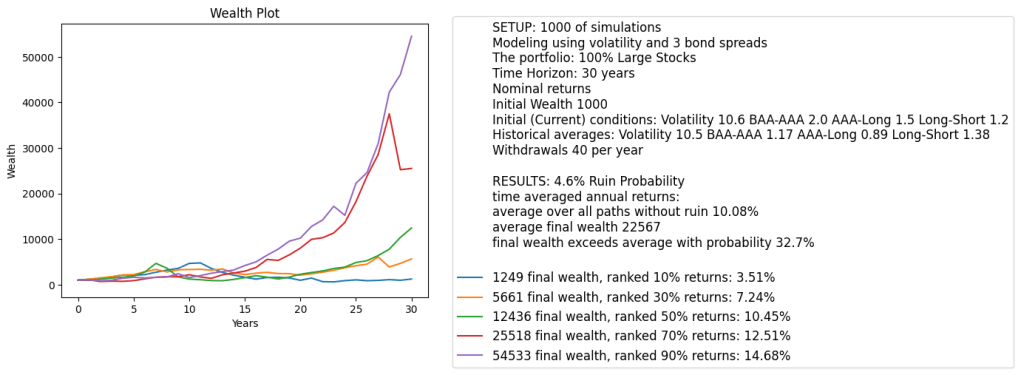

I write this to combine all simulators in the same post. We consider various models for annual total returns (nominal/real) studied in previous blog posts. I carefully checked goodness-of-fit for each regression in each model, so one can trust that innovations are independent identically distributed. Unfortunately, we cannot always guarantee innovations are Gaussian. But for returns, and often for other regressions, they in fact are Gaussian. For other regressions, they are close.

In each version, we run Monte Carlo simulations 1000 times. We allow for choice of time horizon (how many years), annual withdrawals or contributions, initial wealth, and choice of innovations: multivariate Gaussian simulation (which is not exactly true, see above) or kernel density estimation. We compute the following quantities:

Ruin probability

Average final wealth

The probability of the final wealth exceeding its average

Average total returns over the paths which do not result in ruin

We also plot five paths which end in wealth ranked bottom 10%, bottom 30%, median (50% quantile), top 30%, and top 10%. This way we give a range of all plausible outcomes. I think that plotting 5% or 1% quantiles will give an unrealistic picture.

For some but not all, I allowed initial conditions to be changed. I think it’s the best to allow index level, bond spreads, and volatility but not earnings to change. Earnings are trailing, they are a bit hard to find online, and they are updated infrequently. But the other information is updated daily.

Future work will include:

Allowing these initial conditions (index, spreads, volatility) to be changed by the user.

Updating all Python files so that all use the same notation and the same data file century.xlsx.

Upload this data file to my web page.

Test the model with this new valuation measure and the three spreads, and create a simulator for this.

Also include both trailing earnings yield and the new valuation measure in the same regression for returns.

We need to add the following features in this simulator: Choose actions by the investor to make sure that the following events happen with given probability

I need a given amount in a given number of years. How much do I invest now, if I contribute only at the initial time?

I need a given amount in a given number of years. How much do I contribute per year, if I do not invest at the initial time?

Starting from now, I need to withdraw per year during years. Here and below, we can have so we can use this money infinitely long. How much to invest now?

In years I need to withdraw per year during years. How much to invest now, if I invest only at the initial time?

In years I need to withdraw per year during years. How much to contribute in each of these years?

I have now and plan to spend it for years. How much to withdraw per year?

I have amount now and plan to contribute/withdraw per year during years. How much will I have at the end?

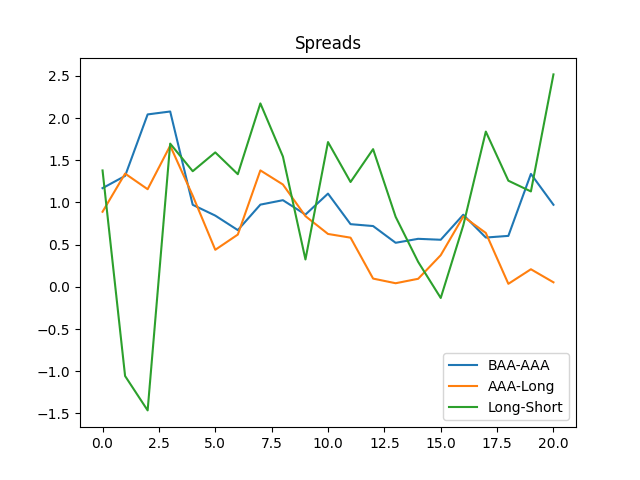

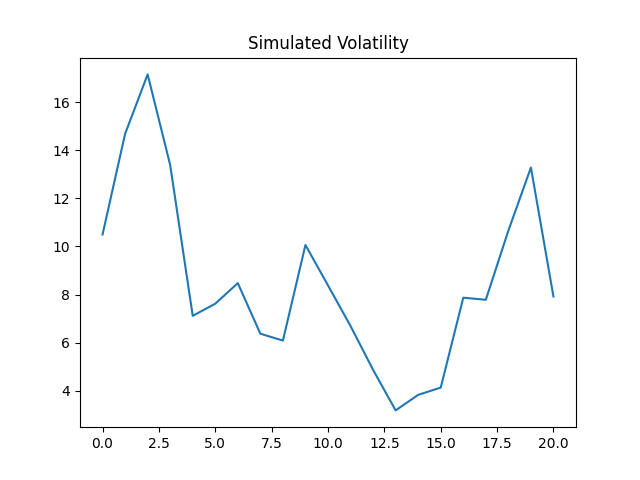

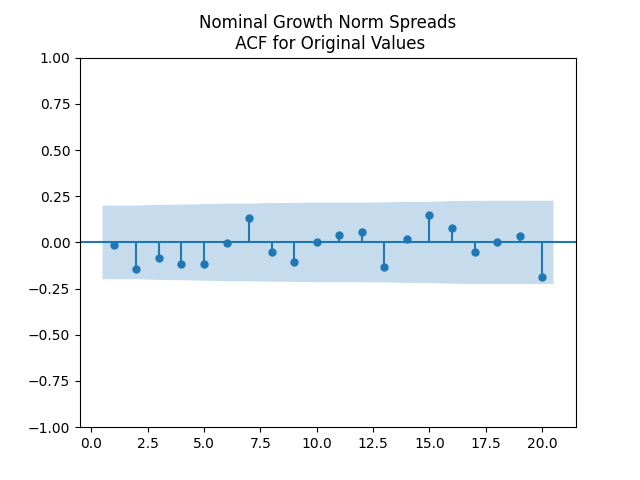

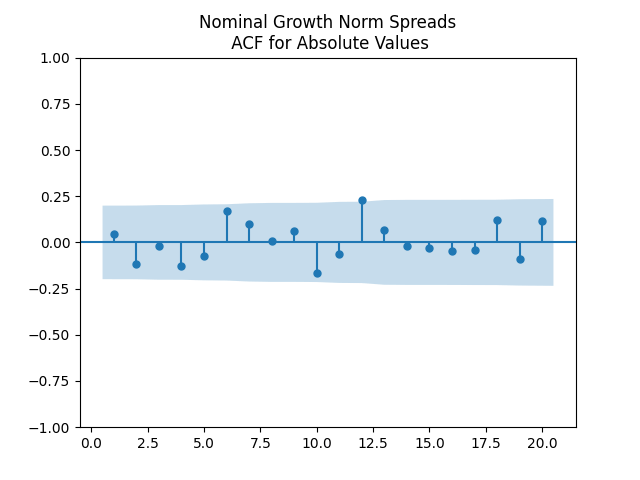

Standard analysis of residuals explained in this main post shows they are well modeled as independent identically distributed Gaussian. All are not significant: Student T-test has p-values greater than 5%. The most significant (having the smallest p-values) is corresponding to the BAA-AAA spread. Exceptions: for Total Nominal Returns, has The coefficient is very statistically significant with See below the graphs for simulated volatility and spreads.

We added to this GitHub repository the entire simulator for the rates-only model (with annual volatility, of course). It is done in Python file rates-only-sim.py in the same repository. See below the graph.

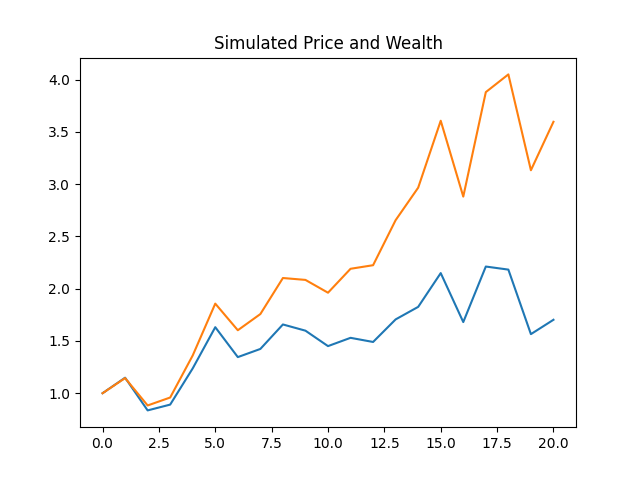

Below we show one simulated path of prices and wealth. This simulation is for the case of real (inflation-adjusted) version and 20-year horizon.

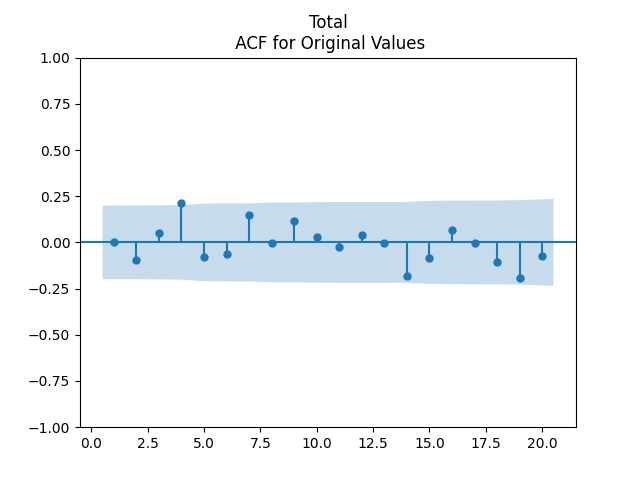

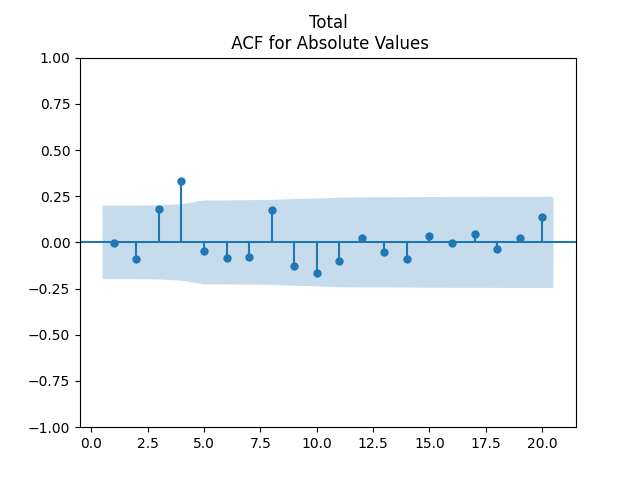

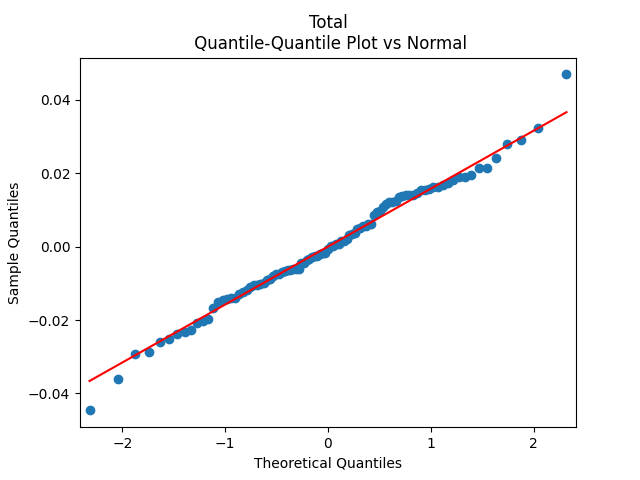

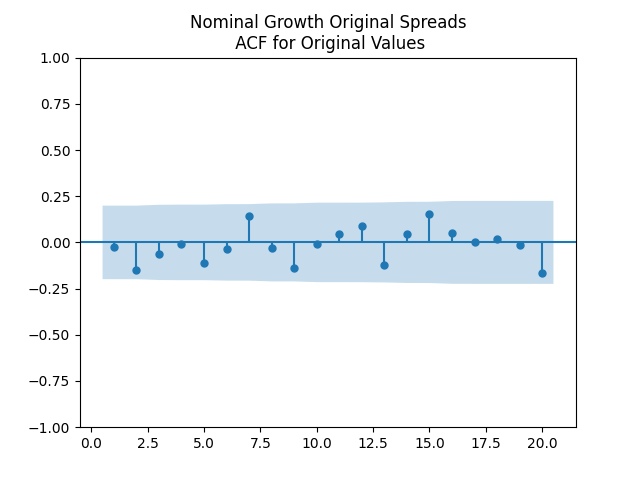

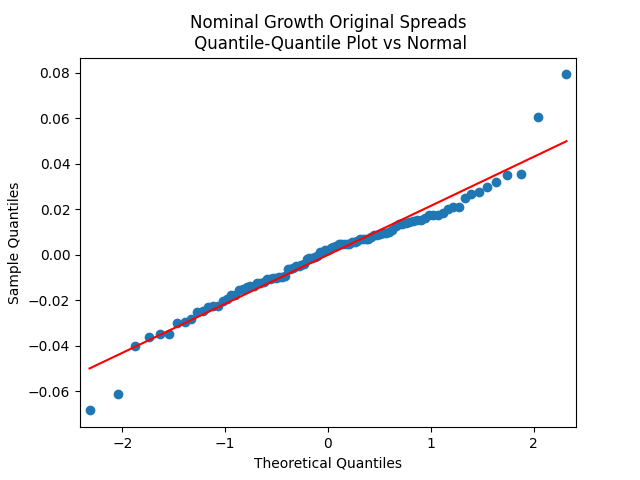

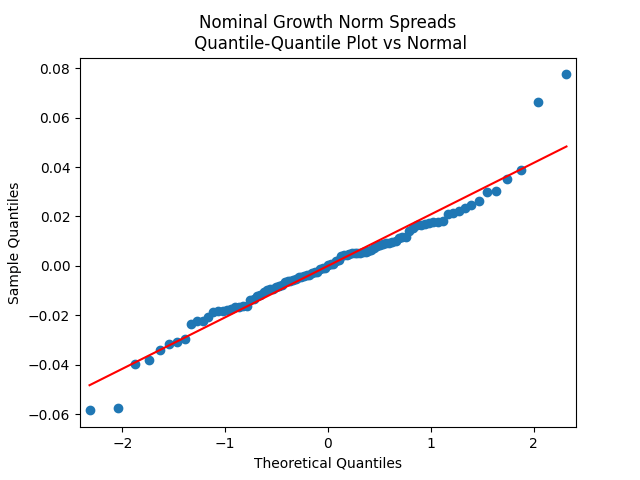

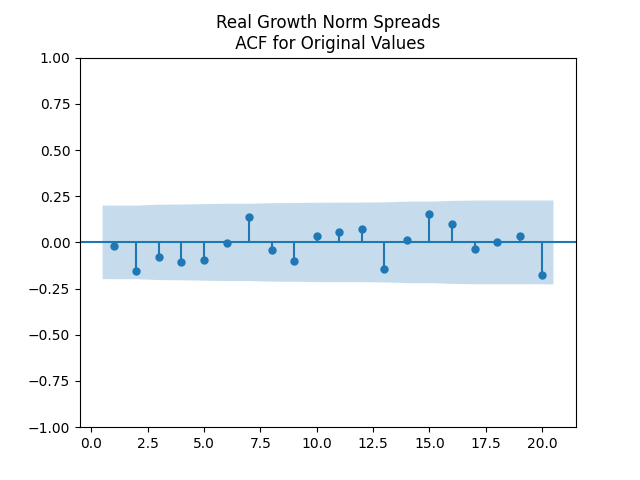

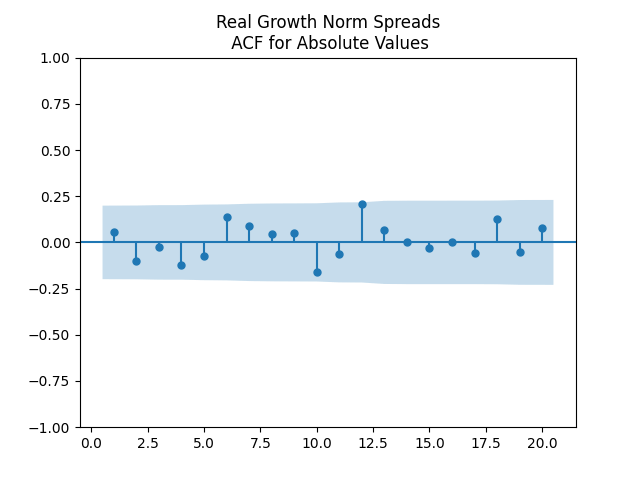

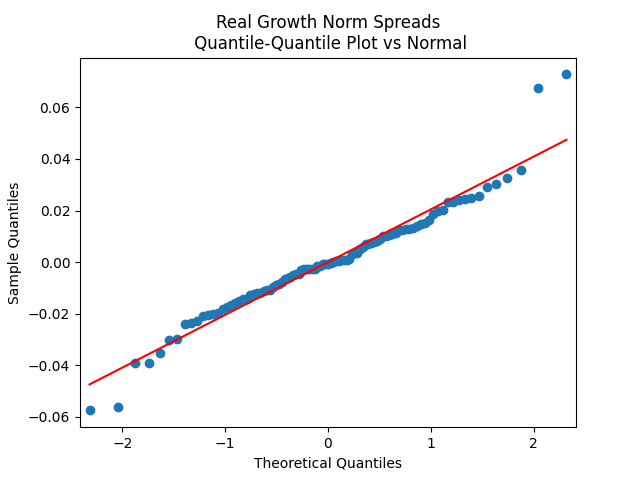

Finally, pick for the case of total nominal returns. Below we see the autocorrelation plot for , for , and the quantile-quantile plot for versus the Gaussian distribution.

As before, we have this strange value at lag 4 for autocorrelation. This presents no problem, since other values are low.

We continue part III of the blog post. There, we modeled price and total returns of S&P 500 (both nominal and real) as a linear regression with four factors: three bond spreads BAA-AAA, AAA-Long, and Long-Short; and earnings yield (last year’s earnings divided by the end-of-year index level). Look at that blog post for background and definitions.

As usual, we had regression residuals multiplied by annual volatility. Also, as usual, we added this volatility as the fifth factor. So that after dividing the regression equation by this volatility and applying ordinary least squares fit, we still have an intercept in this new regression equation.

Here, we change this classic earnings yield to its cyclically adjusted version. We allow any averaging window between 1 and 10 years.

We make another change compared to the blog post: Instead of the earnings yield as a factor in linear regression for total/price and nominal/real returns, we take the logarithm of this earnings yield. This is motivated by a remark at the end of this post.

We also add results of parts I and II in the blog post and unite them in the same Python code file. This is different from the blog post, where we split the Python code in 3 files corresponding to each part I, II, III. The code and data are on GitHub/asarantsev repository 3spreads-CAPE-simulator

Consider the linear regression

Here, are spreads: BAA-AAA, AAA-Long, Long-Short, and cyclically adjusted earnings yield (average earnings over the last few years divided by end-of-year stock index. As usual, is annual realized inflation, and are independent identically distributed. We fit this for windows of 5 and 10 years, and for which are total/price returns, real/nominal versions.

Methods: We apply standard analysis of residuals , outlined in this previous post. We also consider of this regression and compare this with cut version without any spreads. Finally, we consider the Student T-test for each coefficient.

Results: All residuals can be reasonably modeled as IID Gaussian. All coefficients in the large regression are NOT significant. The most significant (having smallest p-value) among spreads is usually BAA-AAA. Adjusted does not change much for price returns and barely for total returns.

Simulation: We allowed to change the index level, three spreads, and volatility for the initial conditions. But we did not allow to change trailing annual earnings. We have an entire averaging window, we do need this, as shown in the previous research. Input of 5 or 10 annual earnings would be cumbersome for a user. However, input of current price is easy.

Also, it’s easy to look for current S&P 500 level, rates (which lead to spreads) and volatility (measured by VIX) in the market. But it’s harder to look up last few years of earnings. Anyway, these earnings change slowly and are updated rarely.

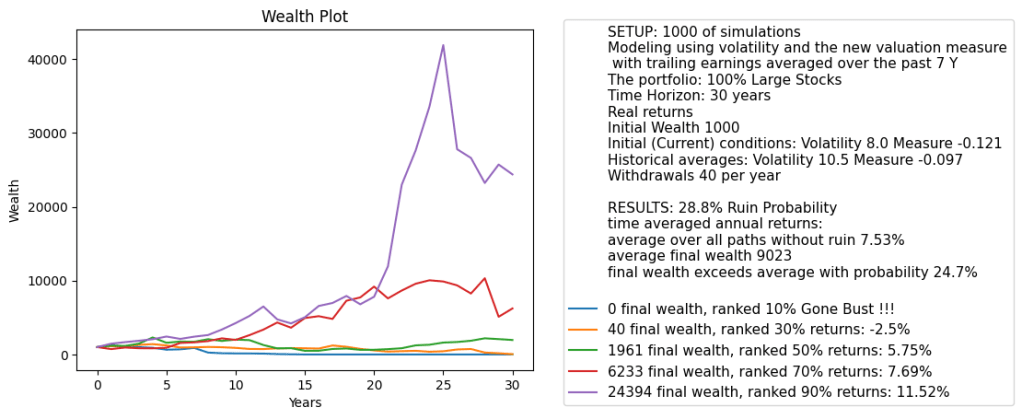

Continuing the research in the blog post and using the Python code from my GitHub repository, I made a simulator of the Standard & Poor 500 annual total returns using the new valuation measure and annual volatility with inputs: Nominal or Real, and averaging window ranging from 1 to 10 years. We can input time horizon, withdrawals/contributions, choice for innovations simulator: kernel density vs multivariate Gaussian law, and initial wealth, for the simulation. This is similar to the combined simulator for volatility and cyclically adjusted earnings yield: see this post and this post. We do not allow the user to choose initial conditions for the simulator, instead making them to be the current (as of December 2024) market conditions.

We consider the regression for where is total returns and is earnings growth terms. Let be the new valuation measure. Then we model as an autoregression of order 1: Earlier we found that it is better to model where is the annual volatility, and are independent identically distributed Gaussian with mean zero. But to use the ordinary least squares regression, we need to divide this equation by the volatility and then fit it. However, this new normalized regression does not contained the intercept

After going back to the original formulation, this intercept term would become the factor of volatility:

Comparing the two regressions, we see that can be rejected: the Student T-test gives very low p-values. This shows us that we might want to use the extended regression. But we keep the original regression with volatility but without the intercept, to make it simple. Extending it will require more research.

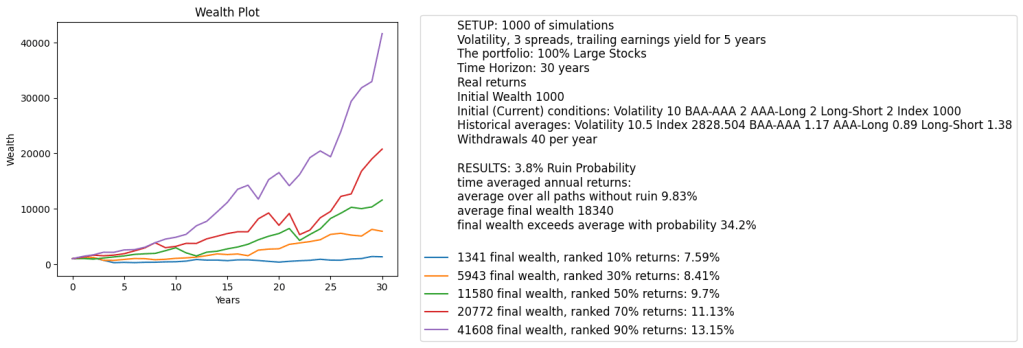

Below we see the results plot for this simulator. We pick 7-year averaging window and 30-year time horizon. The current measure is lower than historical average. This is the opposite of CAPE which shows that currently (as of December 2024) the S&P 500 is overvalued. We see that the variance of the terminal wealth is not very large, compared with the CAPE-volatility model with log(earnings yield) as factor instead of earnings yield in this post.

We need to do the following actions:

Allow for a version of this simulator with 1-year earnings (no averaging) to choose the initial valuation measure and annual volatility. For 2-year and wider averaging windows we do not allow this, because picking earnings for each of 2 or more last years is too complicated for the user.

Present a table for all averaging windows, how good is regression fit? and values for Student T-test. Are innovations Gaussian or independent identically distributed? If the regression fit is not good, according to these metrics, we can prohibit the user to apply these choices for averaging windows.

Include the volatility in the main regression, that is, the coefficient Presumably we need to adapt the autoregression simulation for that. Also, analyze the innovations and see whether this is a good fit. If not, again prohibit the user to apply these options.

This would complete the research for earnings. But we also need the bond spread analysis. This is left for further research: To build a simulator and to include trailing averaged earnings for more than one year. But then you should not allow the user to change these earnings. Maybe it’s OK to choose volatility or bond rates (which lead to bond spreads).

I do not think combining these simulators in one Python code file works well. Indeed, when you add more and more features and options, it becomes harder to manage them. Better to create multiple Python files for each option. In the main Python file we can import all other files and organize input of options. If a user chooses an option, the main Python file should redirect to another Python file which does computation for this chosen option.

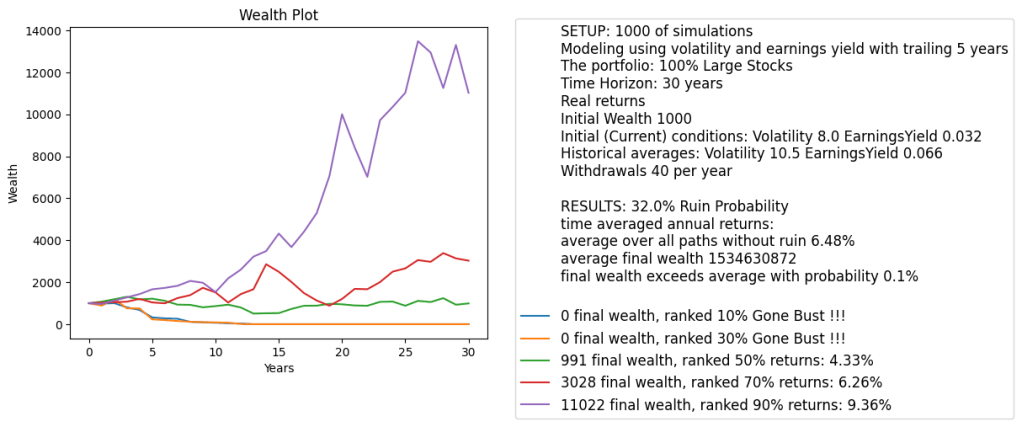

Setting: Withdrawals 40 per year: 4% of the initial capital (inflation-adjusted). Time horizon is long: 30 years. As before for cyclically adjusted price-earning ratio: CAPE, we do not allow the choice of initial conditions: We pick them to coincide with current (as of December 2024) market conditions.

Results: Cyclically adjusted earnings yield currently is much lower than historical average. This is equivalent to CAPE being much higher than historical average. This implies lower future returns than historically, and higher ruin probability.

We can also see high variance of final wealth: Greatly skewed to the right. A few top simulations have huge wealth. This might be due to including earnings yield, instead of its logarithm. Then the time series model (in continuous time this would be a stochastic differential equation) for total returns has an exponentially increasing drift.

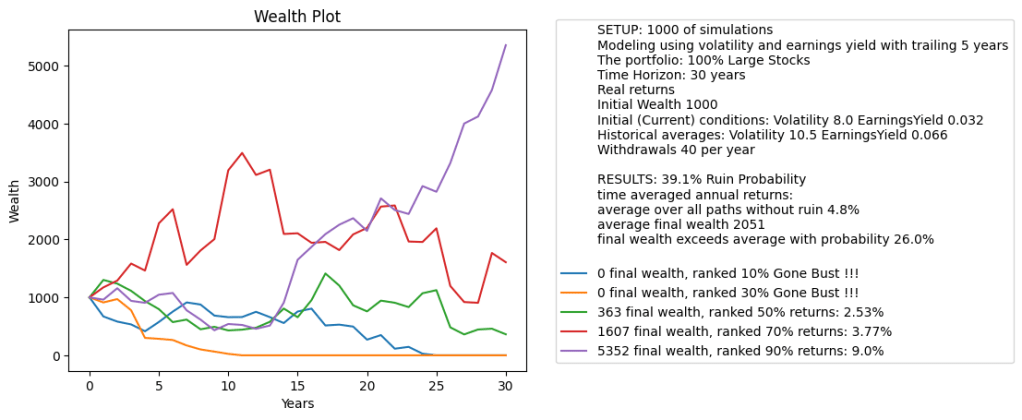

Modification: Let us change the earnings yield factor to its logarithm in regressions for price and total returns. Then the variance of final wealth is much less, and less skewed to the right. That is, unrealistic very high wealth outliers are much less likely. See below the graph. But returns are still much lower than for historically average earnings yield. We still refer to the same GitHub/asarantsev repository earnings-yield-annual-simulator.

This research continues blog posts on modeling returns vs earnings yield and volatility and returns vs only volatility. But previous Python code combines fitting of this model and simulation. Here, we removed plots (quantile-quantile and autocorrelation function for residuals) and analysis of skewness, kurtosis, etc. We only keep fitting regression code necessary for actual simulations. Also, we combine these two options (with or without earnings yield) so a person can make a choice. We also present a choice between simulating innovations using Gaussian multivariate distribution or kernel density estimation.

We also change the models slightly: Previously, we normalized returns and earnings growth by dividing them by annual volatility Here, we instead model these as regression

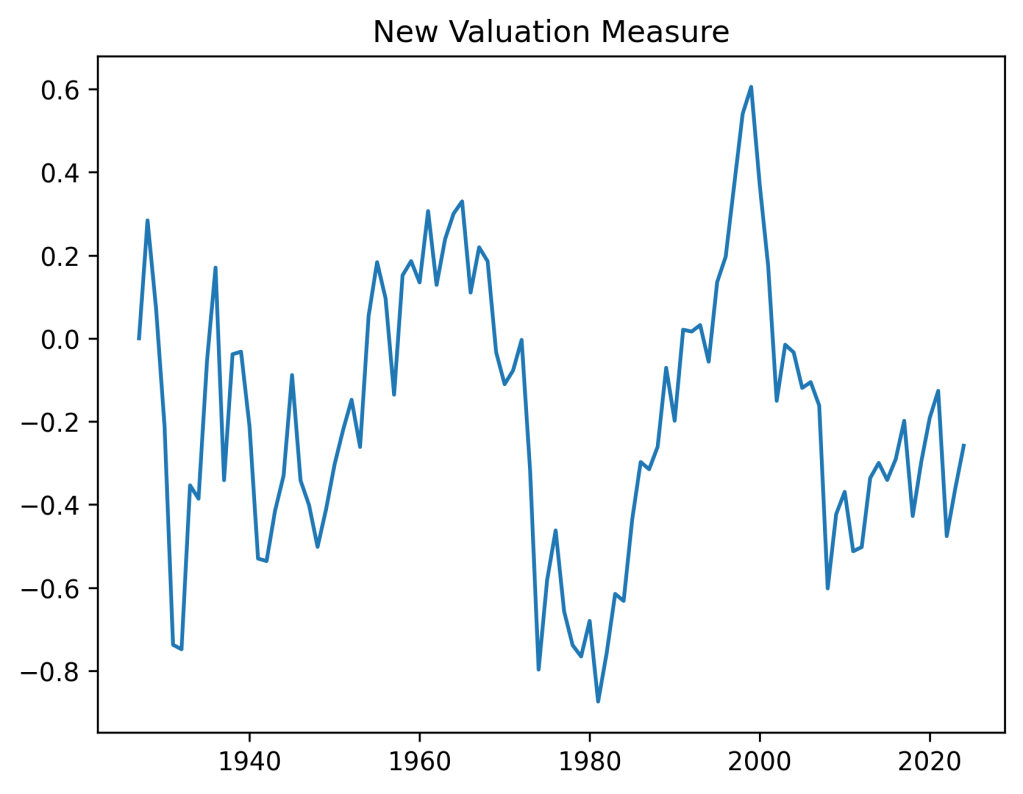

Let be the 10-year trailing averaged annual real earnings. Let be the log growth terms. We compute these for Also, let be total real returns for the same years. Then is implied dividend yield; we assume is its long-term average. We model the valuation measure as an autoregression of order 1:

where innovations are independent identically distributed, with mean zero.

As discussed before, the difference between our research and arXiv:1905.04603 is that we take December CPI data instead of January to compute inflation, and end-of-year S&P index data instead of average January close level. Also, we consider 10-year instead of 5-year trailing window for real earnings.

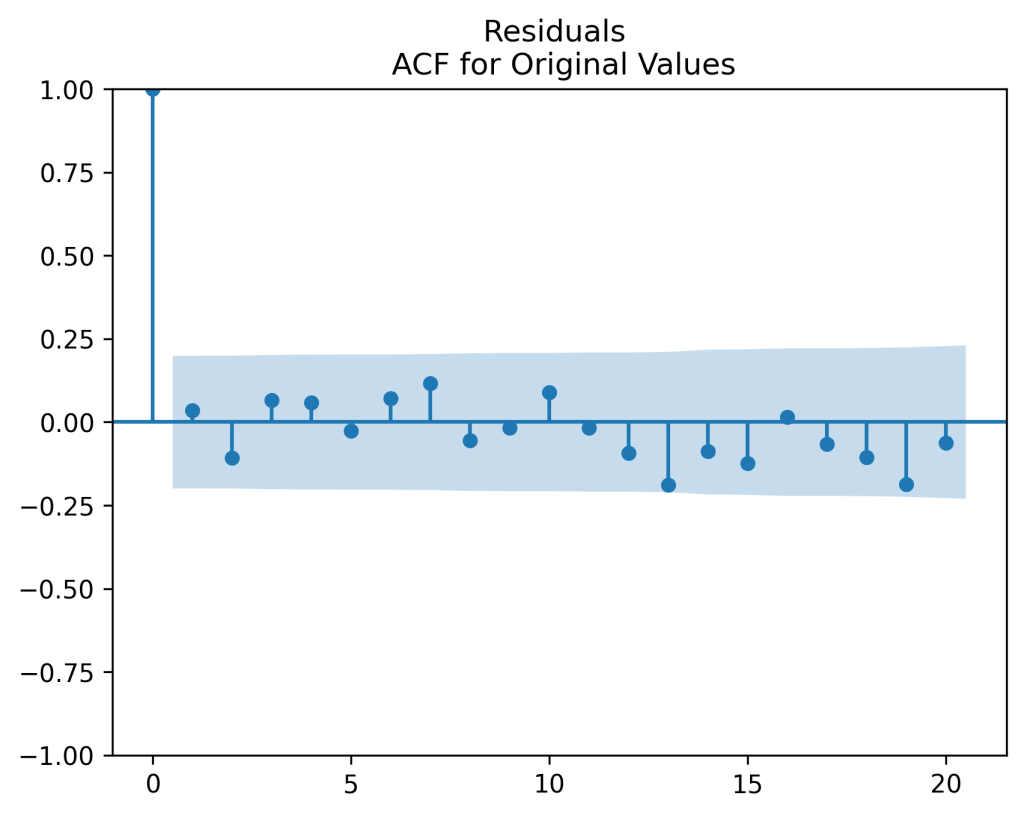

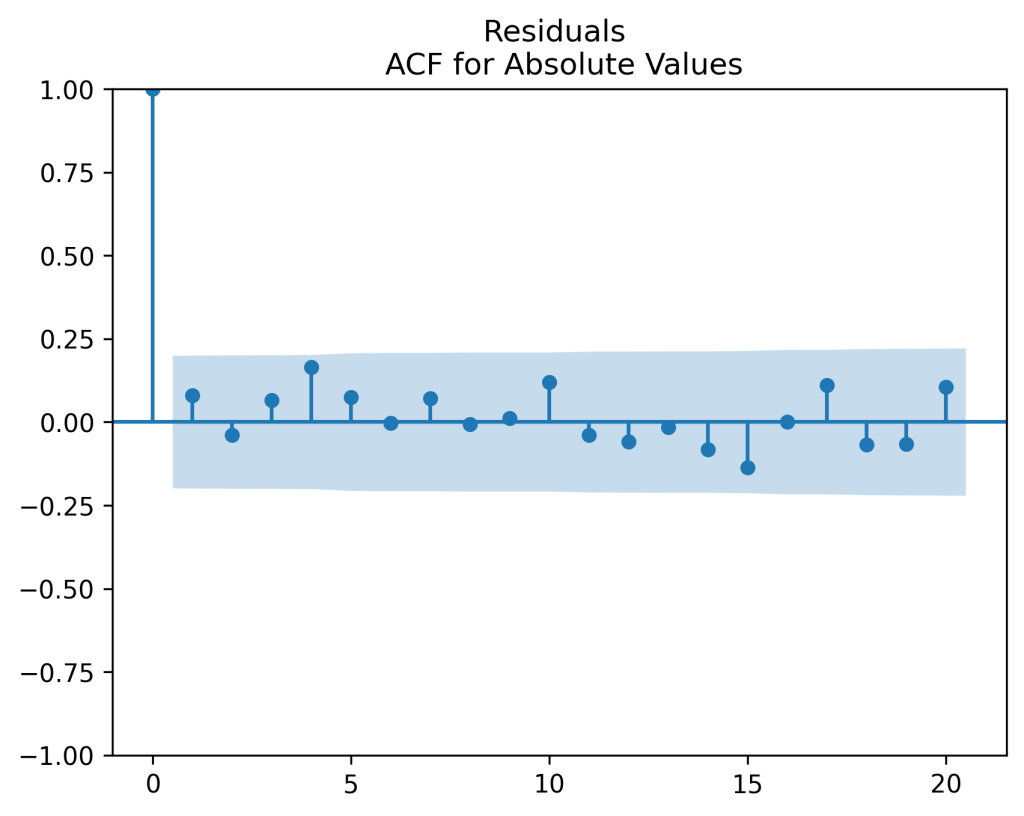

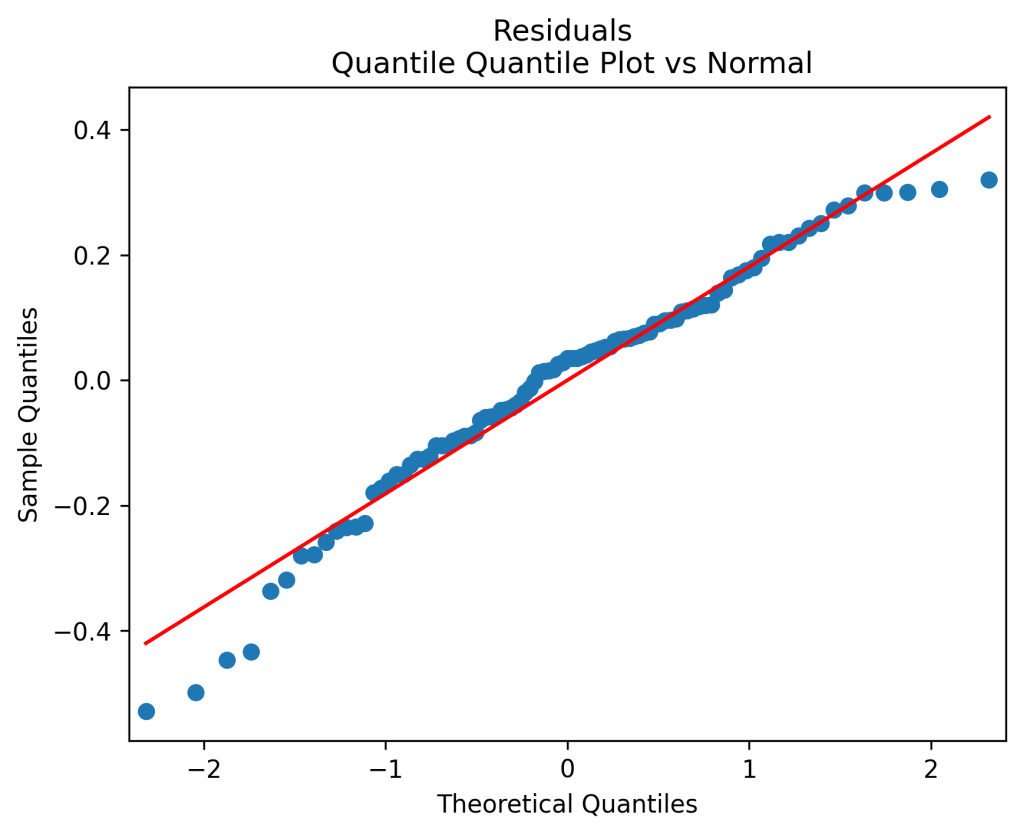

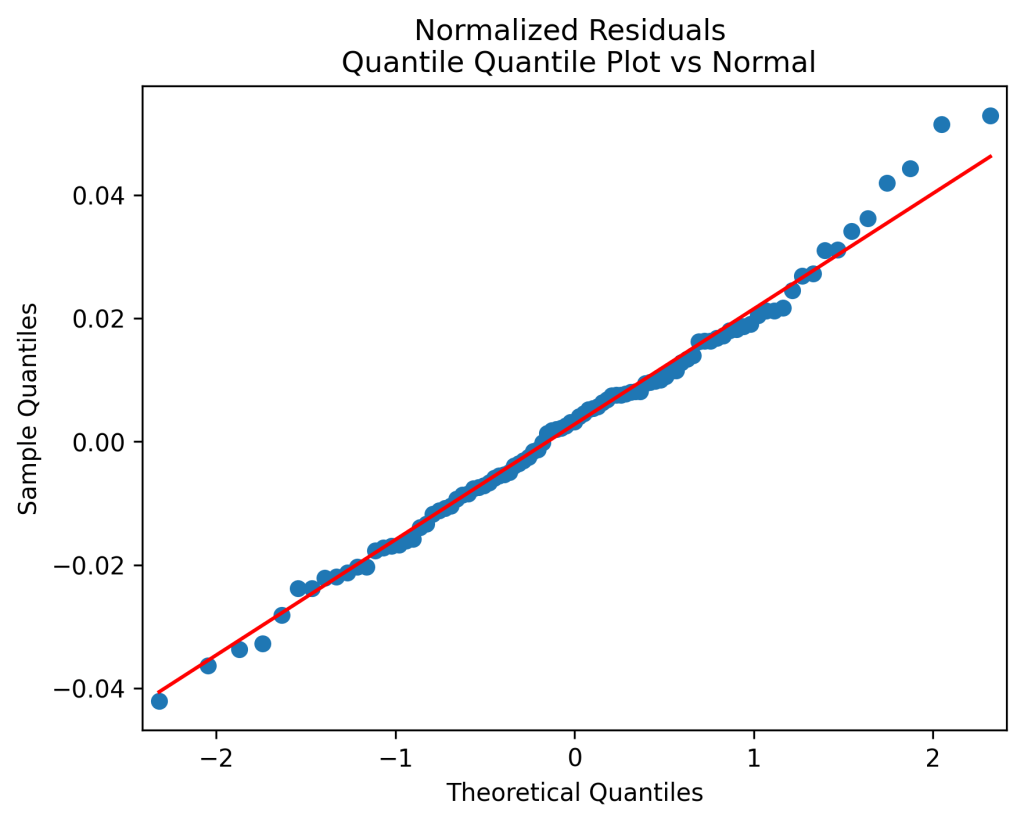

Original model fit: We get innovations which are IID but not quite Gaussian. See plots below. Also, the Shapiro-Wilk and Jarque-Bera tests give us The Student test for gives us so the model is not a random walk, but rather mean-reverting.

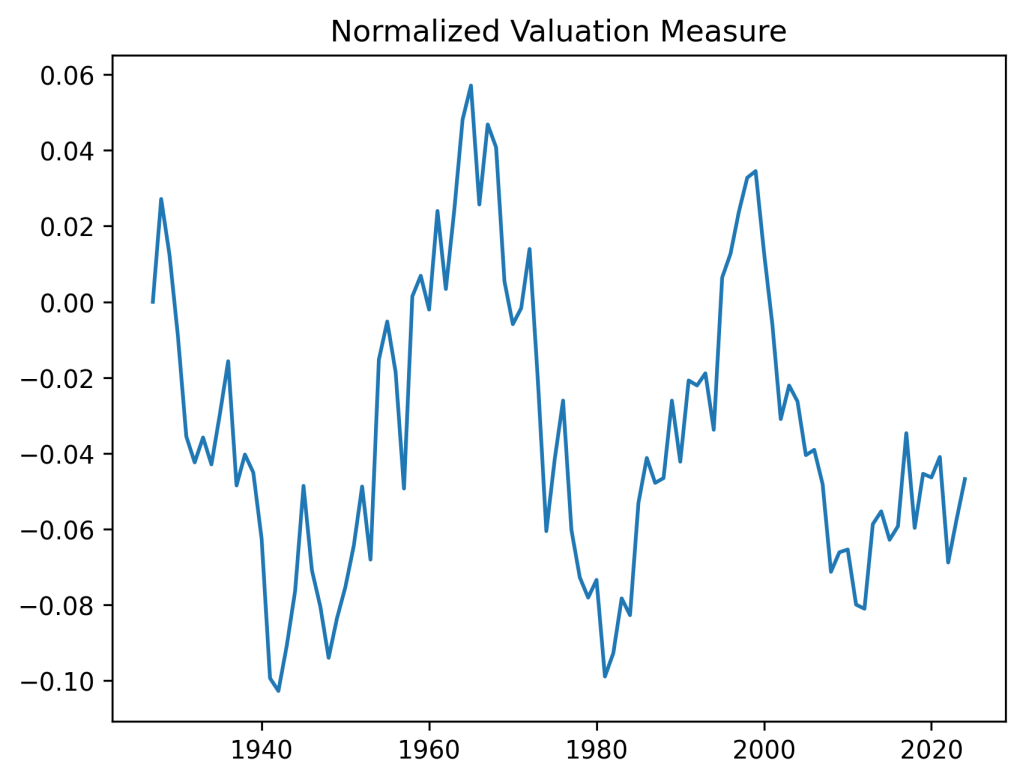

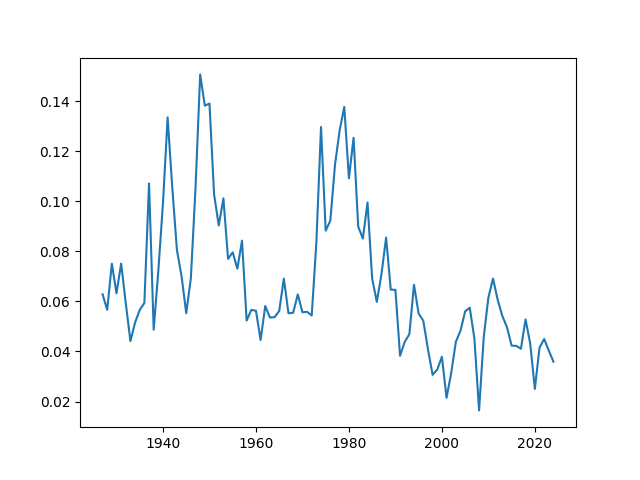

Bubbles and busts: The valuation measure has plot shown below. It is clear that the current valuation measure is well below the historical average. This is in contrast with the classic price-earnings ratio and Shiller CAPE. Both show that the S&P is currently overvalued. However, on the graph below we can see the overvaluation right before the Great Depression, in the 1960s, and at the start of the 21st century (the dotcom bubble). This graph is quite similar to the one in arXiv:1950.04603.

Normalize innovations: Next, let us divide innovations by annual volatility computed by Angel Piotrowski. The result is better: These are independent identically distributed Gaussian. Strange high autocorrelation at lag four does not change the suggestions that the innovations indeed can be modeled as IID. Shapiro-Wilk and Jarque-Bera normality tests are

In other words, it is reasonable to model where

Normalize regression, not residuals: Alternatively, we can divide implied dividend yield by volatility and perform this autoregression for the new terms: Consider and repeat the analysis. See the plot of the valuation measure below. It looks very similar to the one above.

Again, the Student T-test gives us for Next, the Shapiro-Wilk and Jarque-Bera tests for new innovations give us The autocorrelation function plots for and for show it is reasonable to model these as independent identically distributed, and look very similarly to the above plots for instead of Further, the quantile-quantile plot for looks very similarly to the one for

The for original regression and for new regression. We leave it to the reader which one to use. But we intend to use the original regression for future financial simulator.

Update: We used the new regression in the financial simulator. We use the version without the volatility factor, which after division becomes the intercept of the ordinary least squares new regression. This makes the innovations multiplied by this volatility, but does not introduce any new factors in this model. We only compare total returns and earnings growth.

PART 1. Modeling bond spreads BAA-AAA, AAA-Long, Long-Short as vector autoregression

PART 2. Modeling earnings growth using these bond spreads as regression factors

PART 3. Modeling S&P returns using 1-year earnings yield and these bond spreads as regression factors

PART 1:Modeling bond spreads BAA-AAA, AAA-Long, Long-Short using vector autoregression of order 1, with innovations normalized by annual volatility. This model fits well and is stable in the long run, with IID but not quite Gaussian innovations.

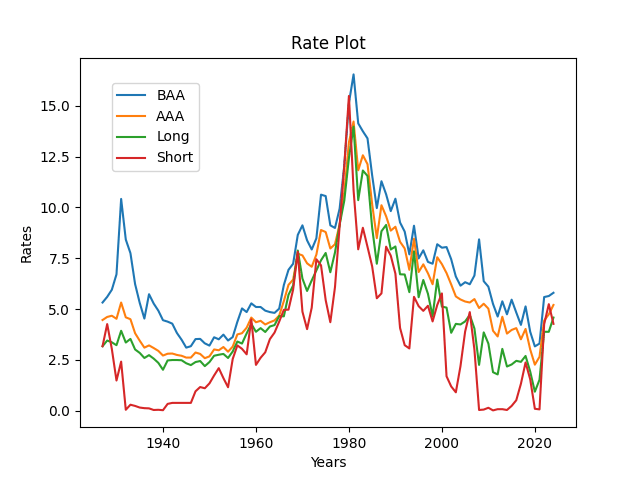

Data: We consider four bond rates, average daily December data 1927-2024, at end of year t:

Long stands for 10-year Treasury rate (1963-now), long-term government securities (1927-1962)

Short stands for 3-month Treasury rate (1934-properly extended to earlier data), and short-term (3- and 6-months) government securities (1927-1933)

BAA is Moody’s rates for portfolios of investment-grade corporate bonds with BAA ratings (1927-2024)

AAA is Moody’s rates for portfolios of investment-grade corporate bonds with AAA ratings (1927-2024)

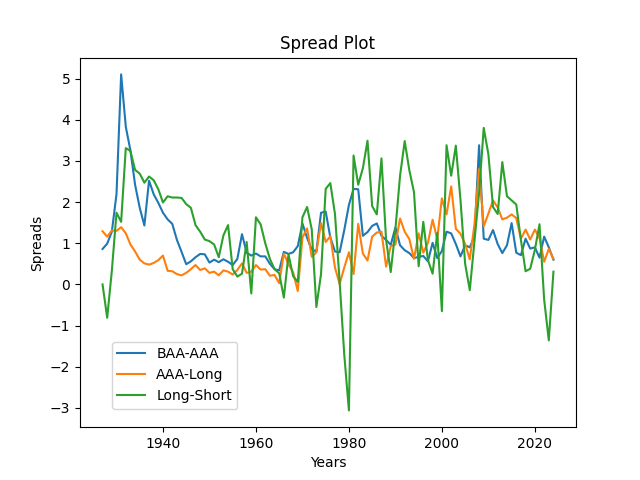

Next, we take three bond spreads: BAA-AAA, AAA-Long, Long-Short. See the time graph below.

Model: Consider the vector S(t) of three bond spreads. We model it as where and is a 3\times 3 matrix, and is a sequence of independent identically distributed (IID) trivariate random vectors with mean zero. This is an extension of the same model for two spreads: BAA-AAA and AAA-Long, which, in turn, continues this research.

As usual, we also have log Heston model for the volatility: where are IID with mean zero. We already fit it in the previous post, so we do not discuss it here.

We fit this multivariate model for by each of three scalar equations. We divide this equation by the volatility and then use ordinary least squares method. Then we test each of the three components of the innovation series for IID Gaussian using the usual procedure:

Empirical skewness and kurtosis (both = 0 for Gaussian)

Shapiro-Wilk and Jarque-Bera normality tests p-values

L1 norm for the autocorrelation function for lags 1, \ldots, 5, of and

Autocorrelation function plots for and for

The quantile-quantile plot of versus the normal distribution

Results for coefficients: We have the following point estimates:

The Student T-test gives us only for diagonal values of B, its third row, and c. It is important to verify that eigenvalues of B are strictly less than 1. Then the time series model above is stable and ergodic in the long-run, see my manuscript arXiv:2411.03699: Zero-Coupon Treasury Rates and Returns using the Volatility Index with Jihyun Park. It has a unique stationary distribution, see this work. But this is left for further research.

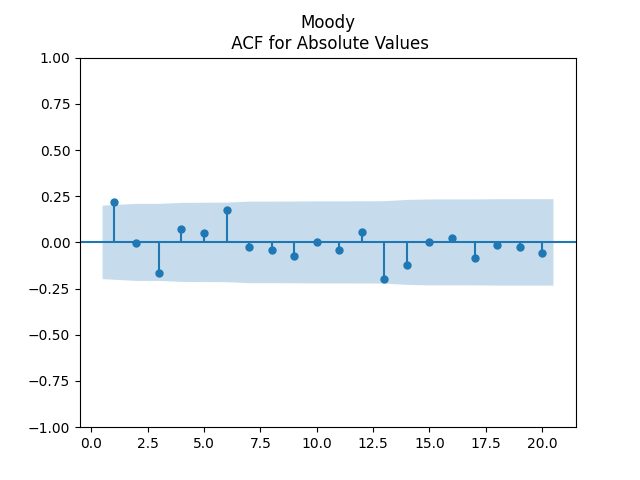

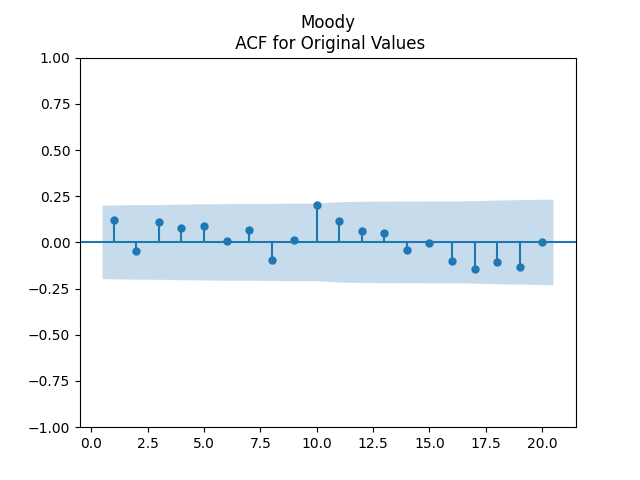

Results for innovations: They can be modeled as IID. The plots are shown below for each of the three series of residuals. First, Moody means BAA-AAA spread. Although we have strange ACF for lag 1 for absolute values, overall the plots are consistent with IID.

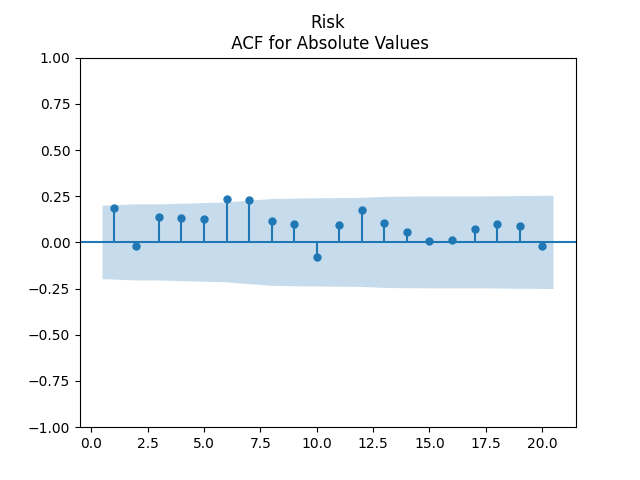

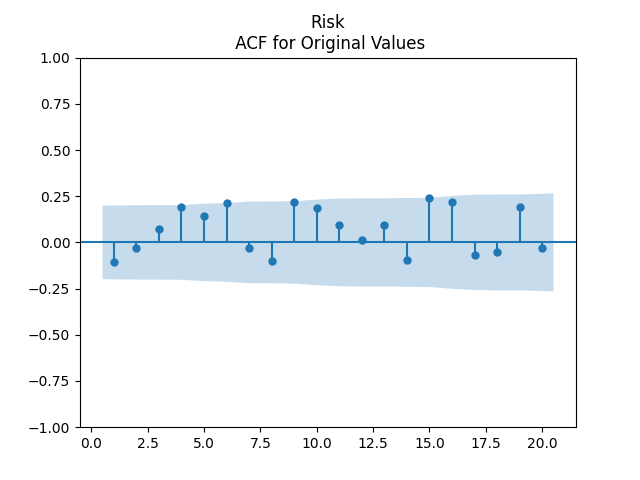

Second, Risk means AAA-Long spread. Here, we have a very good fit for IID.

Finally, Term means Long-Short spread. We also have this strange autocorrelation at lag 1 for absolute values.

Unfortunately, we did not test the cross-correlation functions and plots, similarly to this post. We failed to do this because of lack of time, and because Python lacks a built-in function for such plots, unless you use a simple vector autoregression without volatility. But previous modeling of closely related modeling suggests that these cross-correlation functions will not be significantly different from zero.

The values of L1 norm for the first five lags of ACF from each of the 3 spreads above are:

Spread

BAA-AAA

AAA-Long

Long-Short

Original

0.445

0.539

0.328

Absolute

0.515

0.606

0.431

Recall the critical values for the L1 version of the Ljung-Box white noise test. Comparing them with our values here, we confirm we fail to reject the white noise hypothesis.

Innovations are not Gaussian, but quite close. See the quantile-quantile plots. Also, below are normality statistics.

Spread

BAA-AAA

AAA-Long

Long-Short

Skewness

0.557

0.683

-0.097

Kurtosis

0.594

0.635

1.338

Shapiro-Wilk p

1.3%

0.6%

4.3%

Jarque-Bera p

4.0%

1.0%

2.5%

PART 2:Modeling earnings growth (nominal/real) using these 3 bond spreads as regression factors, with innovations normalized by annual volatility. This model fits well, with IID but not quite Gaussian innovations.

Data: In addition to the data from PART 1, we have annual data 1927-2024: Denote December data for year t by Further, let be annual earnings 1928-2024 for S&P 90/500. These can be real (inflation-adjusted) or nominal (not inflation-adjusted). Then is log earnings growth from year to year

Model 1: We modeled it earlier as IID after dividing by volatility: But here, we model these normalized growth terms using regression versus these three spreads: Here, is a constant, is a vector, and are IID with mean zero.

Model 2: Alternatively, we can model Here we normalize residuals by volatility. Here, again are IID with mean zero, is a vector and are scalars. This is different from the first model, where we normalize growth terms but not spreads. We fit this model after dividing this equation by

Methodology: We analyze residuals for IID Gaussian, as in PART 1, using the five-point program.

Results: All four regressions (Models 1 and 2, nominal and real) have IID residuals (judging by ACF values and plots), which are close to normal (judging by the quantile-quantile plots) but unfortunately not quite normal (judging by normality tests, skewness, and kurtosis). See plots below for Model 1 = normalized spreads, Model 2 = original spreads.

For Model 1, the only significant coefficient with is for Long-Short, judging by Student T-test. For Model 2, this is AAA-Long. All other .

For Model 1, (nominal) and (real). For Model 2, for both nominal and real.

PART 3:We model S&P annual returns (total/price, nominal/real) normalized by S&P volatility using linear regression upon three spreads: BAA-AAA, AAA-Long, Long-Short, and earnings yield. Residuals are IID Gaussian.

Data: We have 1927-2024 S&P 90/500 index data:

end of year (last trading day close) level, 1927-2024;

This allows us to compute four versions of index returns We allow for following options: price (excluding dividends) and total (including dividends); nominal (not adjusted for inflation) and total (adjusted for inflation). Also, we can compute earnings yield This is the ratio of annual earnings this year to end-of-year index level. See the graph below. We have a big drop in 2008 since earnings drop there much faster than index.

As above, we also have four December daily average rates: BAA, AAA, Long and Short, for 1927-2024. This allows us to compute these three spreads. We studied these spreads and used these to model earnings yield before. Denote their vector as

Model 1: Consider the linear regression Here, are IID with mean zero. Next, are scalars and

Model 2: Remove earnings yield from this regression and fit it again:

Methodology: Divide these equations by volatility and fit regressions using ordinary least squares. Use the 5-point program from Part 1 of this post to analyze residuals.

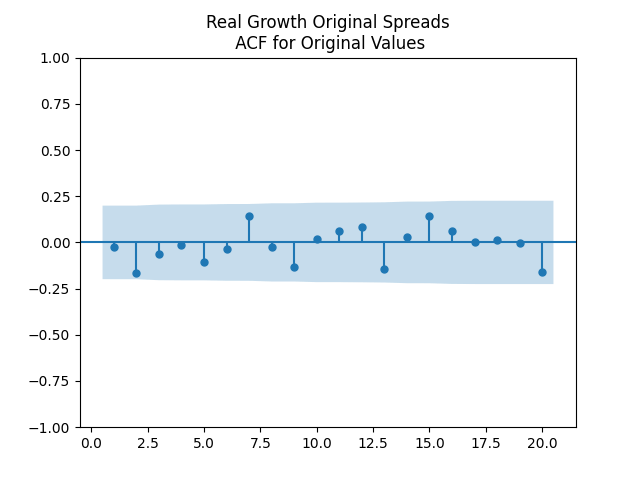

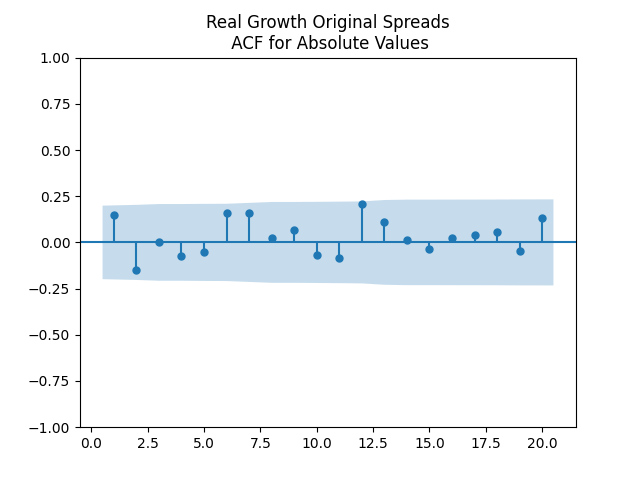

Results: Autocorrelation Function (ACF) plots for and for confirm IID. However, we still have this strange high value in lag 4, similar to the previous blog post. Computation of L1 norm for first 5 lags of ACF for and for also confirm IID.

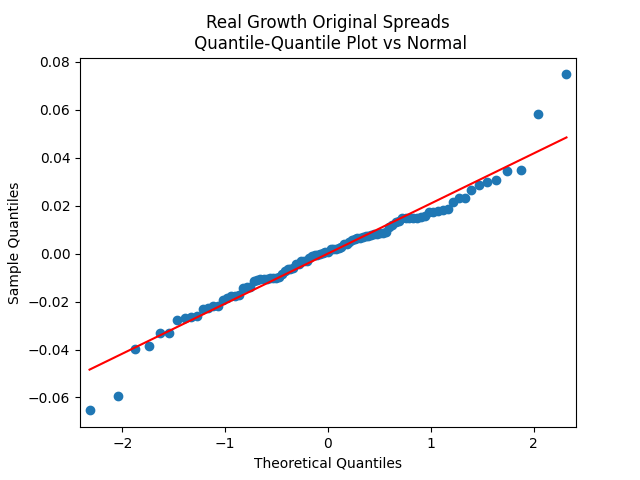

Also, Shapiro-Wilk and Jarque-Bera tests show normality. All

Coefficients for spreads are not significantly different from zero, judging by the Student T-test, for each of four types of returns. But removing these coefficients greatly reduces We also fail to reject Judging by the value for Student T-test, these spreads are BAA-AAA, AAA-Long, Long-Short in decreasing order of importance. I think it is best to use the full version of this regression.

Conclusion: The overall model for the following quantities:

end-of-year bond spreads BAA-AAA, AAA-Long, Long-Short:

annual S&P 500 earnings

end-of-year S&P 500 level

annual realized S&P 500 volatility

annual total S&P 500 returns

Here are independent identically distributed with mean zero, but not Gaussian.

This research is continued in the post where we consider trailing averaged annual earnings, with a window up to 10 years.

Bond spread BAA-10YTR (Moody’s BAA rate minus 10-year Treasury rate)

Also, we add annual realized volatility which we add both additively to the linear regression, as a factor, and multiplicatively, to the innovations (residuals). We have the following model:

Summary of results: Instead of giving large tables, we simply provide a short summary and refer an interested reader to the Python code.

Regression residuals pass Shapiro-Wilk and Jarque-Bera normality test with flying colors. This matches quantile-quantile plots versus the Gaussian distribution.

The autocorrelation function plots for and for show that white noise conjecture is reasonable. Although, similarly to this post, we have strange large value at lag 4.

Applying L1 norm for the autocorrelation function and comparing with this simulation, we get values which lie between 0.4 and 0.5 for and between 0.6 and 0.7 for , which are within the 99% interval. Thus we fail to reject the white noise hypothesis.

Regression factors have large p-values according to the Student T-test. Thus we fail to reject the hypothesis that or or We did not test the joint hypothesis when all these three parameters are zero. But we reject because

Point estimates in all four cases are

A modification: Instead of earnings yield (which is always positive) take its logarithm: Results are almost the same as described above. Although for nominal total returns the L1 norm for is 0.706.

This is Monte Carlo simulation to find critical values of the L1 version of the Ljung-Box test. I was too lazy to look for the official L2 norm for ACF using the classic Ljung-Box test. I simply decided to simulate.

Consider a sample of 100 standard normal random variables

Compute the empirical autocorrelation function with lag which is an empirical correlation of and Do this for Then compute the L1 norm

Do the same for instead of

Finally, compute empirical mean and the empirical centered moments of order

Then the empirical skewness is and the empirical kurtosis is

We create 1 million simulations of this 100 i.i.d. Gaussian variables. We compute values corresponding to 95% and 99% percentiles of simulated data for 100 IID standard normal (a million simulations). We get the following table (skewness is taken with absolute value, disregarding the sign). See https://github.com/asarantsev/4rates

Function

95% percentile

99% percentile

Skewness

0.47

0.63

Excess Kurtosis (normal = 0)

0.76

1.38

L1 norm for ACF (both), 5 lags

0.63

0.76

Added on June 5, 2025: If we make 100 000 simulation of only 50 i.i.d. Gaussian variables (instead of 100, simply changing this number in the code), we have:

Function

95 percentile

99 percentile

Skewness

0.643

0.878

Excess Kurtosis (normal = 0)

0.977

1.859

L1 norm for ACF (5 lags), original

0.882

1.079

L1 norm for ACF (5 lags), absolute

0.877

1.073

We also simulate skew normal variables with skewness parameter 3. Obviously, the true skewness and excess kurtosis will not be equal to zero any more. But we can still take percentiles for the empirical kurtosis and for these L1 norms for ACF, applied to original values of these variables and to absolute values of these variables. We take only 10000 simulations. For sample of size 100/50, we get:

in a given number of

years. How much do I invest now, if I contribute only at the initial time?

per year during

years. Here and below, we can have

so we can use this money infinitely long. How much to invest now?

(price/total, nominal/real)

(price/total, nominal/real)

explained in

explained in  are not significant: Student T-test has p-values greater than 5%. The most significant (having the smallest p-values) is

are not significant: Student T-test has p-values greater than 5%. The most significant (having the smallest p-values) is  corresponding to the BAA-AAA spread. Exceptions: for Total Nominal Returns,

corresponding to the BAA-AAA spread. Exceptions: for Total Nominal Returns,  The coefficient

The coefficient  is very statistically significant with

is very statistically significant with  See below the graphs for simulated volatility and spreads.

See below the graphs for simulated volatility and spreads.

, and the quantile-quantile plot for

, and the quantile-quantile plot for

are spreads: BAA-AAA, AAA-Long, Long-Short, and cyclically adjusted earnings yield (average earnings over the last few years divided by end-of-year stock index. As usual,

are spreads: BAA-AAA, AAA-Long, Long-Short, and cyclically adjusted earnings yield (average earnings over the last few years divided by end-of-year stock index. As usual,  is annual realized inflation, and

is annual realized inflation, and  of this regression and compare this with cut version without any spreads. Finally, we consider the Student T-test for each coefficient.

of this regression and compare this with cut version without any spreads. Finally, we consider the Student T-test for each coefficient. are NOT significant. The most significant (having smallest p-value) among spreads is usually BAA-AAA. Adjusted

are NOT significant. The most significant (having smallest p-value) among spreads is usually BAA-AAA. Adjusted

where

where  is earnings growth terms. Let

is earnings growth terms. Let  be the new valuation measure. Then we model

be the new valuation measure. Then we model  as an autoregression of order 1:

as an autoregression of order 1:  Earlier we found that it is better to model

Earlier we found that it is better to model  where

where  is the annual volatility, and

is the annual volatility, and

can be rejected: the Student T-test gives very low p-values. This shows us that we might want to use the extended regression. But we keep the original regression with volatility but without the intercept, to make it simple. Extending it will require more research.

can be rejected: the Student T-test gives very low p-values. This shows us that we might want to use the extended regression. But we keep the original regression with volatility but without the intercept, to make it simple. Extending it will require more research.

values for Student T-test. Are innovations Gaussian or independent identically distributed? If the regression fit is not good, according to these metrics, we can prohibit the user to apply these choices for averaging windows.

values for Student T-test. Are innovations Gaussian or independent identically distributed? If the regression fit is not good, according to these metrics, we can prohibit the user to apply these choices for averaging windows.  Presumably we need to adapt the autoregression simulation for that. Also, analyze the innovations and see whether this is a good fit. If not, again prohibit the user to apply these options.

Presumably we need to adapt the autoregression simulation for that. Also, analyze the innovations and see whether this is a good fit. If not, again prohibit the user to apply these options.

Here, we instead model these as regression

Here, we instead model these as regression

be the 10-year trailing averaged annual real earnings. Let

be the 10-year trailing averaged annual real earnings. Let  be the log growth terms. We compute these for

be the log growth terms. We compute these for  Also, let

Also, let  is its long-term average. We model the valuation measure

is its long-term average. We model the valuation measure

The Student test for

The Student test for  gives us

gives us  so the model is not a random walk, but rather mean-reverting.

so the model is not a random walk, but rather mean-reverting.

where

where

and repeat the analysis. See the plot of the valuation measure below. It looks very similar to the one above.

and repeat the analysis. See the plot of the valuation measure below. It looks very similar to the one above.

for

for  Next, the Shapiro-Wilk and Jarque-Bera tests for new innovations

Next, the Shapiro-Wilk and Jarque-Bera tests for new innovations  The autocorrelation function plots for

The autocorrelation function plots for  instead of

instead of  Further, the quantile-quantile plot for

Further, the quantile-quantile plot for

for original regression and

for original regression and  for new regression. We leave it to the reader which one to use. But we intend to use the original regression for future financial simulator.

for new regression. We leave it to the reader which one to use. But we intend to use the original regression for future financial simulator.

where

where  and

and  is a 3\times 3 matrix, and

is a 3\times 3 matrix, and  where

where  are IID with mean zero. We already fit it in the previous post, so we do not discuss it here.

are IID with mean zero. We already fit it in the previous post, so we do not discuss it here. by each of three scalar equations. We divide this equation by the volatility and then use ordinary least squares method. Then we test each of the three components

by each of three scalar equations. We divide this equation by the volatility and then use ordinary least squares method. Then we test each of the three components  of the innovation series for IID Gaussian using the usual procedure:

of the innovation series for IID Gaussian using the usual procedure:

only for diagonal values of B, its third row, and c. It is important to verify that eigenvalues of B are strictly less than 1. Then the time series model above is stable and ergodic in the long-run, see my manuscript

only for diagonal values of B, its third row, and c. It is important to verify that eigenvalues of B are strictly less than 1. Then the time series model above is stable and ergodic in the long-run, see my manuscript

Further, let

Further, let  to year

to year

But here, we model these normalized growth terms using regression versus these three spreads:

But here, we model these normalized growth terms using regression versus these three spreads:  Here,

Here,  is a constant,

is a constant,  is a vector, and

is a vector, and  Here we normalize residuals by volatility. Here, again

Here we normalize residuals by volatility. Here, again  are scalars. This is different from the first model, where we normalize growth terms but not spreads. We fit this model after dividing this equation by

are scalars. This is different from the first model, where we normalize growth terms but not spreads. We fit this model after dividing this equation by

is for Long-Short, judging by Student T-test. For Model 2, this is AAA-Long. All other

is for Long-Short, judging by Student T-test. For Model 2, this is AAA-Long. All other  .

.  (nominal) and

(nominal) and  (real). For Model 2,

(real). For Model 2,  for both nominal and real.

for both nominal and real. We allow for following options: price (excluding dividends) and total (including dividends); nominal (not adjusted for inflation) and total (adjusted for inflation). Also, we can compute earnings yield

We allow for following options: price (excluding dividends) and total (including dividends); nominal (not adjusted for inflation) and total (adjusted for inflation). Also, we can compute earnings yield  This is the ratio of annual earnings this year to end-of-year index level. See the graph below. We have a big drop in 2008 since earnings drop there much faster than index.

This is the ratio of annual earnings this year to end-of-year index level. See the graph below. We have a big drop in 2008 since earnings drop there much faster than index.

Here,

Here,  are scalars and

are scalars and

Then

Then

We also fail to reject

We also fail to reject  Judging by the

Judging by the

are independent identically distributed with mean zero, but not Gaussian.

are independent identically distributed with mean zero, but not Gaussian.

show that white noise conjecture is reasonable. Although, similarly

show that white noise conjecture is reasonable. Although, similarly and between 0.6 and 0.7 for

and between 0.6 and 0.7 for  , which are within the 99% interval. Thus we fail to reject the white noise hypothesis.

, which are within the 99% interval. Thus we fail to reject the white noise hypothesis.  or

or  or

or  We did not test the joint hypothesis when all these three parameters are zero. But we reject

We did not test the joint hypothesis when all these three parameters are zero. But we reject  because

because

which is an empirical correlation of

which is an empirical correlation of  and

and  Do this for

Do this for  Then compute the L1 norm

Then compute the L1 norm

instead of

instead of  and the empirical centered moments of order

and the empirical centered moments of order

and the empirical kurtosis is

and the empirical kurtosis is