A continuation of research in github.com/asarantsev repository Annual-Bank-of-America-Rated-Bond-Data from my previous post. Consider total returns

If these were Treasury bonds and there were no risk of default, and if these were zero-coupon bonds (with only principal payment at maturity) then total returns would be equal to the rate minus maturity times rate change. See my manuscript arXiv:2411.03699. The equation is:

The maturity is given in the following table, together with analysis of residuals: skewness, kurtosis, Shapiro-Wilk and Jarque-Bera normality test

| Rating |  | Skewness | Kurtosis | Shapiro-Wilk | Jarque-Bera | ACF of  | ACF of  |

| AAA | 6.03 | -2.049 | 5.173 | 0.014% | <0.001% | 0.539 | 0.687 |

| AA | 4.89 | -0.941 | 1.154 | 2.549% | 5.831% | 0.944 | 0.874 |

| A | 4.94 | -0.894 | 1.307 | 7.877% | 5.726% | 0.977 | 0.704 |

| BBB | 5.17 | -0.573 | 0.027 | 25% | 46% | 0.38 | 0.604 |

| BB | 3.81 | -1.75 | 3.64 | 0.054% | <0.001% | 0.83 | 0.245 |

| B | 3.12 | -2.036 | 4.323 | 0.003% | <0.001% | 1.17 | 0.653 |

| CCC | 2.55 | -2.304 | 5.34 | 0.001% | <0.001% | 0.9 | 0.716 |

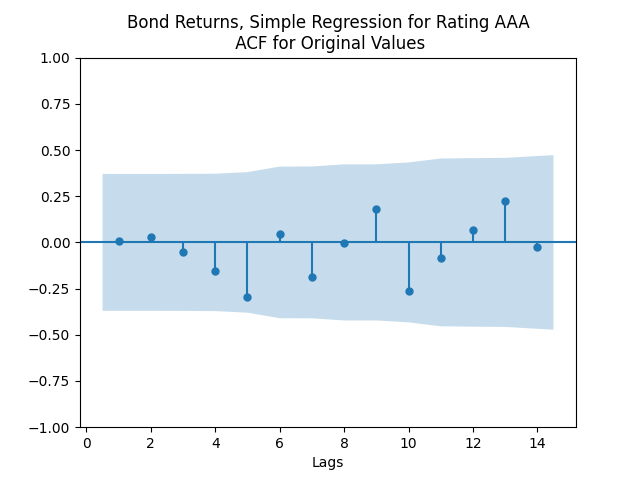

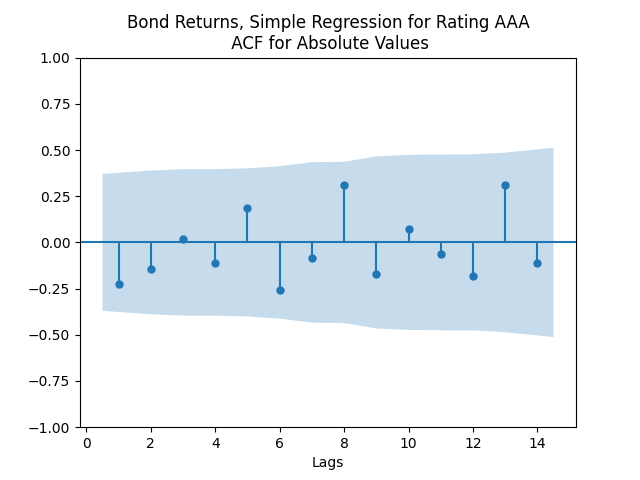

The autocorrelation function plots for

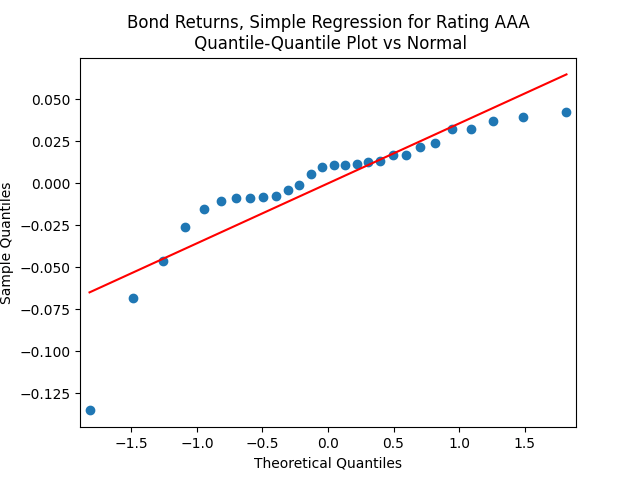

This is confirmed by the results of Shapiro-Wilk and Jarque-Bera tests, shown in the table above.

Apply the same technique as in the previous post: Normalize residuals by dividing them by annual average VIX. We get:

Coefficient estimates and analysis of innovations

| Rating |  | |  | Skewness | Kurtosis | Shapiro-Wilk | Jarque-Bera | ACF of | ACF of |

| AAA | 0.0661 | 7.0787 | -0.0034 | -0.737 | 0.576 | 28% | 23% | 0.922 | 0.361 |

| AA | 0.0453 | 5.3226 | -0.0023 | 0.126 | -0.039 | 46% | 96% | 0.57 | 0.761 |

| A | 0.0423 | 5.3423 | -0.0022 | -0.181 | 0.02 | 35% | 93% | 0.73 | 0.459 |

| BBB | 0.0293 | 5.6074 | -0.0016 | -0.232 | -0.775 | 67% | 62% | 0.875 | 0.498 |

| BB | 0.0422 | 3.6671 | -0.0024 | -0.894 | 1.426 | 19% | 6.3% | 0.574 | 0.888 |

| B | 0.0682 | 2.9970 | -0.0050 | -1.562 | 3.479 | 0.397% | <0.001% | 0.998 | 0.354 |

| CCC | 0.0712 | 2.6532 | -0.0075 | -1.588 | 2.649 | 0.072% | 0.005% | 0.835 | 0.723 |

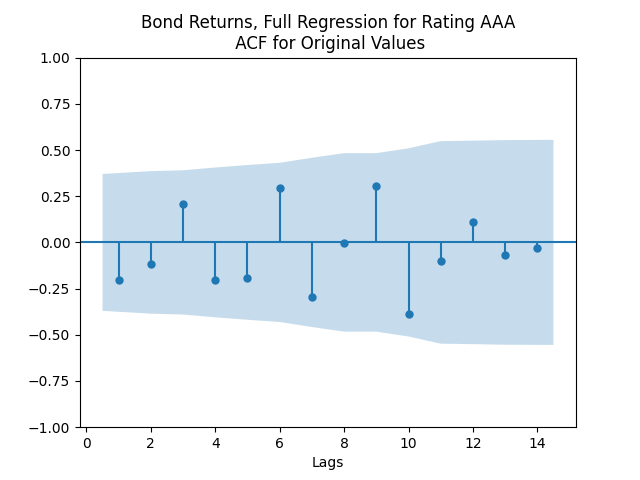

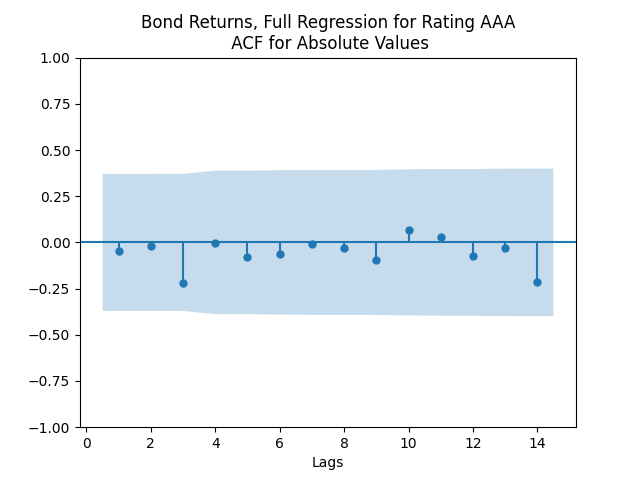

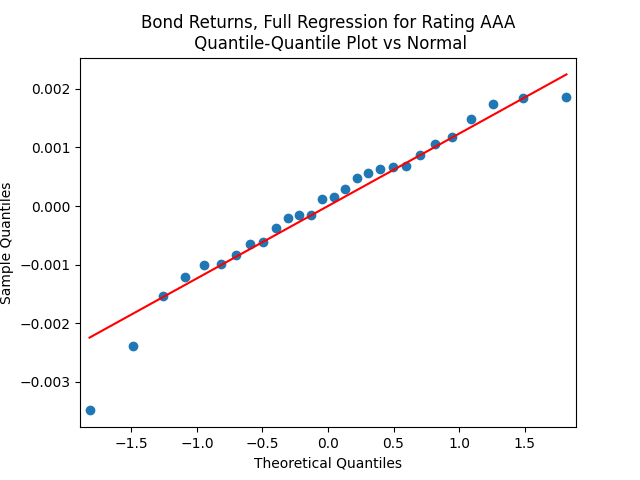

We see the residuals can be well described as Gaussian white noise for ratings BB and higher, especially well for investment-grade bonds. But for B and CCC ratings, not so much. However, judging by the ACF, new residuals (see the second table) are comparable to old residuals (see the first table) in being close to independent identically distributed. See also the following plots for AAA rated bonds:

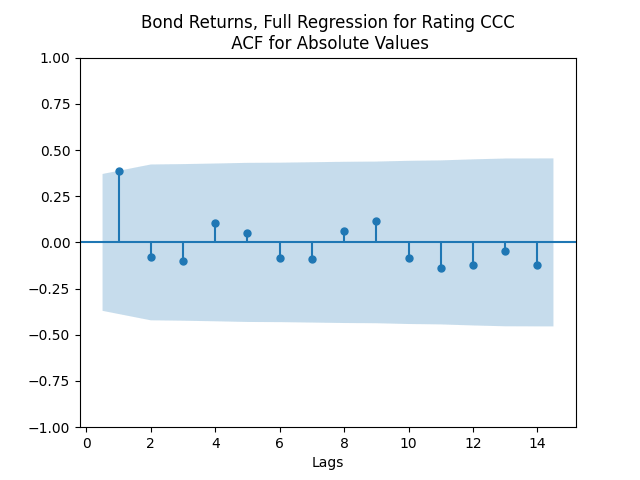

And for the lowest-rated CCC bonds the situation is different: We see that the first lag is quite significant for both version of the autocorrelation function.

Combining the model above with the results of the previous post, we get the trivariate model:

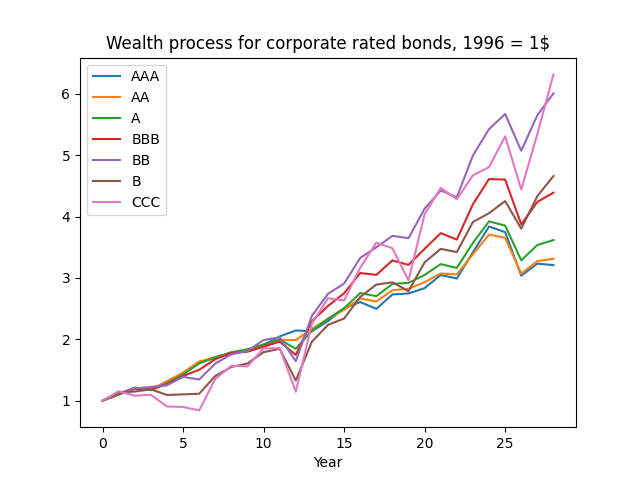

And the wealth process is given by

Next, for ratings BB and above, the trivariate innovations sequence

Leave a reply to Investment-Grade Corporate Bond Returns 1972-2024 – My Finance Cancel reply