A financial econometrician often hopes against hope that returns exhibit the following properties: (A) normal, following the bell curve; (B) IID, meaning independent identically distributed. Unfortunately, this is almost never true.

Here, let me describe a nifty trick: Dividing each data point by the standard deviation normalizes the data. The standard deviation of stock market returns (in financial econometrics this is called volatility) is not constant over time. Periods of economic calm and steady growth when volatility is small alternate with economic crises and financial crashes when volatility is large. It is not clear that dividing by overall volatility makes sense.

Another way to say is that volatility is stochastic: It is a random process by itself. How to extract this stochastic volatility, and how to model it? Here autoregressive conditional heteroscedastic (ARCH/GARCH) models are very useful. They model dependence of current volatility upon the past volatility and returns, with fixed number of lags. These are widely used in Quantitative Finance, often combined with classic linear autoregressive and moving average (ARMA) models. Every time series of returns would have

By chance, we discovered another trick, which obviates the need for GARCH-type models and allows to simply reduce all it to a couple of linear regressions. The miracle is that we can observe volatility independently and separately from the main time series!

Enter VIX, the index created and maintained by the Chicago Board of Options Exchange. Options are contracts which give the holder the right (but not the obligation) to buy or sell a stock or a stock index in the future (at a maturity) at a predetermined price (the strike). The celebrated Black-Scholes formula computes the option price based on current stock price, the strike price, the maturity, and the volatility.

Lost of options are traded in Chicago based on S&P 500. Comparing the market price of each option at a given moment, we solve the Black-Scholes formula backward and find the unknown volatility. This is called the implied volatility. Taking a weighted average of all options, we get the overall implied volatility of the index, which is called VIX. It was computed daily for S&P 500 from the start of 1990, and for S&P 100 (a subset of S&P 500) from 1986.

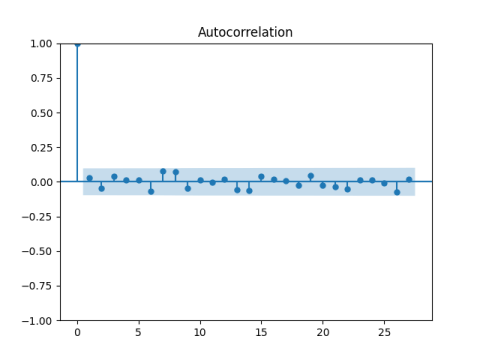

Below is the ACF plot. Take monthly returns of Wilshire Total Stock Market Index, including dividends, from 1990. Below is the plot of their autocorrelation (correlation between month

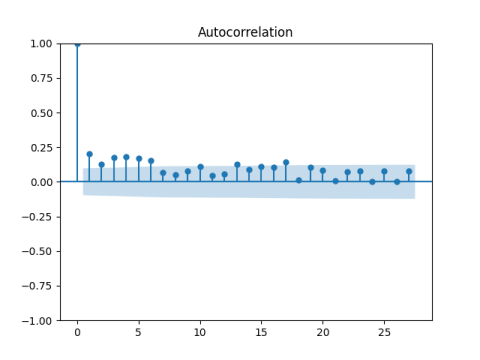

However, if we take autocorrelations for the absolute values, this is not IID anymore!

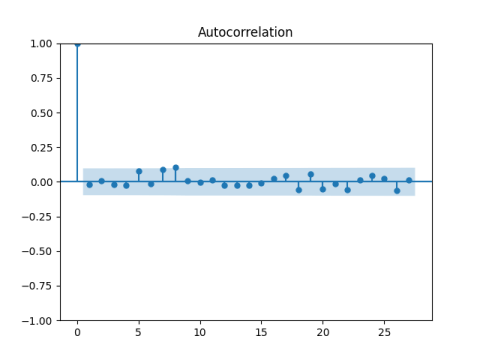

Finally, if we divide total returns by monthly average VIX, we get the autocorrelation functions for returns to be well-behaved, that is, corresponding to IID.

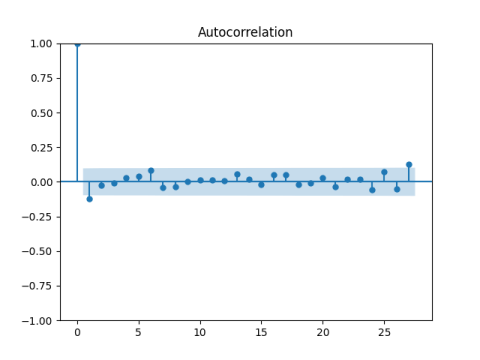

And for their absolute values as well.

We can have

We discussed in the last post the model

When analyzing financial and economic data, one should always be mindful of this possibility. If we checked autocorrelation for both

We can also apply white noise tests to

Consider correlations of

Doing the same for

I created combined test (omnibus or portmanteau) to test

Moreover, it makes them normal, or much closer to normal than originally! This is true by statistical tests of normality (Shapiro-Wilk, Jarque-Bera, or others) and by the quantile-quantile plot (QQ) vs the normal law.

Finally, these properties work for any well-diversified factor market portfolio: Small, Value, Large Growth, and so on. VIX was created from S&P 500 options, but it works for indices, portfolios, and funds other than S&P 500.

Of course, the mean, variance, and other statistics of normalized returns will be different for two different portfolios. But normality and independence stay.

Portfolios are many, but volatility is universal!

Leave a reply to Financial Simulator, Current Version – My Finance Cancel reply