There are three S&P indices: Large-Cap 500, Mid-Cap 400, Small-Cap 600. These have exchange-traded funds (ETFs) by iShares. We use their monthly data to study equity premia: Total returns (including dividends) minus risk-free returns (measured by 3-month Treasury bill). As suggested previously, we divide these by monthly average volatility (measured by VIX) and get . Regress the last two upon the large to do Capital Asset Pricing Model: and . We get: are not significantly different from zero, so let us ignore them. But .

Thus investing in mid-cap and especially small-cap stocks creates a slightly larger market exposure than the benchmark S&P 500 but does not have extra return on top of the one predicted by this extra risk assumed.

The residuals are independent and identically distributed, judging by the autocorrelation function plot, and Gaussian for mid-cap but not for small-cap stocks. For the latter, they seem to be well-described by the Laplace distribution.

Let us do alpha-beta analysis (simple linear regression) of zero-dividend stocks upon dividend-paying stocks.

Consider monthly equity premia (total returns, including dividends, minus risk-free returns measured by 3-month Treasury rate). We subtract risk-free returns because this is the benchmark upon which we measure stock returns. Indeed, what good is it to get this year from risky stocks if you could get from risk-free Treasury bonds?

Let be the equity premium for zero-dividend stocks and let be the equity premium for dividend-paying stocks. Then , where are residuals. This implies that excess return for month and so for a year. And market exposure (for a month or a year). The . This makes the following financial sense:

When you invest in zero-dividend stocks, you expose yourself to more risk that dividend-paying stocks, since , but you lose per year. In fact, annualized equity premium for dividend stocks is and for zero-dividend stocks is . The annualized standard deviation for dividend stocks is and for zero-dividend stocks is . More risk, less reward!

Many of these zero-dividend stocks are startups. But historically, investing in startups is a recipe for trouble. Although individual IPOs outperform the market (Microsoft, Walmart, Starbucks, Amazon), on average they lag far behind. This is another argument for good old value investing.

is it better to invest in stocks with zero or negative recent net income? The answer is no. Consider the monthly data from 1954 ( months). Compute total returns of negative earnings stocks and subtract risk-free returns (measured by 3-month Treasury rates), this is the equity premium . Then do the same for the benchmark: top large stocks, get .

Simple linear regression with Capital Asset Pricing Model gives us , where are residuals. Statistical tests show that W are close to independent identically distributed, but not quite Gaussian. The . Here, monthly (so annually), thus excess return is negative. But , so market exposure is much greater than 1! More risk, less reward!

A corroboration of value investing. This portfolio is capitalization-weighted: Each stock is weighted according to its market weight. This means we invest in a slice of the total market. Most index funds are capitalization-weighted. Rate data is from Federal Reserve Economic Data (FRED) web site, and stock data is from Kenneth French’s Data Library at Dartmouth College.

A financial econometrician often hopes against hope that returns exhibit the following properties: (A) normal, following the bell curve; (B) IID, meaning independent identically distributed. Unfortunately, this is almost never true.

Here, let me describe a nifty trick: Dividing each data point by the standard deviation normalizes the data. The standard deviation of stock market returns (in financial econometrics this is called volatility) is not constant over time. Periods of economic calm and steady growth when volatility is small alternate with economic crises and financial crashes when volatility is large. It is not clear that dividing by overall volatility makes sense.

Another way to say is that volatility is stochastic: It is a random process by itself. How to extract this stochastic volatility, and how to model it? Here autoregressive conditional heteroscedastic (ARCH/GARCH) models are very useful. They model dependence of current volatility upon the past volatility and returns, with fixed number of lags. These are widely used in Quantitative Finance, often combined with classic linear autoregressive and moving average (ARMA) models. Every time series of returns would have

By chance, we discovered another trick, which obviates the need for GARCH-type models and allows to simply reduce all it to a couple of linear regressions. The miracle is that we can observe volatility independently and separately from the main time series!

Enter VIX, the index created and maintained by the Chicago Board of Options Exchange. Options are contracts which give the holder the right (but not the obligation) to buy or sell a stock or a stock index in the future (at a maturity) at a predetermined price (the strike). The celebrated Black-Scholes formula computes the option price based on current stock price, the strike price, the maturity, and the volatility.

Lost of options are traded in Chicago based on S&P 500. Comparing the market price of each option at a given moment, we solve the Black-Scholes formula backward and find the unknown volatility. This is called the implied volatility. Taking a weighted average of all options, we get the overall implied volatility of the index, which is called VIX. It was computed daily for S&P 500 from the start of 1990, and for S&P 100 (a subset of S&P 500) from 1986.

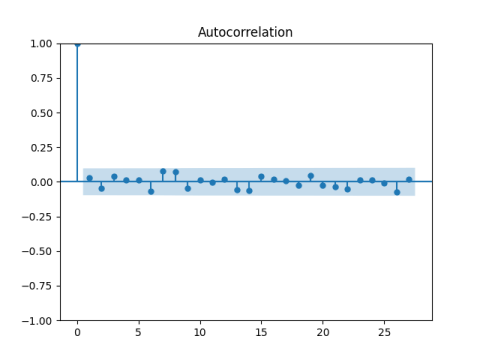

Below is the ACF plot. Take monthly returns of Wilshire Total Stock Market Index, including dividends, from 1990. Below is the plot of their autocorrelation (correlation between month and month , for each ) All correlations are very small and lie within a narrow blue band. This blue band is the fail-to-reject region, where you do not reject the null hypothesis that all returns are IID. It looks like this is, in fact, IID.

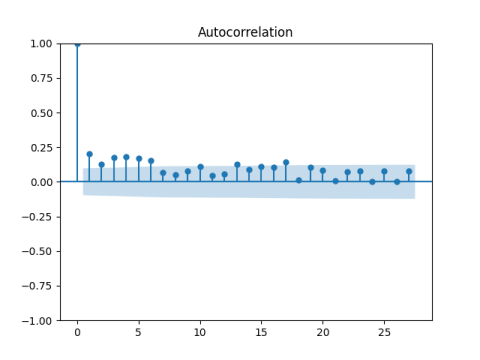

However, if we take autocorrelations for the absolute values, this is not IID anymore!

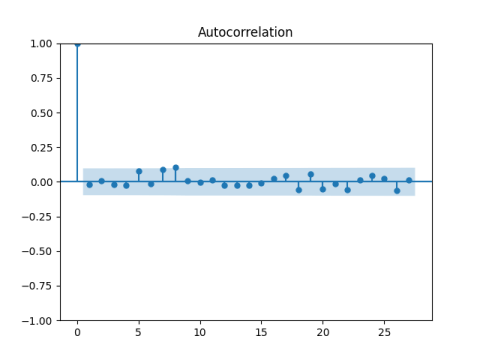

Finally, if we divide total returns by monthly average VIX, we get the autocorrelation functions for returns to be well-behaved, that is, corresponding to IID.

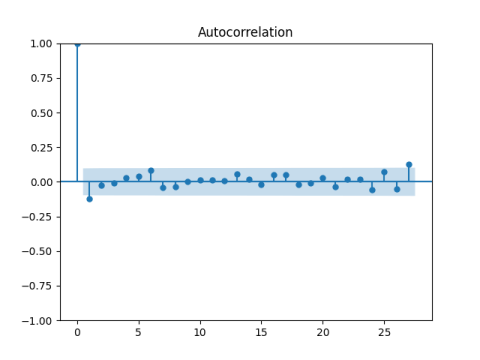

And for their absolute values as well.

We can have without autocorrelation: , but with autocorrelation. In this case, plotting autocorrelation for will give us a false impression that is IID. This would be true if were Gaussian, because for these uncorrelated means independent. Unfortunately, many times data in finance is NOT Gaussian, they have heavy tails!

We discussed in the last post the model , where IID and is auto regression or another mean-reverting process, independent of . Then X have zero autocorrelation, but have positive autocorrelation. Indeed, for crisis times V(t) is large and then is large, and thus and are both large.

When analyzing financial and economic data, one should always be mindful of this possibility. If we checked autocorrelation for both and , and both are zero, then it makes sense to assume X are IID.

We can also apply white noise tests to and to separately.

Consider correlations of ; correlation of ; etc. correlation between . Are they all close to zero? We can test them separately, or combine them (sum of absolute values, sum of squares, or another function = statistics). This gives us Box-Pierce, Ljung-Box, and any other white noise test.

Doing the same for instead of , we can reject or fail to reject white noise for .

I created combined test (omnibus or portmanteau) to test and simultaneously. See the article IID Time Series Testing (2023) in Theory of Stochastic Processes, published by the Ukrainian National Academy of Sciences.

Moreover, it makes them normal, or much closer to normal than originally! This is true by statistical tests of normality (Shapiro-Wilk, Jarque-Bera, or others) and by the quantile-quantile plot (QQ) vs the normal law.

Finally, these properties work for any well-diversified factor market portfolio: Small, Value, Large Growth, and so on. VIX was created from S&P 500 options, but it works for indices, portfolios, and funds other than S&P 500.

Of course, the mean, variance, and other statistics of normalized returns will be different for two different portfolios. But normality and independence stay.

Assume a stock cost 10$ on March 31, 2015, and 12$ on June 30, 2015. In addition, it paid dividend 0.5$ on June 12, 2015. Price return is computed as R = 12/10 – 1 = 20%, and total return (including dividends) as Q = (12+0.5)/10 – 1 = 25%. These are arithmetic returns.

These are good for computing portfolio returns: For three stocks A, B, C, with total returns 10%, -5%, and 20%, consider the portfolio investing in them in proportions 40%, 30%, 30%. Then the total return of this portfolio is 0.4*10% + 0.3*(-5%) + 0.3*20% = 8.5%. Same is true if we are speaking of price return.

❌ However, compound interest presents a problem: If in January total return is 10% and in February it is 20%, then the overall total return is not 10% + 20% = 30%. Instead, it is 32%. Why? Because we get February return not simply on the original wealth but on the wealth gained in January. Indeed, if we start with wealth 100 on the New Year’s day then on January 31 we get 110 and on February 28, we get: 110*(1 + 20%) = 132, thus 100 turns into 132 which gives us 32%. Same problem if we got price returns instead of total returns.

Thus analysts sometimes use geometric (logarithmic) returns: Revisit the example at the beginning of this post. The price return is ln(12/10) = ln(1.2) = 18.2%, and the total return is ln(12.5/10) = ln(1.25) = 22.3%.

It is easy to convert arithmetic return into geometric return: If R is the arithmetic return, then G = ln(1+R) is the geometric return. Conversely, R = exp(G) – 1. But do not forget that percentages must always be converted to fractions, for example 0.05 instead of 5%.

This solves the compound interest problem: The total geometric return in January is ln(1 + 10%) = ln(1.1) = 9.5% and in February . Thus the overall total geometric return is 9.5% + 18.2% = 27.7% = ln(1+32%) = ln(1.32).

On the other hand, for geometric returns one cannot compute the portfolio return out of stock returns like we did for arithmetic returns. You need to convert it back to arithmetic returns.

Conclusion: Use geometric returns for analysis of financial time series, and arithmetic returns for portfolio analysis.

This is my short notices about financial econometrics and stochastic financial modeling. We discuss stocks, bonds, portfolios, rates, volatility, and more. WordPress was chosen because it supports . I am a professor of Mathematics & Statistics at the University of Nevada, Reno.

this year from risky stocks if you could get

this year from risky stocks if you could get  from risk-free Treasury bonds?

from risk-free Treasury bonds? be the equity premium for zero-dividend stocks and let

be the equity premium for zero-dividend stocks and let  be the equity premium for dividend-paying stocks. Then

be the equity premium for dividend-paying stocks. Then  , where

, where  are residuals. This implies that excess return

are residuals. This implies that excess return  for month and so

for month and so  for a year. And market exposure

for a year. And market exposure  (for a month or a year). The

(for a month or a year). The  . This makes the following financial sense:

. This makes the following financial sense: , but you lose

, but you lose  and for zero-dividend stocks is

and for zero-dividend stocks is  . The annualized standard deviation for dividend stocks is

. The annualized standard deviation for dividend stocks is  and for zero-dividend stocks is

and for zero-dividend stocks is  . More risk, less reward!

. More risk, less reward! months). Compute total returns of negative earnings stocks and subtract risk-free returns (measured by 3-month Treasury rates), this is the equity premium

months). Compute total returns of negative earnings stocks and subtract risk-free returns (measured by 3-month Treasury rates), this is the equity premium  stocks, get

stocks, get  .

. , where

, where  are residuals. Statistical tests show that W are close to independent identically distributed, but not quite Gaussian. The

are residuals. Statistical tests show that W are close to independent identically distributed, but not quite Gaussian. The  . Here,

. Here,  monthly (so

monthly (so  annually), thus excess return is negative. But

annually), thus excess return is negative. But  , so market exposure is much greater than 1! More risk, less reward!

, so market exposure is much greater than 1! More risk, less reward!  and month

and month  , for each

, for each  ) All correlations are very small and lie within a narrow blue band. This blue band is the fail-to-reject region, where you do not reject the null hypothesis that all returns are IID. It looks like this is, in fact, IID.

) All correlations are very small and lie within a narrow blue band. This blue band is the fail-to-reject region, where you do not reject the null hypothesis that all returns are IID. It looks like this is, in fact, IID.

without autocorrelation:

without autocorrelation:  , but

, but  with autocorrelation. In this case, plotting autocorrelation for

with autocorrelation. In this case, plotting autocorrelation for  will give us a false impression that

will give us a false impression that  , where

, where  IID and

IID and  is auto regression or another mean-reverting process, independent of

is auto regression or another mean-reverting process, independent of  . Then X have zero autocorrelation, but

. Then X have zero autocorrelation, but  have positive autocorrelation. Indeed, for crisis times V(t) is large and then

have positive autocorrelation. Indeed, for crisis times V(t) is large and then  is large, and thus

is large, and thus  are both large.

are both large. ; correlation of

; correlation of  ; etc. correlation between

; etc. correlation between  . Are they all close to zero? We can test them separately, or combine them (sum of absolute values, sum of squares, or another function = statistics). This gives us Box-Pierce, Ljung-Box, and any other white noise test.

. Are they all close to zero? We can test them separately, or combine them (sum of absolute values, sum of squares, or another function = statistics). This gives us Box-Pierce, Ljung-Box, and any other white noise test. . Thus the overall total geometric return is 9.5% + 18.2% = 27.7% = ln(1+32%) = ln(1.32).

. Thus the overall total geometric return is 9.5% + 18.2% = 27.7% = ln(1+32%) = ln(1.32). . I am a professor of Mathematics & Statistics at the University of Nevada, Reno.

. I am a professor of Mathematics & Statistics at the University of Nevada, Reno.