My undergraduate student Angel Piotrowski continued her work, started with annual volatility 1928-2023. First, she updated the annual realized volatility for 2024. The resulting series 1928-2024 is still well modeled by log Heston model, see another post. The research in this post is done in GitHub/asarantsev repository.

Then she computed annual returns of S&P 500 (and its predecessor, S&P 90) 1928-2024 in four versions:

- nominal (not adjusted for inflation) or real (adjusted for inflation);

- price (due only to price changes) or total (including dividends paid).

We take nominal annual dividend:

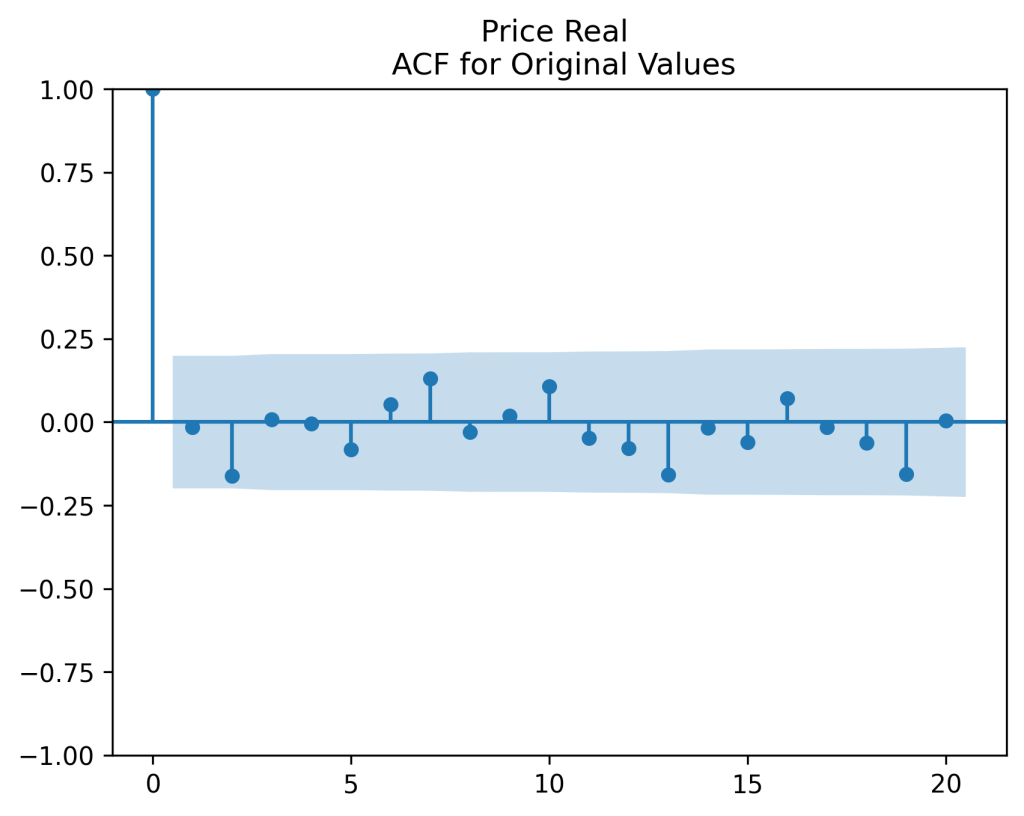

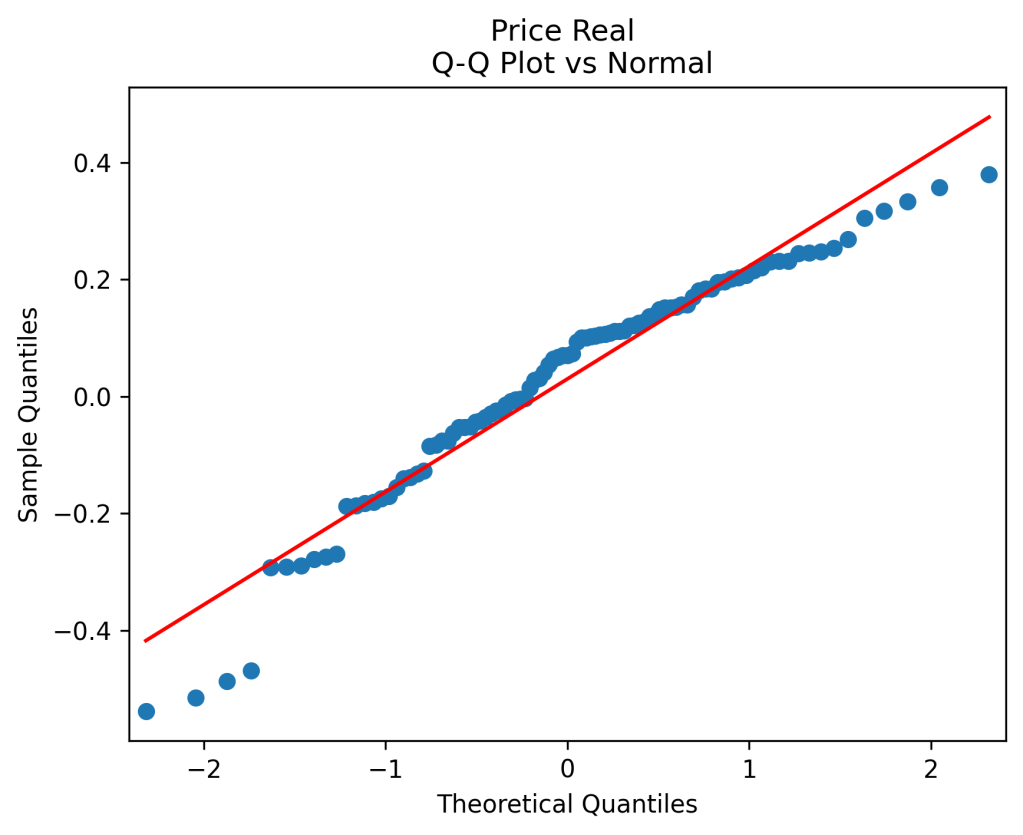

In each of these four cases, returns are IID but not normal. However, dividing them by volatility keeps them IID but makes them normal. Just to illustrate, let us take real price returns

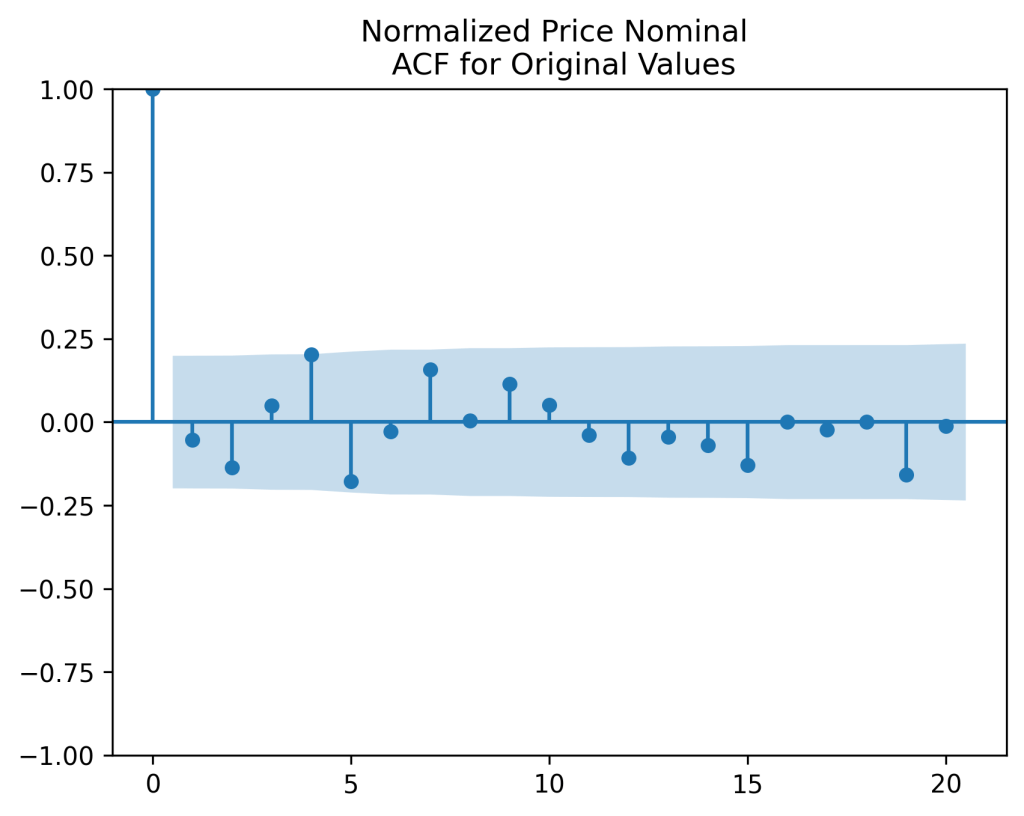

The autocorrelation function for

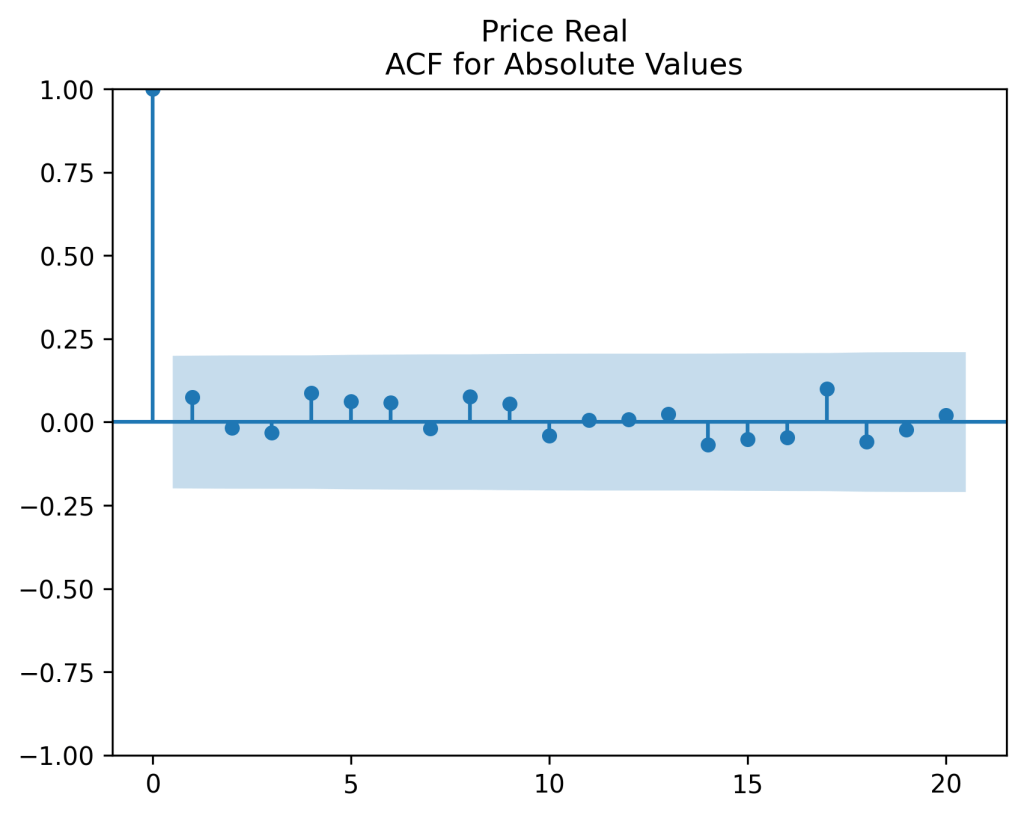

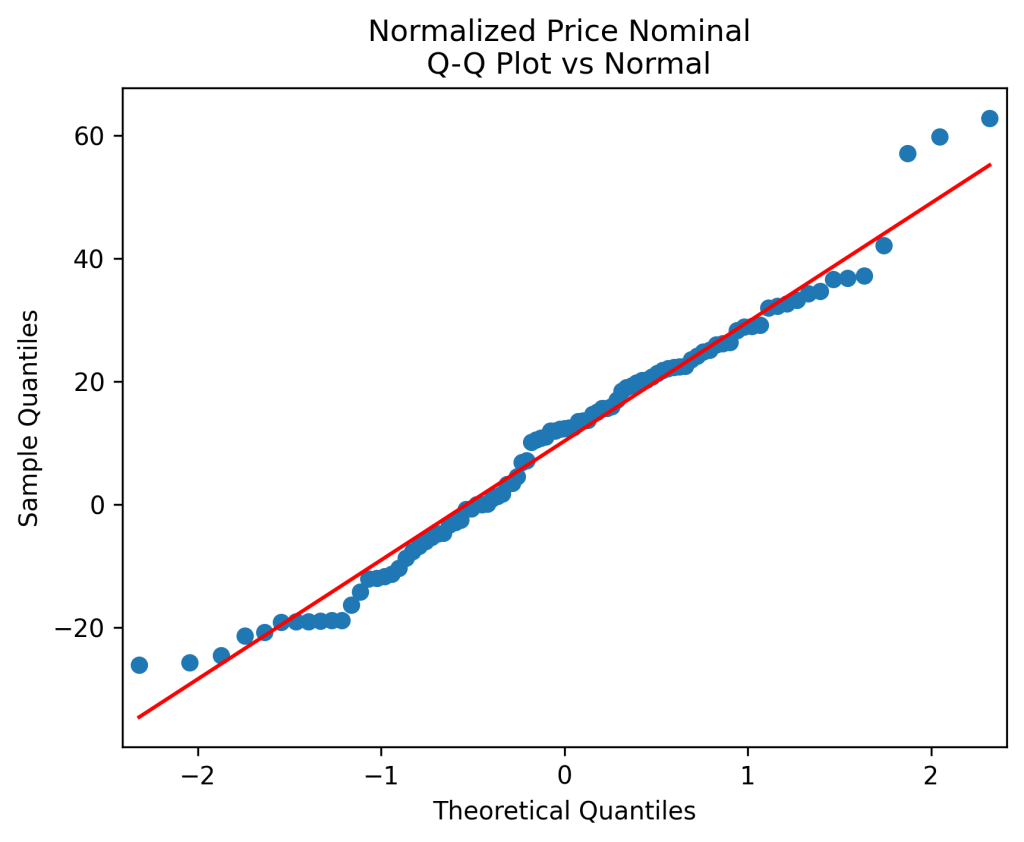

Next, repeat this analysis for normalized

And see that

This is confirmed by results of two statistical tests for normality: Shapiro-Wilk and Jarque-Bera. See their

| Returns | Original Total Real | Normd Total Real | Original Total Nominal | Normd Total Nominal | Original Price Real | Normd Price Real | Original Price Nominal | Normd Price Nominal |

| Shapiro-Wilk p | 0.00164 | 20% | 0.00027 | 11% | 0.00087 | 28% | 0.00009 | 11% |

| Jarque-Bera p | 0.00627 | 63% | 0.00005 | 60% | 0.00217 | 86% | 0.00000 | 60% |

Leave a reply to Updated Simulator for Rate and Volatility – My Finance Cancel reply