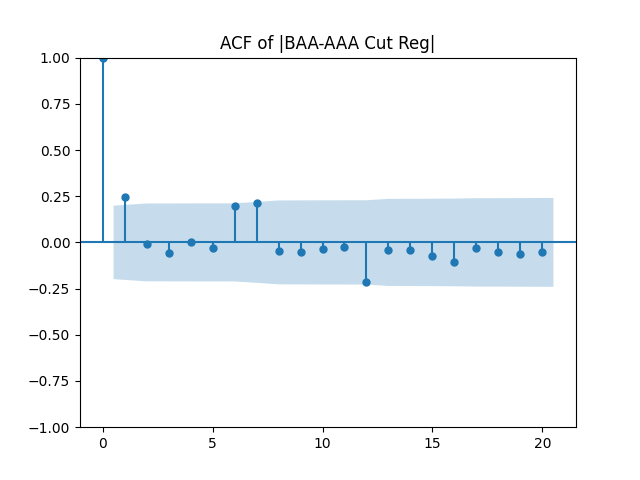

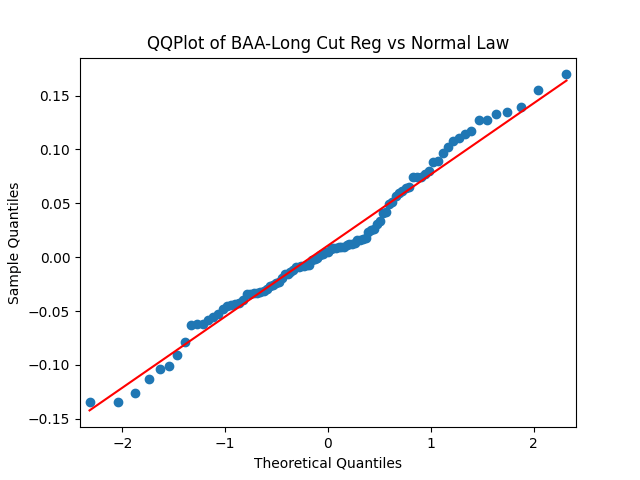

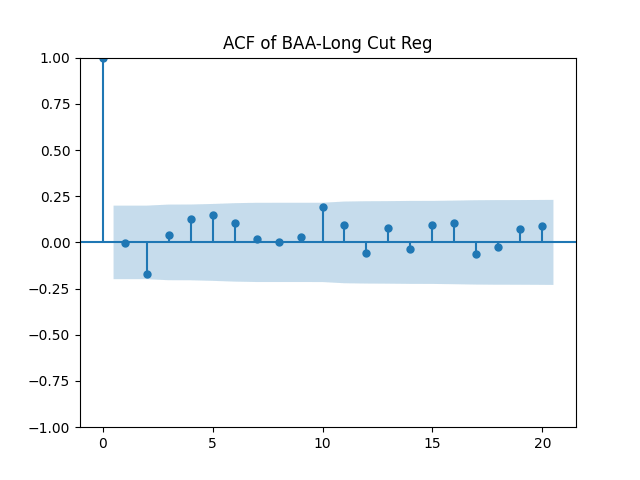

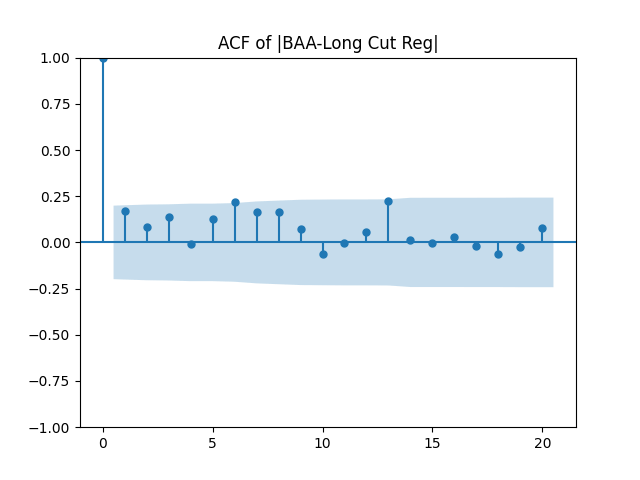

Results: Unfortunately, innovations here are further from Gaussian than in the previous post. Judging by the autocorrelation function plots for these innovations and for their absolute values: Yes, we can model

| Innovations | Skewness (Gaussian = 0) | Kurtosis (Gaussian = 0) | Shapiro-Wilk p-value | Jarque-Bera p-value | L1 norm for 5 lags ACF of original values | L1 norm for 5 lags ACF of absolute values |

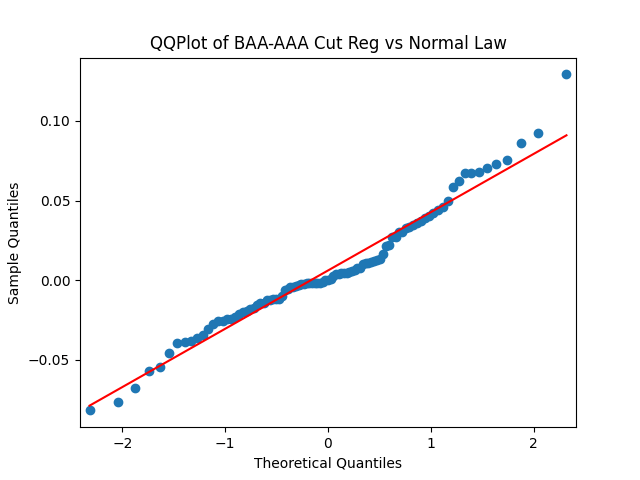

| BAA-AAA | 0.714 | 0.847 | 0.2% | 0.4% | 0.45 | 0.605 |

| BAA-Long | 0.631 | 0.181 | 1.0% | 3.7% | 0.554 | 0.487 |

We recall that the threshold 95% value for the L1 statistic is around 63%, based on Monte Carlo simulations.

Dependence upon volatility

Removing intercepts: If we do the vector model above without

| Innovations | Skewness (Gaussian = 0) | Kurtosis (Gaussian = 0) | Shapiro-Wilk p-value | Jarque-Bera p-value | L1 norm for 5 lags ACF of original values | L1 norm for 5 lags ACF of absolute values |

| BAA-AAA | 0.5 | 0.819 | 2.8% | 3.4% | 0.375 | 0.342 |

| BAA-Long | 0.204 | -0.203 | 15.9% | 65.8% | 0.489 | 0.528 |

The p-values for Student T-test for BAA-AAA with factor BAA-Long is 32.3% and the other way around is 43%. In principle, we could model these two spreads as separate autoregressions of order 1, but with correlated innovations.

Conclusion: For bivariate vector autoregression of order 1 applied to BAA-AAA and BAA-Long spreads, dividing innovations by volatility makes them independent identically distributed Gaussian. After that, adding this volatility as a factor in a linear regression improves the fit as judging by significant dependence, and keeps innovations independent identically distributed, but destroys their normality.

Leave a comment