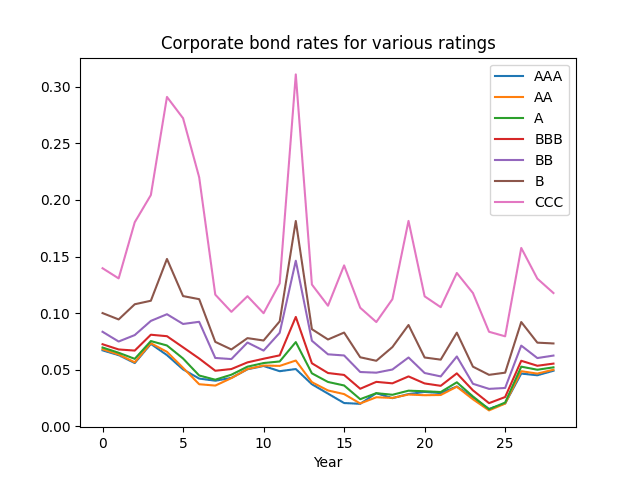

Here we use annual volatility to model bond rates: annual, end-of-year 1996-2024. We take Bank of America bond portfolios with the following seven rates: AAA, AA, A, BBB (investment-grade) and BB, B, CCC (junk, high-yield). Data and code are available on GitHub/asarantsev depository Annual-Bank-of-America-Rated-Bond-Data.

First, consider the rate on the last day of years 1996-2024. Below is the graph of them.

Let

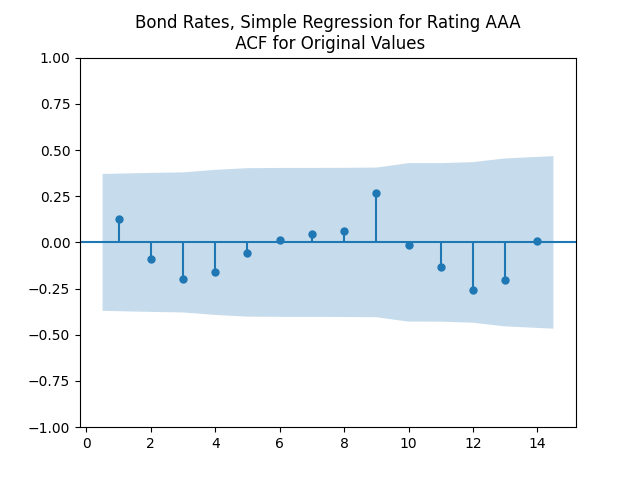

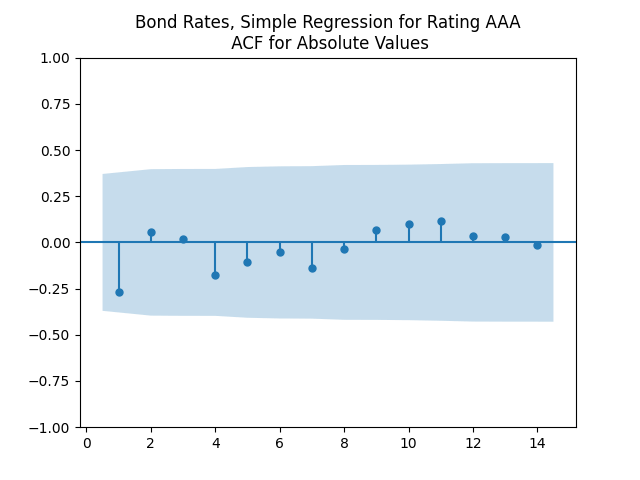

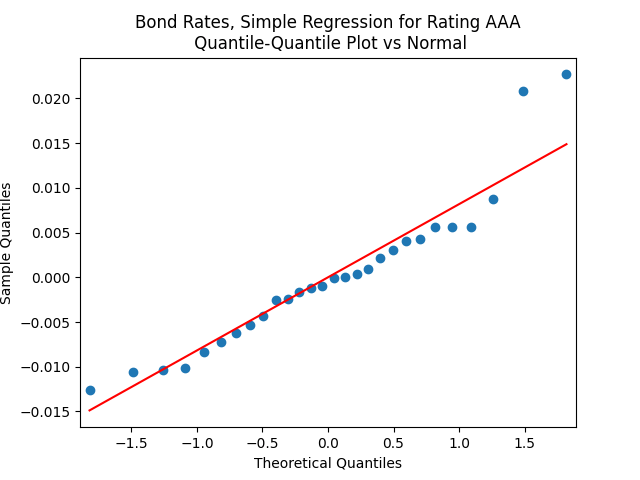

And the results are available in the table below. The last three columns are: Autocorrelation function for innovations, sum of absolute values of the first 5 lags (ACFO); same but for absolute values of innovations (ACFA); Pearson test for

| Rate |  |  | Stdev of residuals | Skew | Kurtosis | Shapiro-Wilk  | Jarque-Bera | ACFO | ACFA | Pearson Test |

| AAA | -0.21 | 0.0081 | 0.008 | 0.994 | 1.241 | 0.029 | 0.041 | 0.629 | 0.627 | 0.051 |

| AA | -0.23 | 0.0087 | 0.009 | 0.747 | 0.842 | 0.108 | 0.18 | 0.716 | 0.918 | 0.049 |

| A | -0.26 | 0.011 | 0.01 | 0.571 | 0.53 | 0.138 | 0.397 | 0.48 | 0.744 | 0.043 |

| BBB | -0.33 | 0.017 | 0.012 | 0.799 | 1.671 | 0.09 | 0.044 | 0.262 | 0.699 | 0.025 |

| BB | -0.46 | 0.031 | 0.02 | 1.479 | 3.951 | 0.007 | <0.001 | 0.482 | 0.814 | 0.009 |

| B | -0.57 | 0.048 | 0.026 | 1.612 | 3.629 | 0.003 | <0.001 | 0.366 | 0.727 | 0.003 |

| CCC | -0.57 | 0.082 | 0.055 | 1.338 | 2.051 | 0.007 | 0.001 | 0.576 | 0.626 | 0.004 |

The autocorrelation function (ACF) plots for

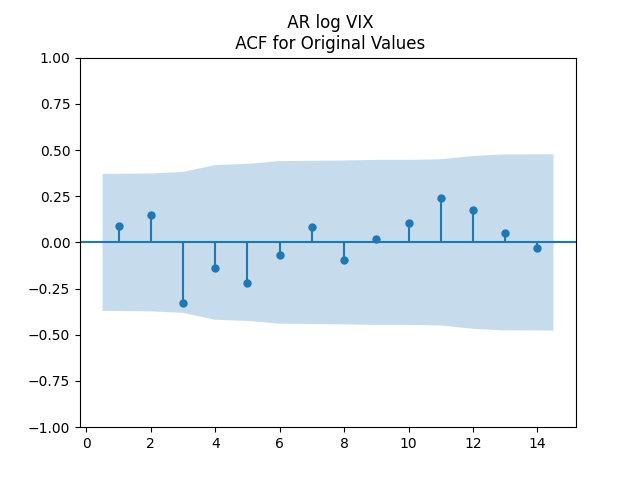

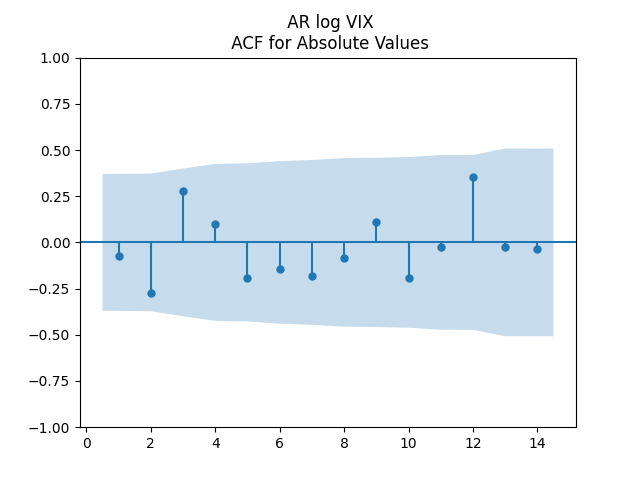

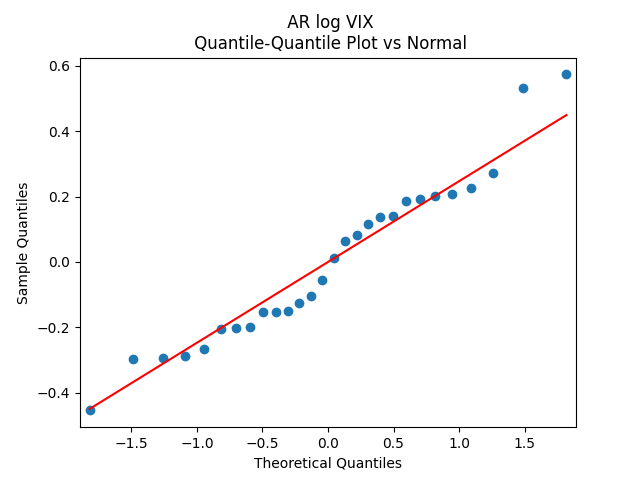

As usual, we can improve fit and make innovations Gaussian by dividing them by annual volatility. Now we take average annual VIX instead of monthly. This parallels research by Angel Piotrowski mentioned in previous posts. But she computed annual realized volatility, and I use averaged VIX (implied volatility). Let us first fit the log Heston model for VIX 1996-2024:

Here,

Consider the autoregression with normalization of innovations

Divide by VIX and then get an ordinary least squares regression with residuals

Results are available below in the table: Coefficients and analysis of innovations

| Rate |  | |  | Stdev | Skew | Kurt | S-W | J-B | ACFO | ACFA |

| AAA | 0.01 | -0.14 | -2.41 | 0.00037 | 0.774 | 0.664 | 22% | 19% | 0.352 | 0.816 |

| AA | 0.0099 | -0.116 | -2.78 | 0.0004 | 0.67 | 0.807 | 43% | 24% | 0.402 | 0.924 |

| A | 0.0087 | -0.157 | -1.06 | 0.00044 | 0.342 | 0.2 | 93% | 74% | 0.395 | 0.963 |

| BBB | 0.0099 | -0.279 | -2.1 | 0.00051 | 0.039 | -0.4 | 96% | 91% | 0.405 | 0.779 |

| BB | 0.015 | -0.539 | 10.0 | 0.00076 | 0.303 | -0.21 | 88% | 79% | 0.656 | 0.594 |

| B | 0.0235 | -0.77 | 20.3 | 0.00096 | 0.35 | -0.126 | 46% | 74% | 0.576 | 0.722 |

| CCC | 0.0217 | -0.73 | 41.5 | 0.00198 | 0.58 | 0.25 | 36% | 44% | 0.817 | 0.948 |

All correlation between

Thus we see a joint model: For

![(W(t), \varepsilon(t)) \sim \mathcal N_2([0, 0], \Sigma)](https://s0.wp.com/latex.php?latex=+%28W%28t%29%2C+%5Cvarepsilon%28t%29%29+%5Csim+%5Cmathcal+N_2%28%5B0%2C+0%5D%2C+%5CSigma%29+&bg=ffffff&fg=000&s=0&c=20201002)

As discussed, we might consider

In our previous research, we proved long-term stability of this bivariate model. This is true not just for Gaussian innovations, but for more general cases, under certain conditions.

We continue this research in the next post, where we model total returns.

Leave a reply to Investment-Grade Corporate Bond Returns 1972-2024 – My Finance Cancel reply