Dear readers, after a long break, I am back. I updated the annual volatility and other data for S&P 500 for the year 2025. The data are available here.

- Data Updates

- New Graphs

- Total Returns

- Volatility Autoregression

- Price Returns

- BAA Bond Rates

- Dividend Growth

- Conclusion

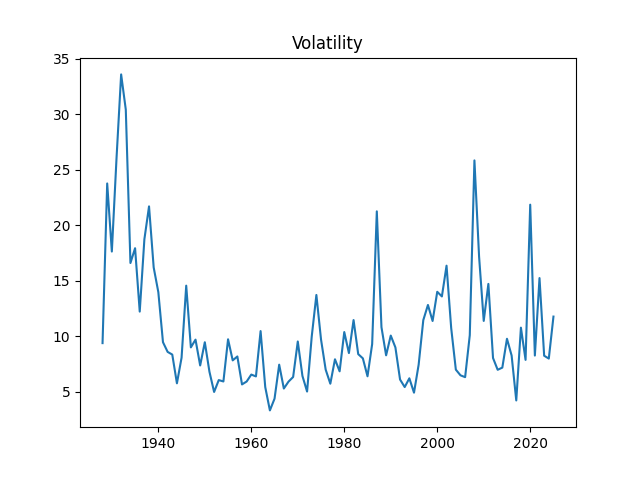

1. Data Updates. Annual volatility is computed as the empirical standard deviation of daily log changes multiplied by 1000 (for normalizing). The end-of-year price for S&P 500 in 2025 is also updated. We also add S&P 500 dividends for 2025. Now we have data on volatility for 1928-2025, on dividends for 1927-2025, and end-of-year level of S&P 500 for 1927-2025 too.

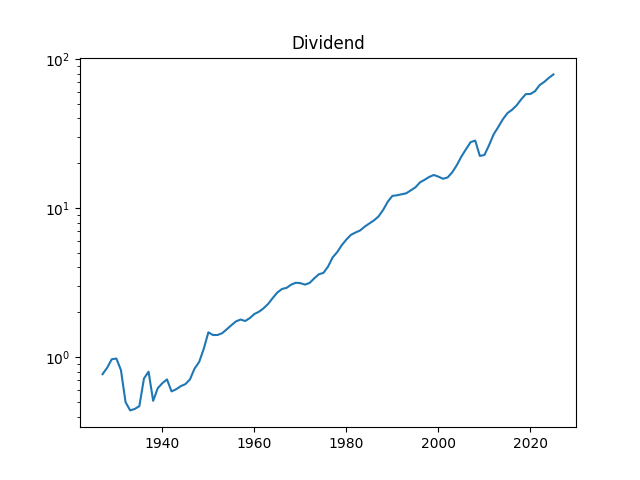

We added the dividend data for 1927 as well, to increase the number of data points. This is fine, since S&P 90 (a predecessor for S&P 500) was created in 1926, and the data is taken from Robert Shiller’s data library.

The volatility for 2025 is 11.77. This is higher than the long-term average 10.51, or the 2024 volatility, which is 7.98. See the original post with computations of Angel Piotrowski for 1928-2023 and its previous update for 2024.

Dividends for 2025 are 78.92, which is significantly higher than dividends for 2024, which are 74.83.

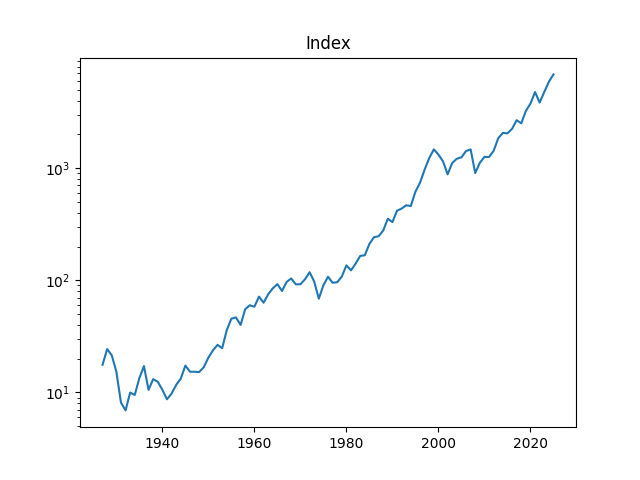

The S&P 500 increased a lot in 2025: End-of-year 2024 level is 5881.63, but end-of-year 2025 level is 6845.5.

We could not yet provide earnings for 2025, since we have earnings for 2025 Quarter 4 reported only on 2026 Quarter 1, which is still ongoing. We will provide them as soon as we can.

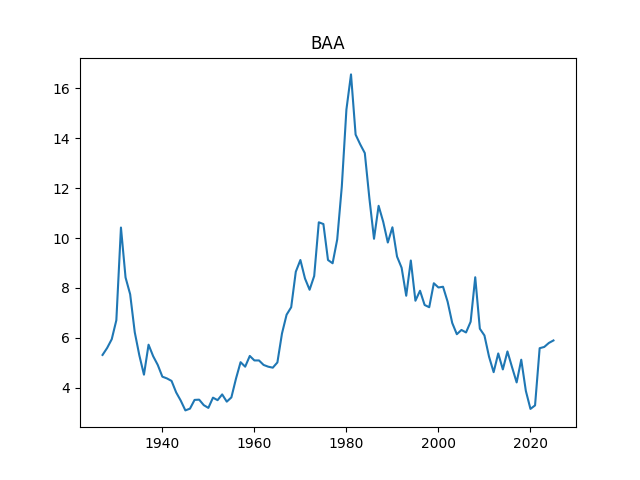

Finally, we added the BAA rate: December 2025 daily average. The BAA are lowest-rated investment-grade corporate bonds. The rate in December 2025 is 5.9, slightly higher than 5.8 for December 2024.

2. New Graphs. We graph the index, dividend, rates, and volatility.

Above, logarithmic plots of index levels and dividends for 1927-2025. Below, the annual volatility and December BAA rate.

The data are published on my web page: We created a new tab named Financial Data Library on my web page. Let us now apply

Let us replicate this post: Make stock returns IID Gaussian.

We have the following notation:

the S&P level at end-of-year

the dividend of S&P in year

December daily average BAA rate during year

annual realized volatility for the S&P for year

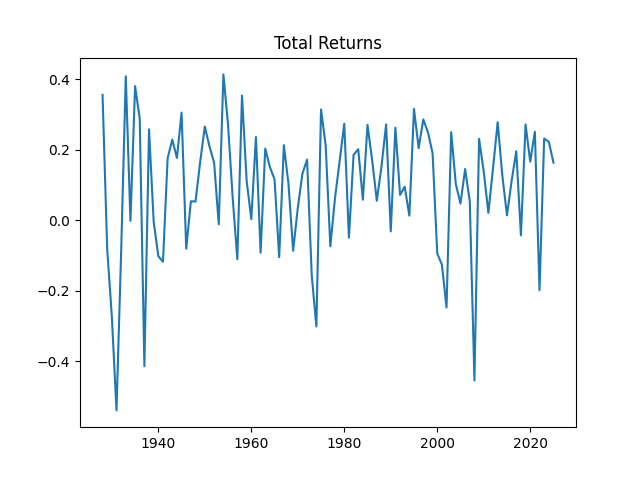

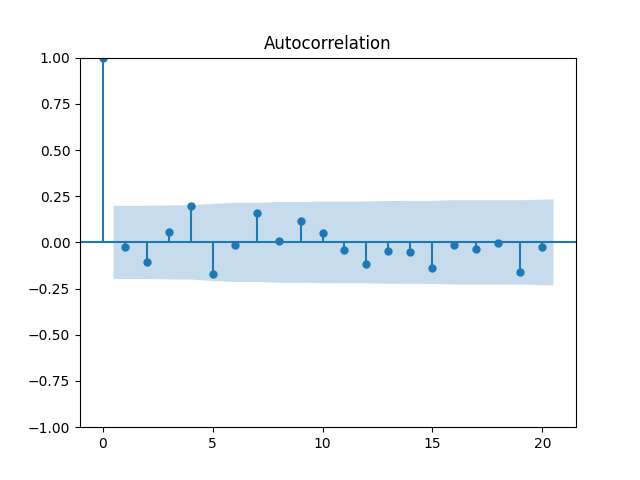

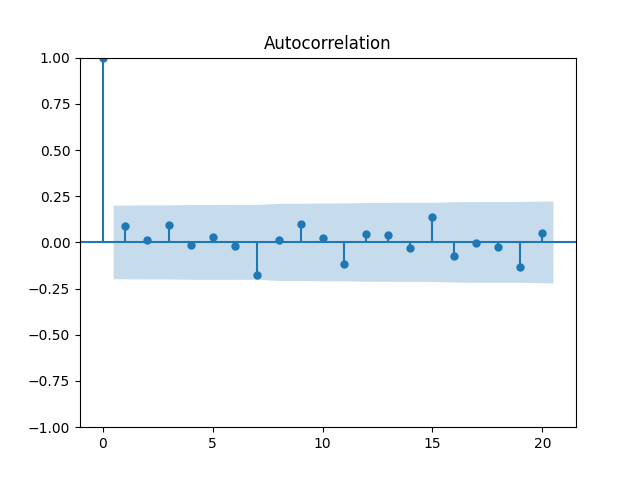

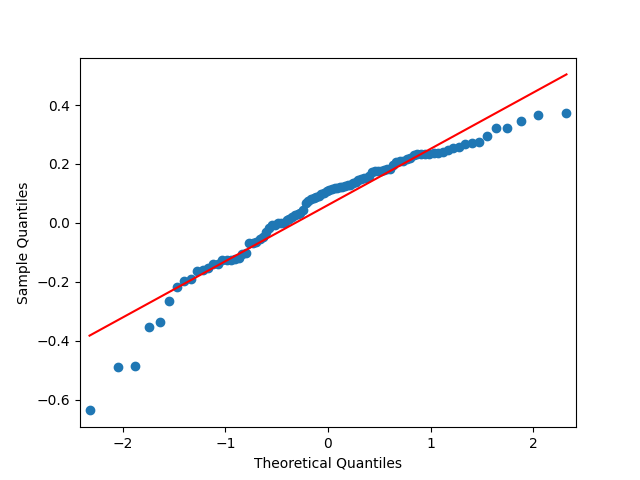

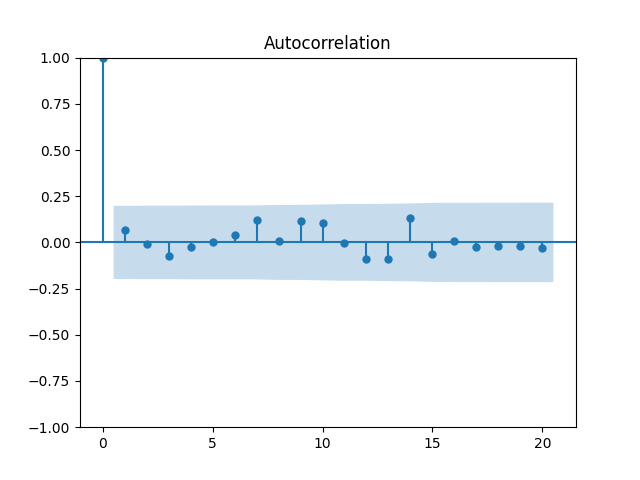

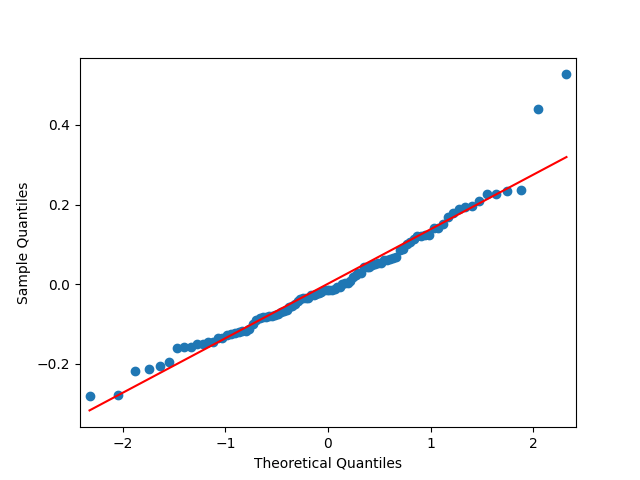

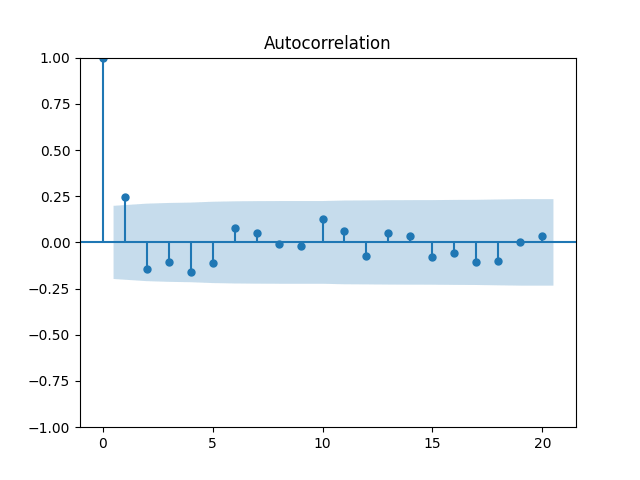

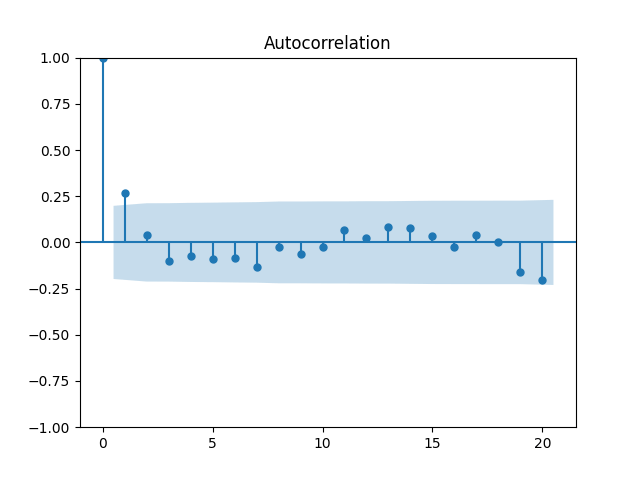

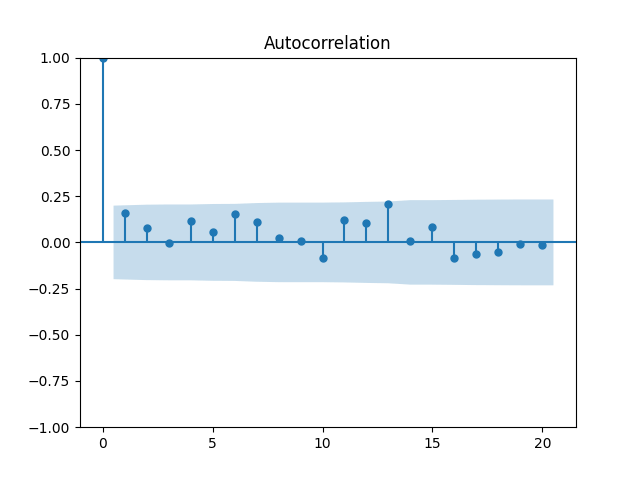

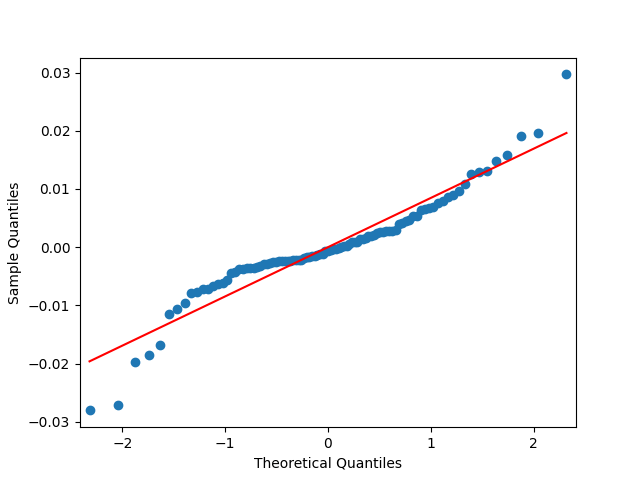

3. Total Returns. We continue this blog post. Compute total nominal geometric returns for the S&P 500:

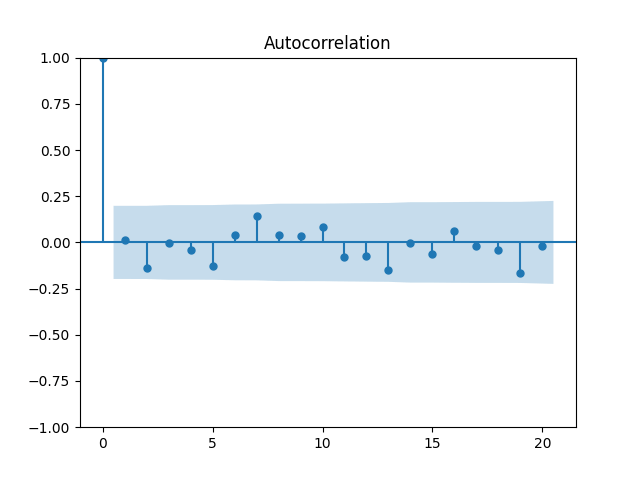

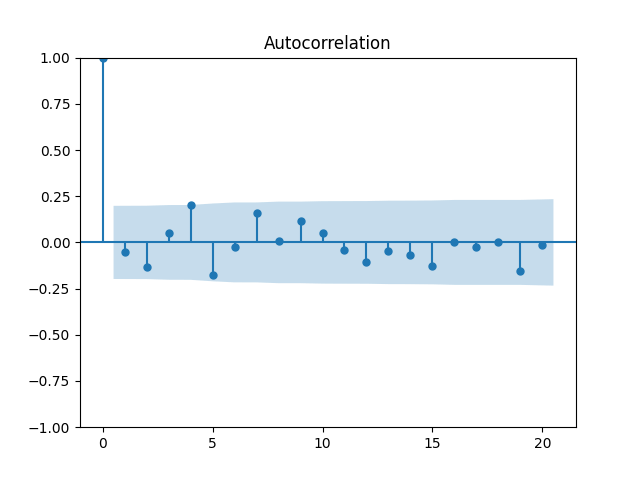

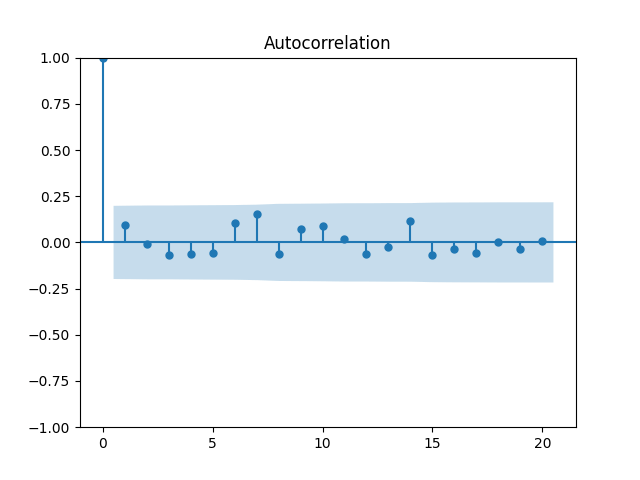

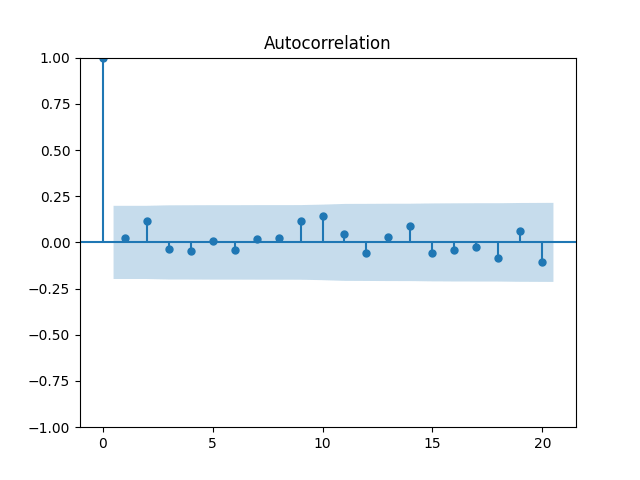

Now plot the autocorrelation function for these total returns

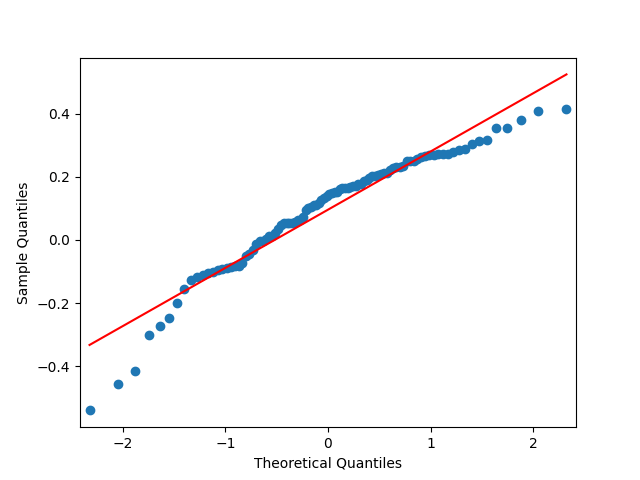

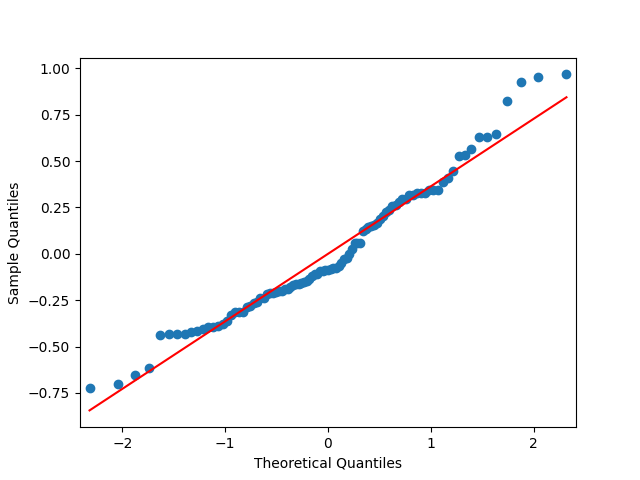

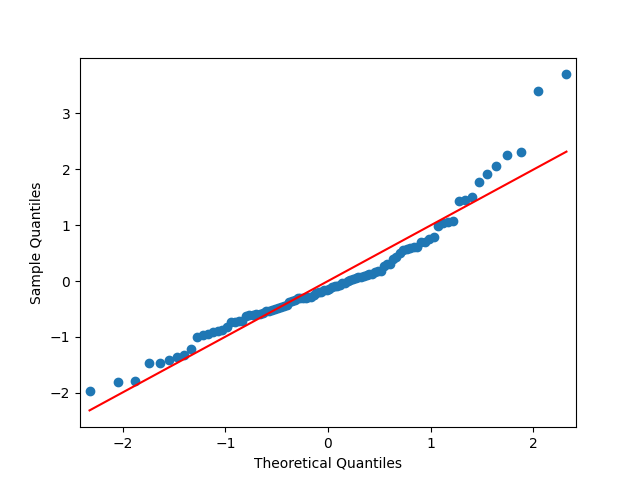

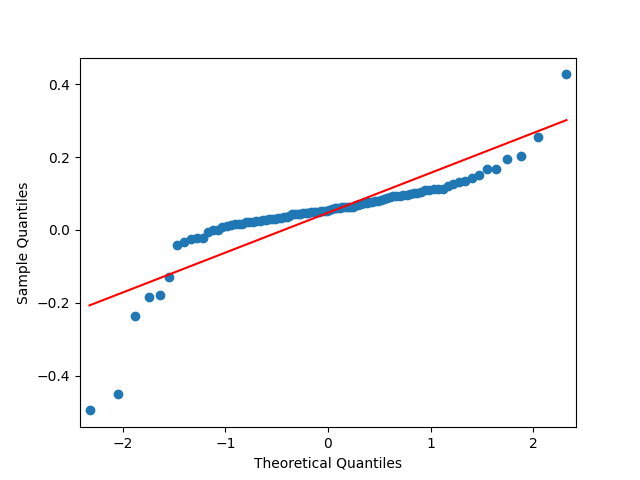

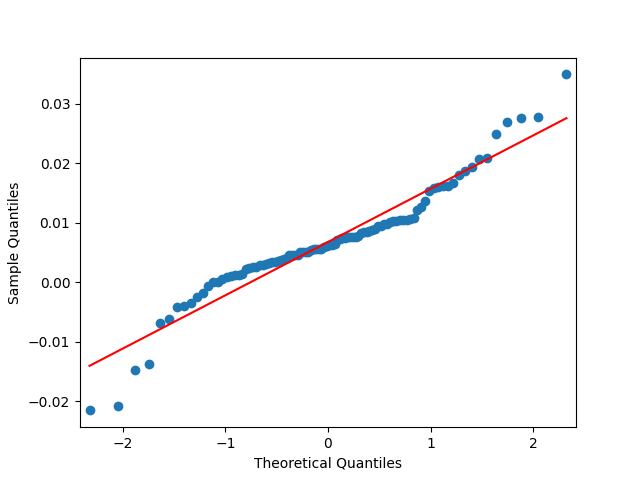

The quantile-quantile plot of these returns is shown as well. We see that the returns are not Gaussian. This is consistent with the normality testing. Shapiro-Wilk and Jarque-Bera tests give us

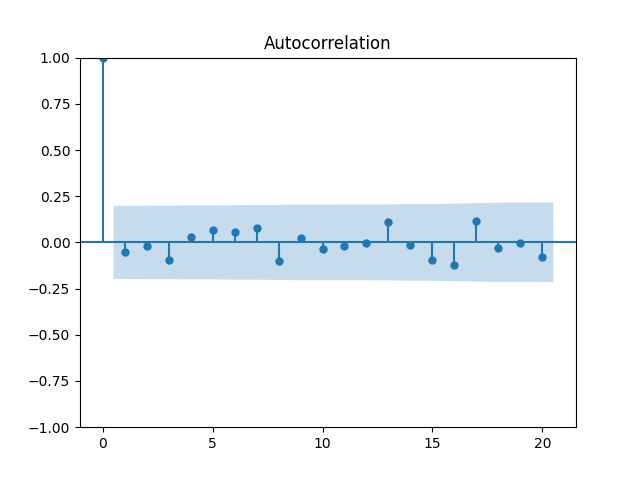

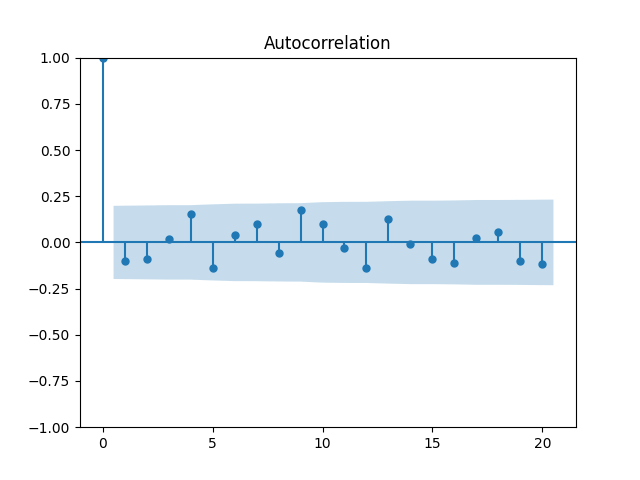

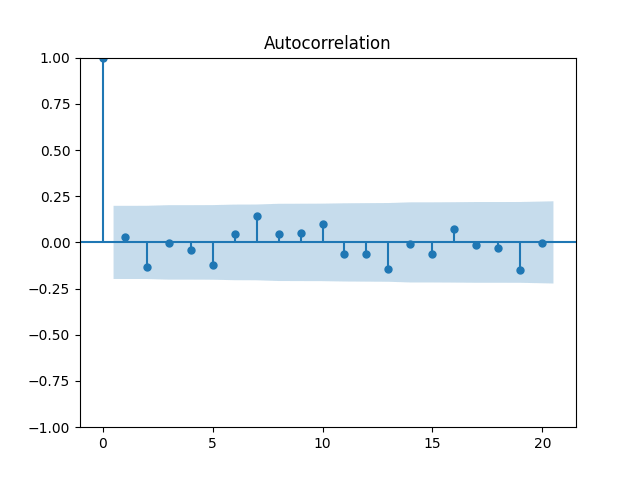

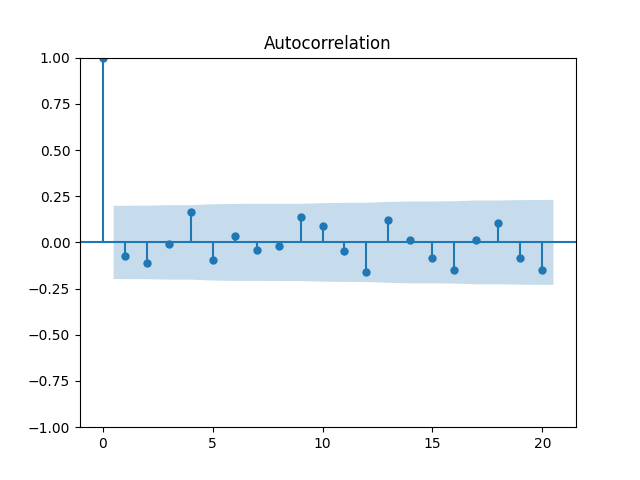

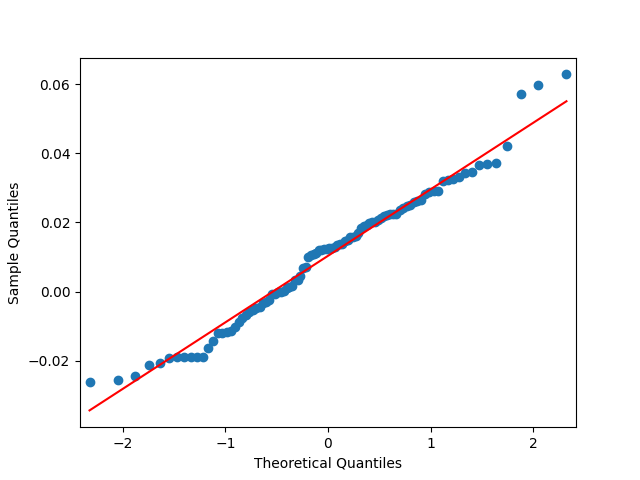

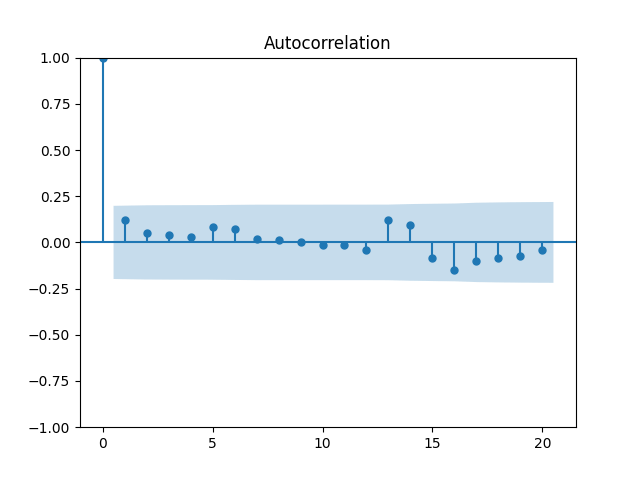

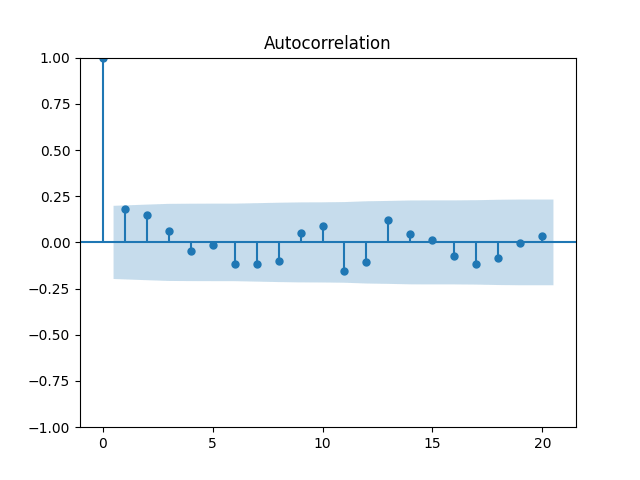

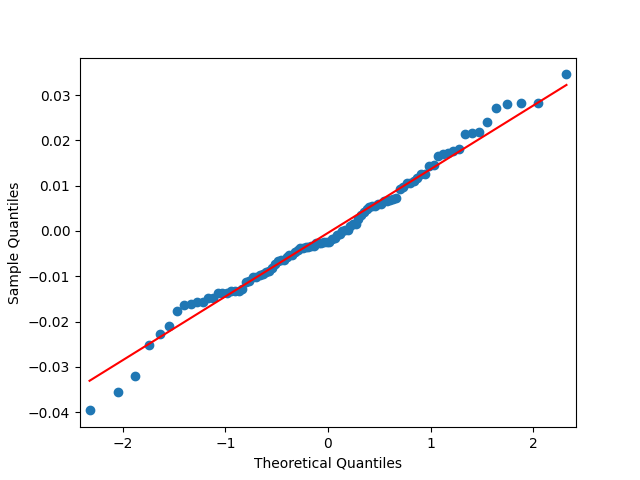

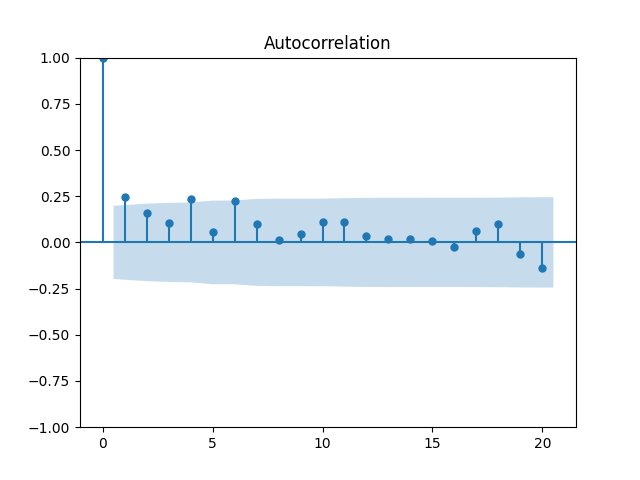

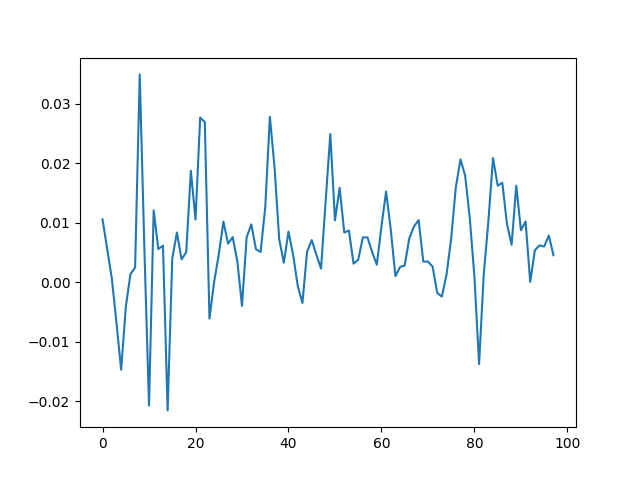

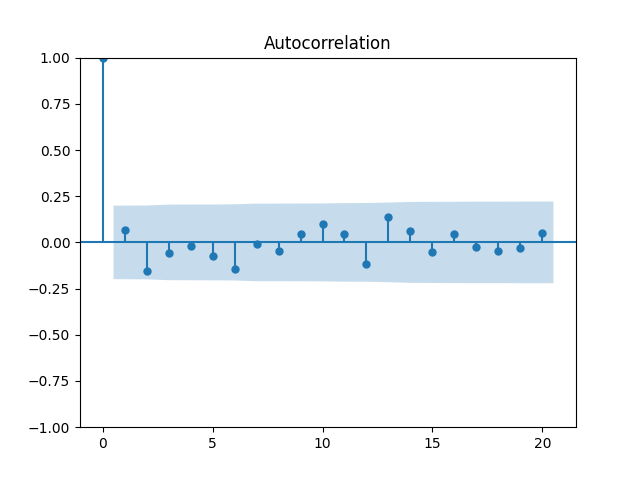

What if we do divide these total returns by annual volatility? We get

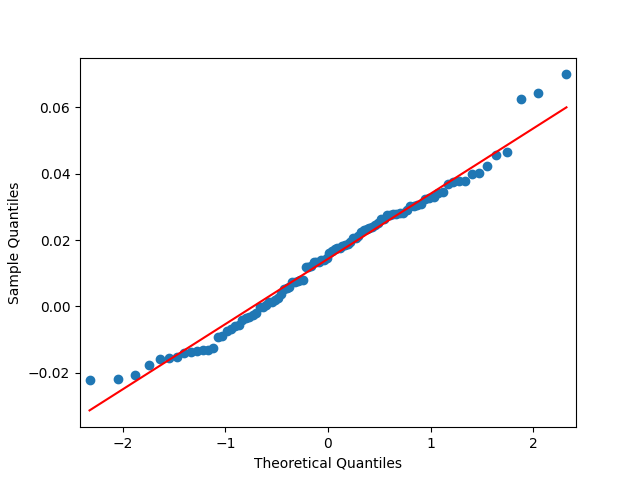

These are still consistent with white noise, although, in my view, the autocorrelation function values are greater. But the quantile-quantile plot versus the normal distribution is below. We get

4. Volatility Autoregression. We continue this blog post. Let us now fit the auto-regression model for logarithm of volatility:

We fit

This is consistent with the assumption that

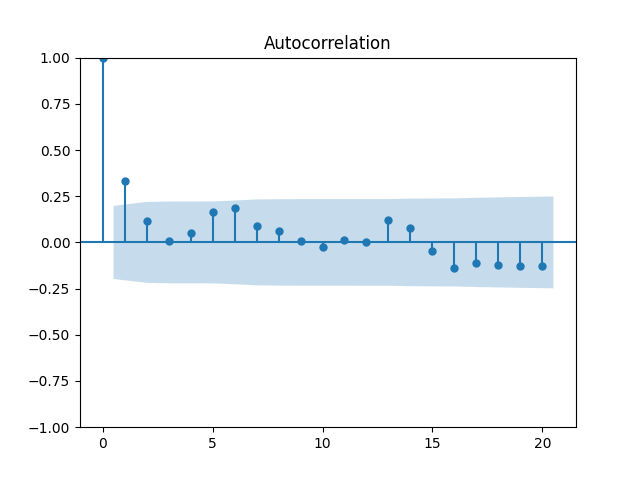

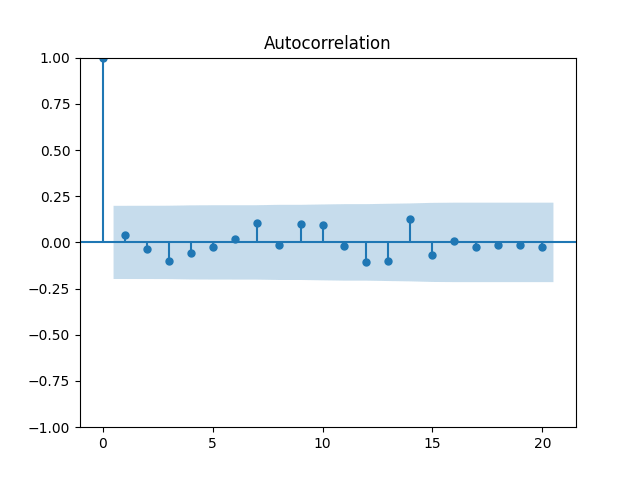

5. Price Returns. These are computed as

Quite close to independent identically distributed! Next, the quantile-quantile plot versus the Gaussian distribution: This shows price returns are not Gaussian, similarly to total returns. This is confirmed by familiar Shapiro-Wilk and Jarque-Bera tests

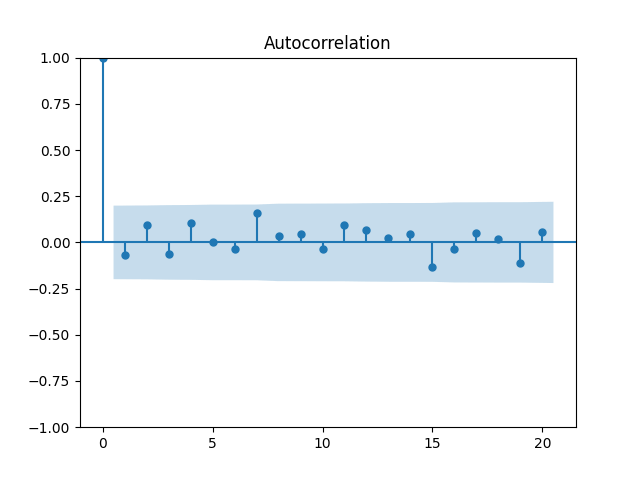

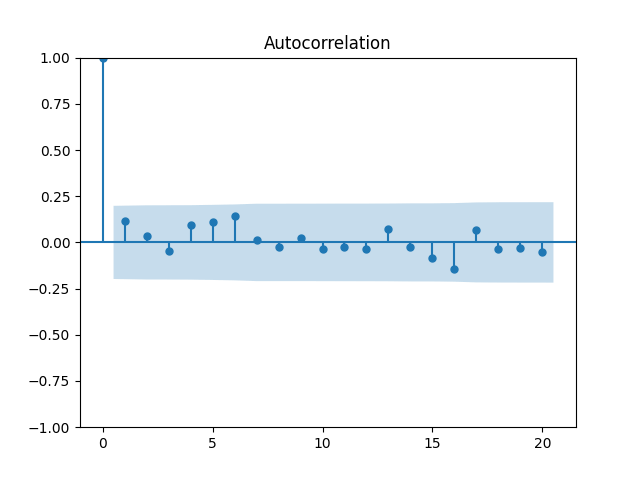

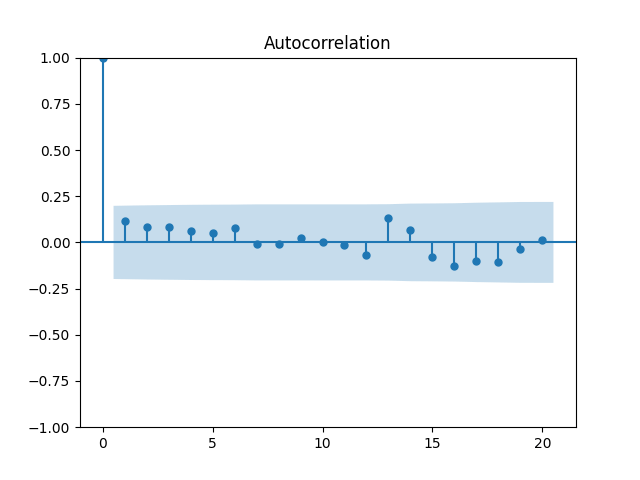

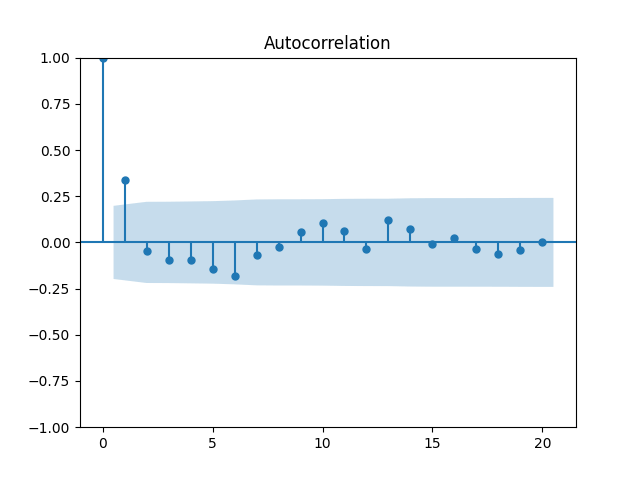

Let us divide price returns by volatility. Below we plot the autocorrelation function of

The Shapiro-Wilk and Jarque-Bera tests give us

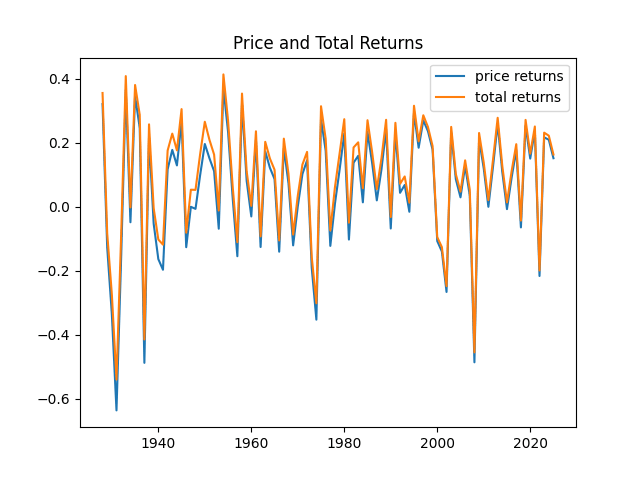

Finally, let us plot price and total returns together. We see that, of course, total returns are greater than price returns.

6. BAA Bond Rates. Continue this blog. We also fit a simple autoregression:

We get:

Both p-values for normality tests of innovations

Instead, like for the volatility, let us take the logarithm:

We get

Let us modify this to try a random walk model:

Next, the quantile-quantile plot versus the normal distribution is much closer to the straight line than before for other models of the BAA rate. This is confirmed that the Shapiro-Wilk and Jarque-Bera tests give us

Next, try to make these independent identically distributed but non-Gaussian terms Gaussian. We do the same as in sections 1 and 3: Divide the log rate change by volatility. We get

The quantile-quantile plot below shows these are Gaussian terms, and the same is shown by the Shapiro-Wilk and Jarque-Bera tests with

7. Dividend Growth is computed as

Define

See the plot of the dividend growth below. It is quite volatile but not as much as the stock returns. But we clearly see the persistence: It makes sense to model dividend growth or its normalized version as the simple autoregression. This is different from annual earnings growth, where dividing by volatility makes it independent identically distributed, see this blog post.

Let us try the simple autoregression for normalized annual dividend growth

We have

Here we have independent identically distributed but not Gaussian residuals

8. Conclusion. Here, we found all time series Markov models for dividends, price and total returns, volatility, and the BAA rates. In the next post, we will discuss updates for the valuation measure based on one-year dividends instead of trailing 10-year earnings, and regression modeling using rate change and duration, continuing this post and this post.

Leave a comment