This work was done by my undergraduate student Ian Anderson, using the volatility data computed by my other undergraduate student Angel Piotrowski, see the previous post.

Ian took 1927-2023 net earnings of Standard & Poor 500 (since 1957; or its predecessor Standard & Poor 90)

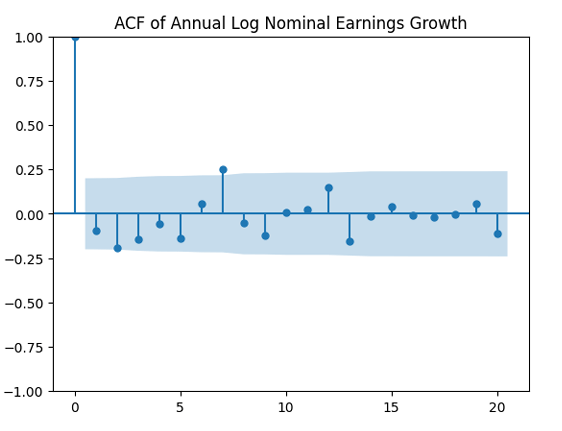

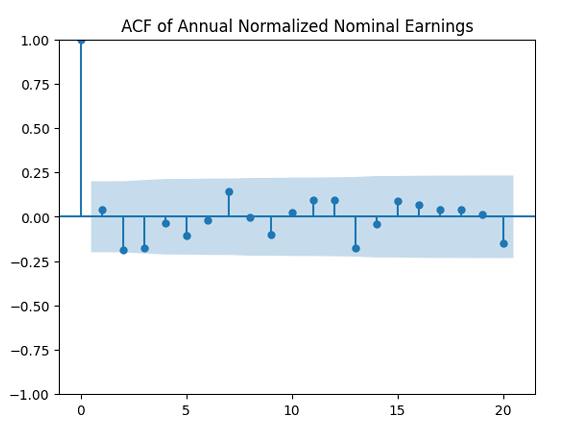

And we plot the autocorrelation function for

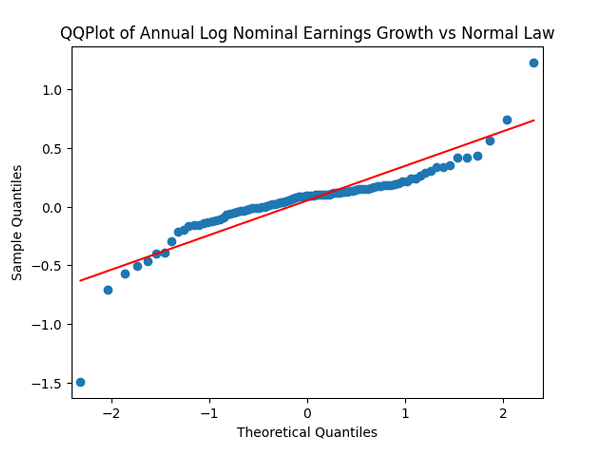

We see from the QQ plot that, unfortunately, earnings growth terms are not Gaussian. The autocorrelation function for earnings growth corresponds to white noise: It shows that

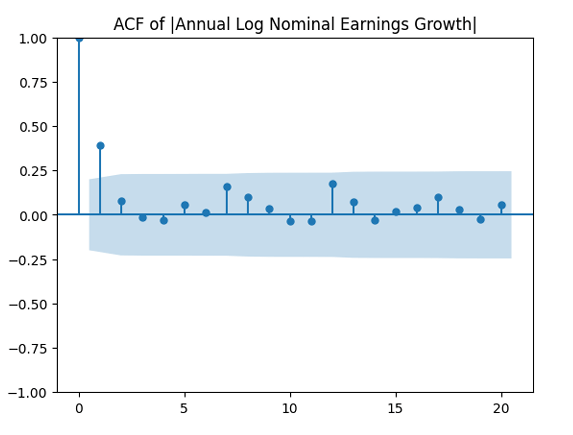

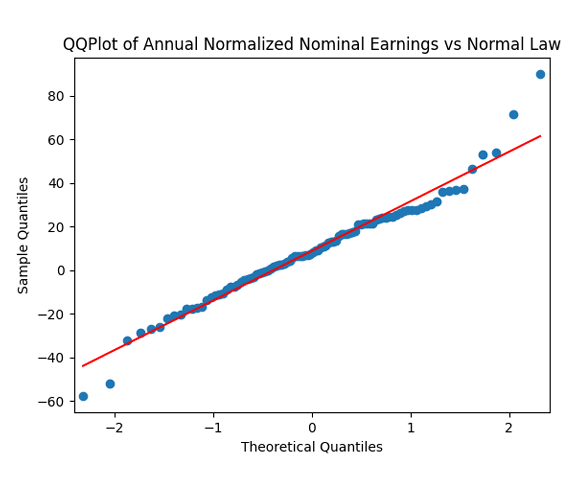

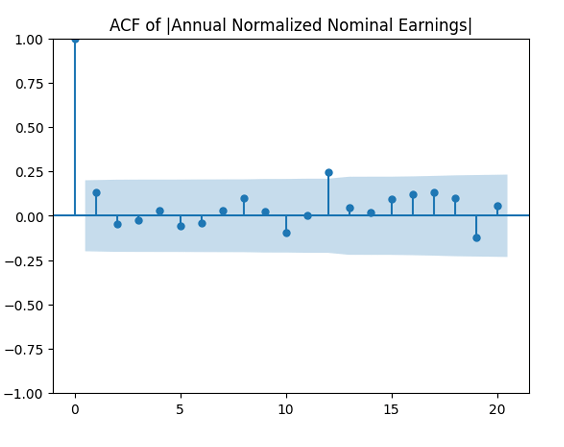

Then divide the earnings growth by annual volatility and get

We see that now both autocorrelation plots show lack of significant autocorrelations. And the quantile-quantile plot is much closer to linear. Thus it makes sense to model

The same happens if we consider real earnings (inflation-adjusted) instead of nominal earnings, using December data for the Consumer Price Index. Thus we have joint model for earnings and volatility, annual 1927-2023:

![(W(t), Z(t)) \sim \mathcal N_2([0, 0], \Sigma)](https://s0.wp.com/latex.php?latex=+%28W%28t%29%2C+Z%28t%29%29+%5Csim+%5Cmathcal+N_2%28%5B0%2C+0%5D%2C+%5CSigma%29+&bg=ffffff&fg=000&s=0&c=20201002)

Leave a reply to Growth/Volatility vs Spreads – My Finance Cancel reply