In the last few days, I did a lot of research.

In the previous blog post, I have written about the simulator using only one factor: annual volatility, and two equations: for volatility and for total returns. Annual volatility was computed by my undergraduate student Angel Piotrowski as realized standard deviation of daily price returns. I multiplied it by 1000 for normalizing.

Our Model: Here, I extended it to two factors: annual volatility and annual earnings. Previously, annual earnings growth was modeled by another undergraduate student Ian Anderson. We have four equations:

- Autoregression of order 1 for logarithmic volatility

- Earnings growth divided by volatility as IID

- Price returns (excluding dividends) as linear regression with innovations = IID times volatility

- Total returns (including dividends) as linear regression with innovations = IID times volatility

These two regressions have factors: this year’s volatility and previous year’s earnings yield: last year’s earnings divided by end of last year’s index. This earnings yield is the classic valuation measure used by financial practitioners.

This model has two versions for the last three equations: nominal (not inflation-adjusted) and real (inflation-adjusted). We use four series of innovations which are multivariate Gaussian:

Volatility:

Earnings growth:

Price returns:

Total returns:

Regression Results: Below is the table. We see that coefficients

Presumably this low prediction value is because of high volatility of earnings. For example, in 2008 earnings plummeted so much that the yield plummeted as well, thus making the markets seem overvalued. But in reality, they were undervalued, since earnings rebounded fast, and it took the markets an entire decade to rebound.

| Point Estimate | 95% Confidence Interval | p-value for Student test | |

Real Returns  | 0.1655 | [0.064, 0.267] | 0.002 |

Real Returns  | -0.0141 | [-0.024, -0.005] | 0.004 |

Real Returns  | 0.1453 | [-0.903, 1.194] | 0.784 |

Real Returns  | 0.1668 | [0.068, 0.265] | 0.001 |

Real Returns  | -0.0136 | [-0.023, -0.004] | 0.004 |

Real Returns  | 0.5494 | [-0.465, 1.564] | 0.285 |

| Nominal Returns | 0.1693 | [0.074, 0.264] | 0.001 |

| Nominal Returns | -0.0133 | [-0.022, -0.004] | 0.003 |

| Nominal Returns | 0.4432 | [-0.537, 1.424] | 0.372 |

| Nominal Returns | 0.1706 | [0.079, 0.262] | 0.000 |

| Nominal Returns | -0.0127 | [-0.021, -0.004] | 0.004 |

| Nominal Returns | 0.8473 | [-0.097, 1.792] | 0.078 |

Normality: Skewness, kurtosis, and normality tests (Shapiro-Wilk and Jarque-Bera) show that residuals for price and total returns are Gaussian. However, evidence for normality of earnings growth normalized by volatility; or, equivalently, residuals

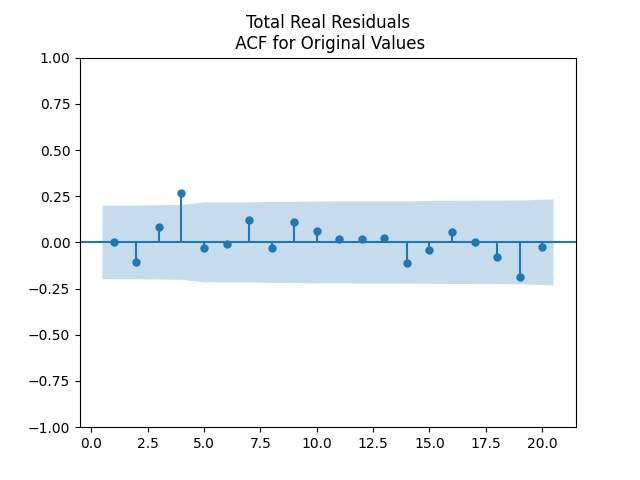

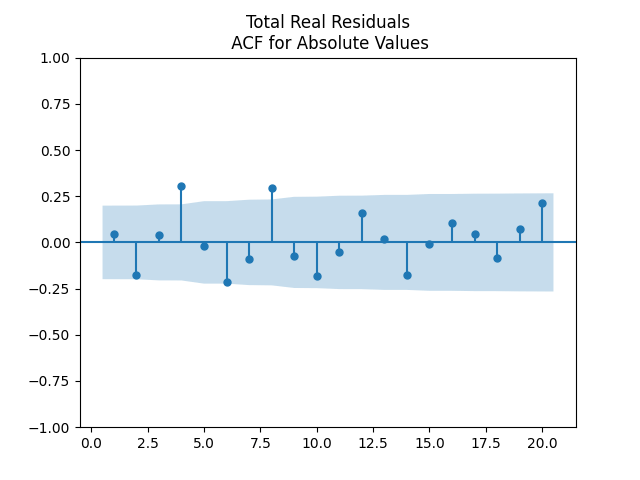

Independence: We show below the autocorrelation functions for original values of residuals:

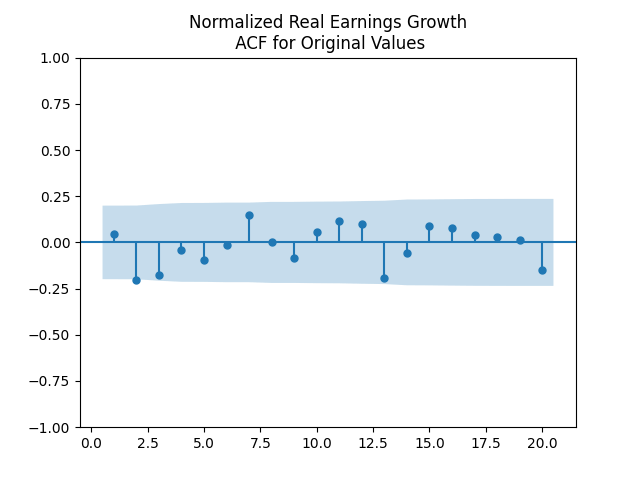

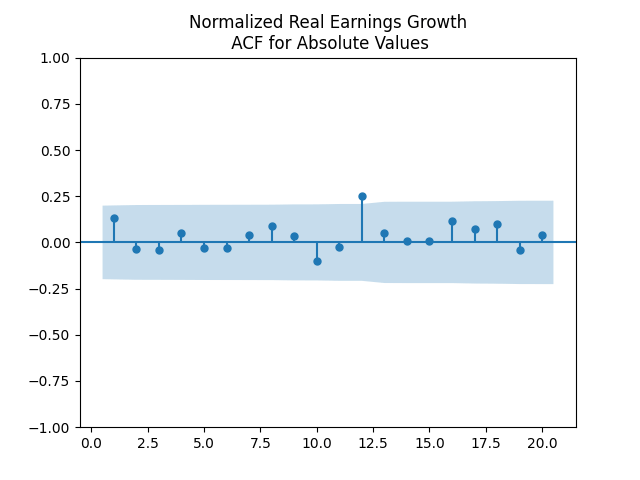

Next, the autocorrelation function plots for nominal and real growth terms show that these can indeed be modeled by IID. We show plots for real earnings growth. Nominal earnings growth have similar autocorrelation plots.

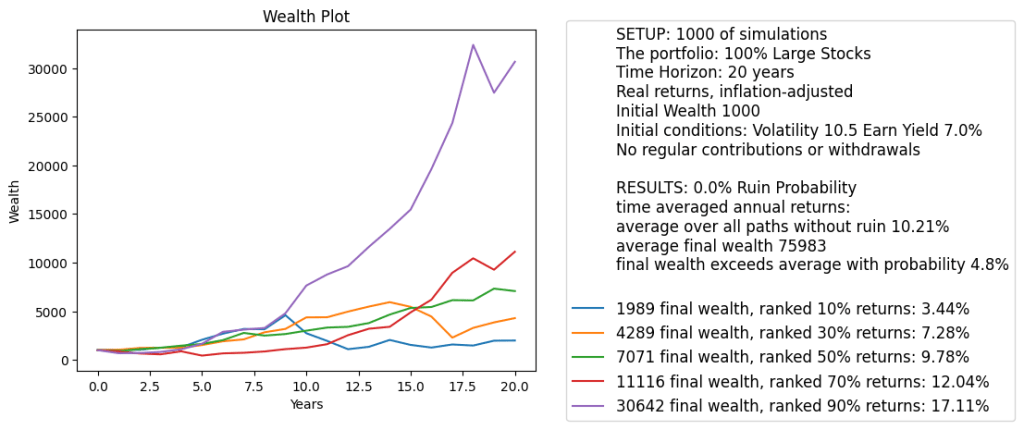

Simulation. We built a version of the financial simulator which has inputs: initial volatility, initial earnings yield, and time horizon in years. We also allow, as usual, annual contributions or withdrawals. We allow for nominal (not inflation-adjusted) or real (inflation-adjusted) versions. The code and data are available on GitHub/asarantsev repository earnings-yield-annual-simulator. We see the graph of total wealth below. This graph also shows:

- No contributions or withdrawals

- Real returns

- 20 years time horizon

- Initial volatility: 10.5 (close to historical average)

- Initial earnings yield: 7% (close to historical average)

We see that average returns over time and all simulations is 10.21%. This is much higher than historical average returns: 6.7%. This presents a problem: If we start with average data, then we should reproduce historical average returns over many simulations. We also see that with high probability returns are very large: the 90% quantile is 17.11%.

Finally, plot earnings yields for the five chosen simulations. We see that yields can become very high. In two simulations out of five, we have yields greater than 30%. Yields like this do not happen in real life.

What is the reason? We think it is because we have exponential terms in the time series equation for earnings yield

Take the equations for earnings growth and price returns at the beginning of this post. Plug them into the above equation:

The change in

Conclusion: We think this makes our research financially unrealistic, despite rigorous statistical analysis. A better way might be to use the CAPE or its inverse, cyclically adjusted earnings yield (using the last few years average for earnings instead of only last year). Another way might be to reproduce my research on the new valuation measure.

Leave a reply to S&P 500 Annual Returns with CAPE and Volatility – My Finance Cancel reply