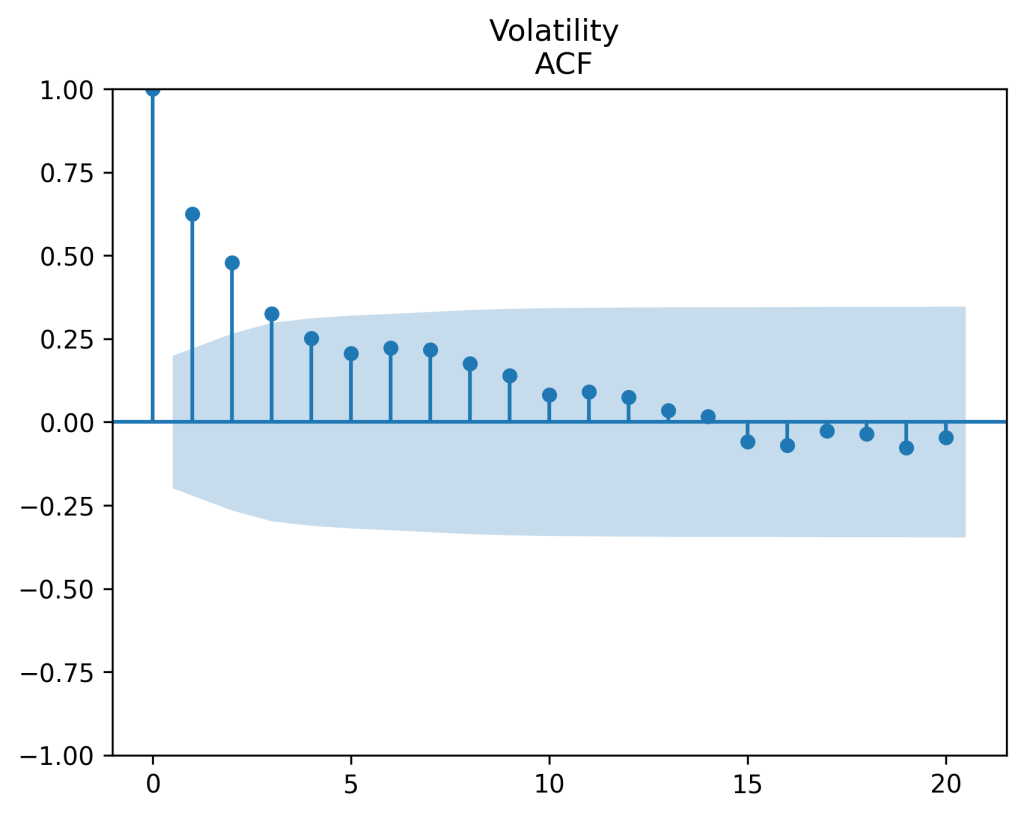

My undergraduate student Angel Piotrowski updated annual realized volatility for 2024. Previously she computed it for 1928-2023, each year. She took log change in daily closing prices of the Standard & Poor 500, or its predecessor, Standard & Poor 90, and computed empirical standard deviation. Given this annual volatility data

This strongly suggests using the autoregression model, which is called the Heston model in quantitative finance:

Results after fitting this simple linear regression using ordinary least squares method are:

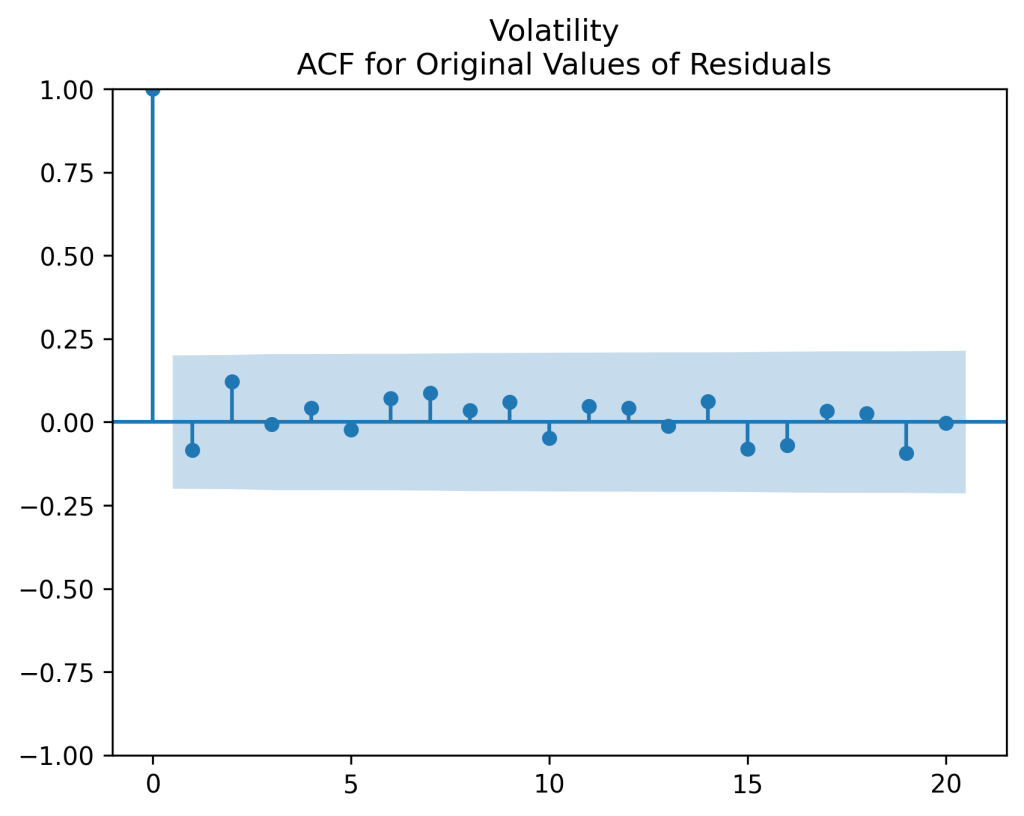

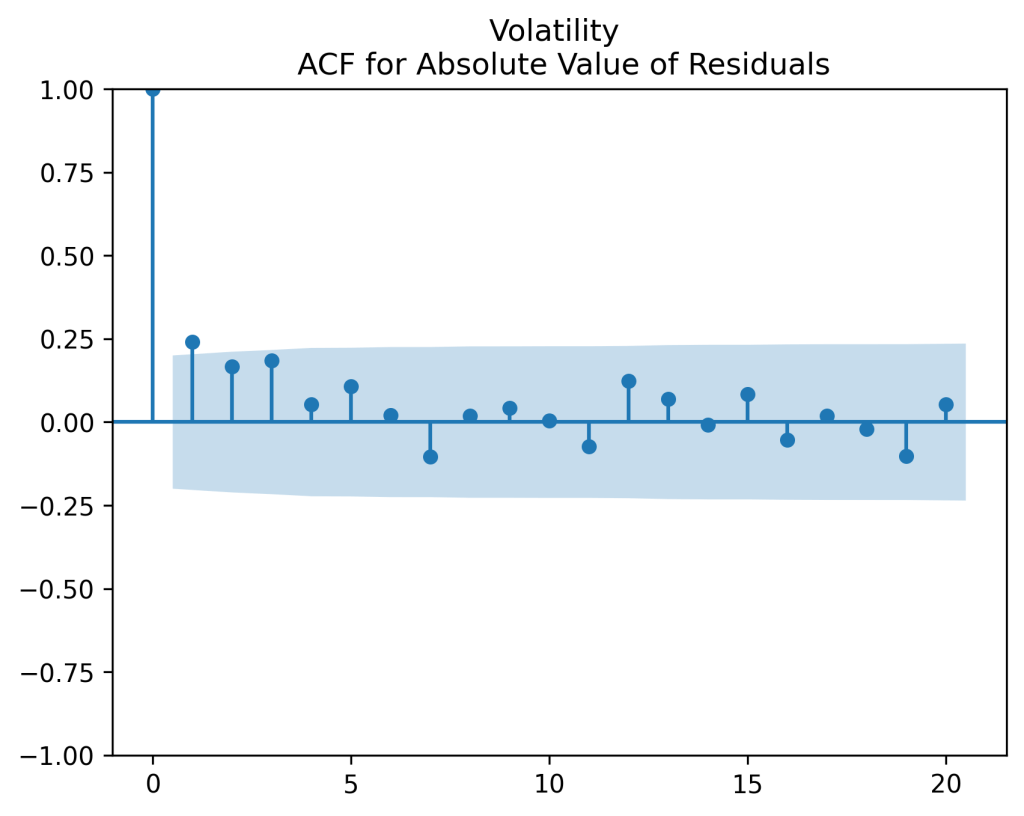

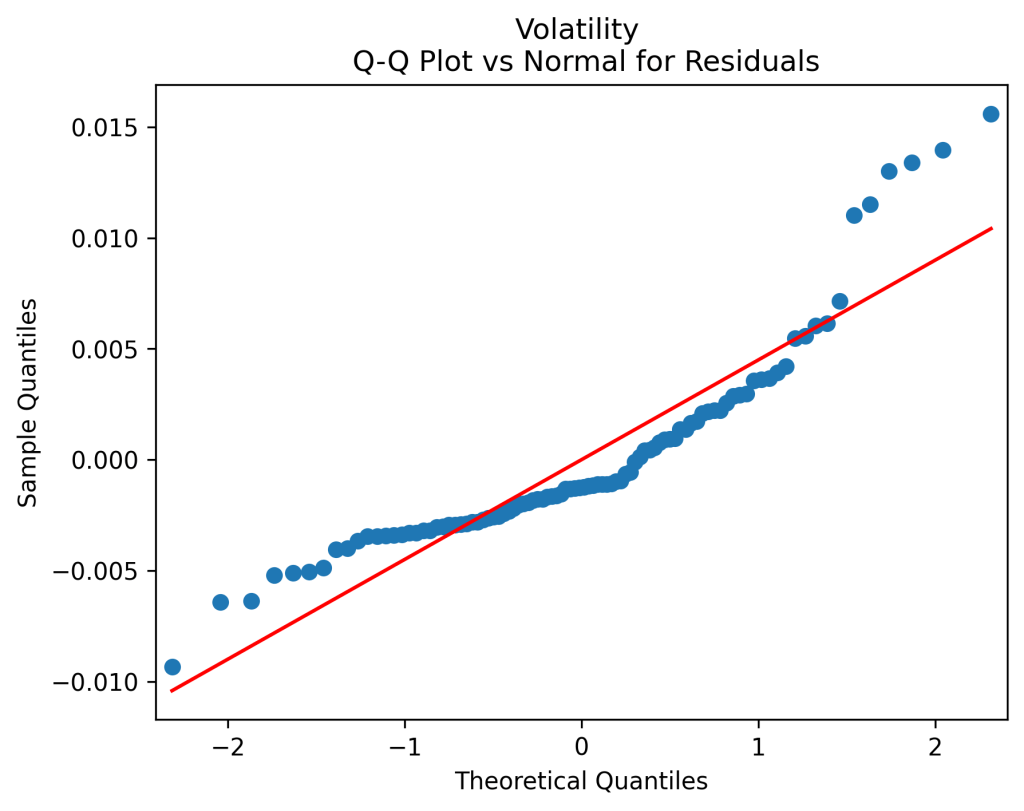

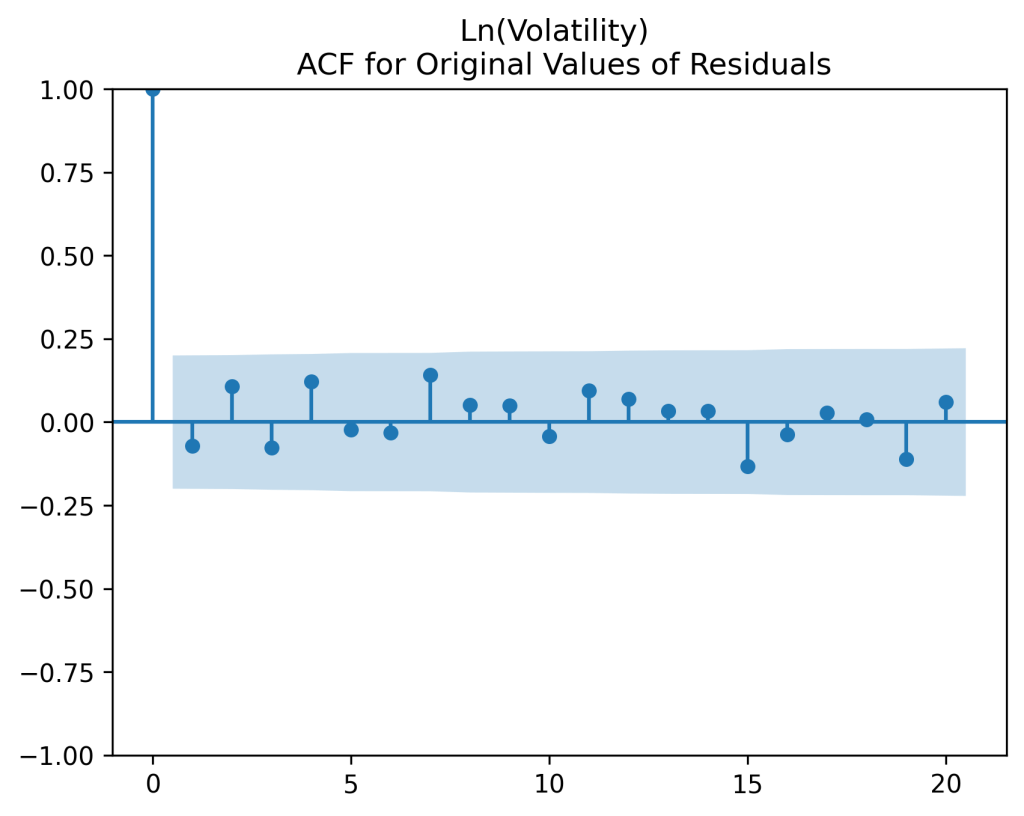

Now let us analyze residuals (innovations)

We see that the ACF plot for

Yet another problem with this Heston model: Volatility can go negative according to this model, but this is impossible in real life. As a standard deviation of market fluctuations, volatility is always supposed to stay positive.

Next, Angel modeled the resulting series

For updated data,

See the autocorrelation function plots for innovations

The resulting stationary distribution

![\mathbb E[V(\infty)] = 0.0104](https://s0.wp.com/latex.php?latex=+%5Cmathbb+E%5BV%28%5Cinfty%29%5D+%3D+0.0104+&bg=ffffff&fg=000&s=0&c=20201002)

Updated data for 1928-2024 volatility, nominal and real returns, and index prices, can be found on my web site

The code and data for the current post can be found on https://github.com/asarantsev/Annual-Volatility

Leave a reply to Investment-Grade Corporate Bond Returns 1972-2024 – My Finance Cancel reply