See the GiHub repository https://github.com/asarantsev/growth-spread

Continuing research of Ian Anderson, we model

- Model 0:

- Model 1:

- Model 2:

- Model 3:

For each regression, we compute both nominal (not inflation-adjusted) and real (inflation-adjusted) earnings growth. Thus we have 6 models. We compute autocorrelation function plots for each

| Series | Skewness (Normal 0) | Kurtosis (Normal 0) | Shapiro-Wilk  | Jarque-Bera |  | p-value for Student test |

Nominal  | 0.479 | 2.158 | 0.3% | 0.0% | 7.2% | 32% (volatility) |

Real  | 0.459 | 1.893 | 0.7% | 0.0% | 4.9% | 24% (volatility) |

Nominal  | -0.114 | 2.105 | 1.3% | 0.0% | 4% | 5.2% (BAA-AAA) and 6.9% (BAA-10YTR) |

Real  | -0.136 | 1.861 | 2.8% | 0.1% | 5.2% | 5.2% (BAA-AAA) and 6.9% (BAA-10YTR) |

Nominal  | 0.163 | 2.226 | 0.6% | 0.0% | 23.6% | 3.4% (BAA-AAA) and 1.4% (BAA-10YTR) |

| Real | 0.137 | 2.039 | 1.0% | 0.0% | 15.4% | 1.4% (BAA-AAA) and 0.7% (BAA-10YTR) |

Nominal  | 0.256 | 2.068 | 1.2% | 0.0% | 13.3% | 27.4% (volatility) |

| Real | 0.227 | 1.86 | 1.9% | 0.1% | 12.4% | 23.8% (volatility) |

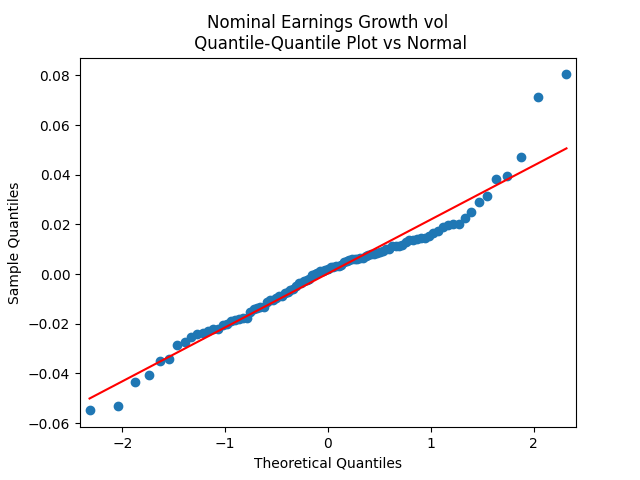

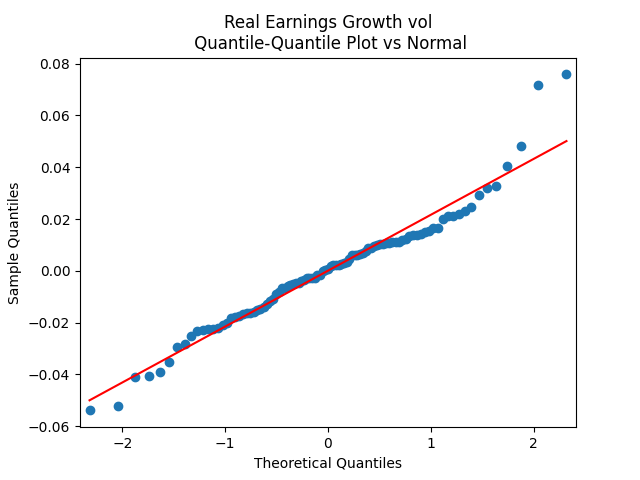

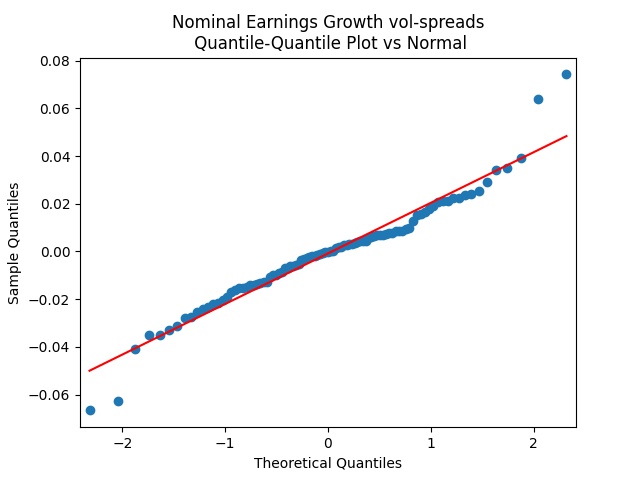

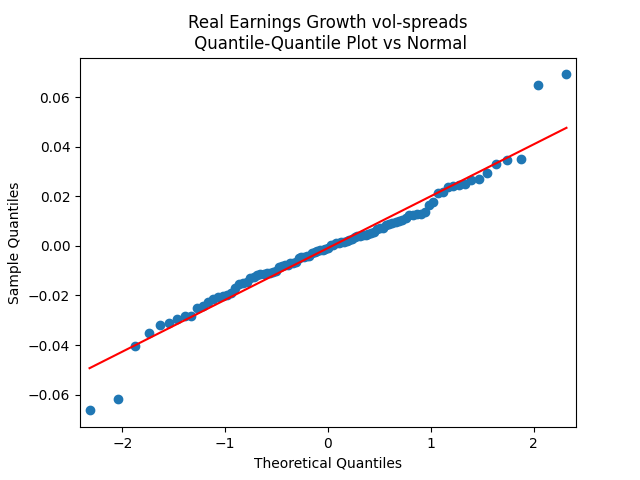

The quantile-quantile plot of earnings growth (nominal and real) versus the Gaussian distribution for Model 0:

The quantile-quantile plot of earnings growth (nominal and real) versus the Gaussian distribution for Model 1:

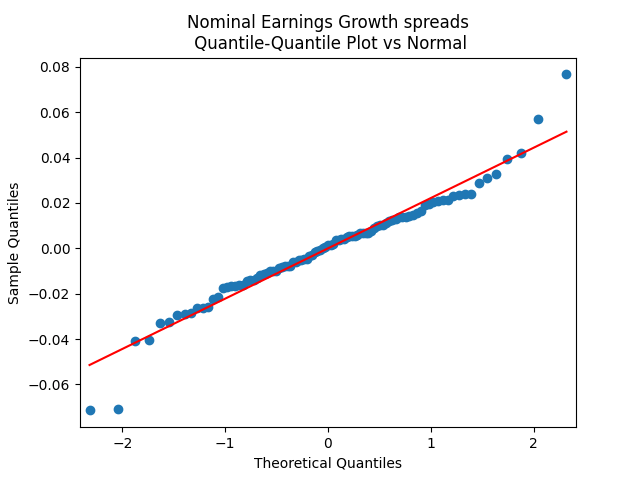

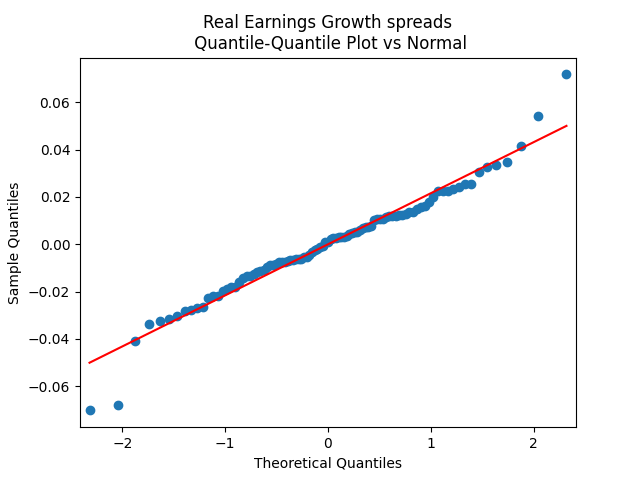

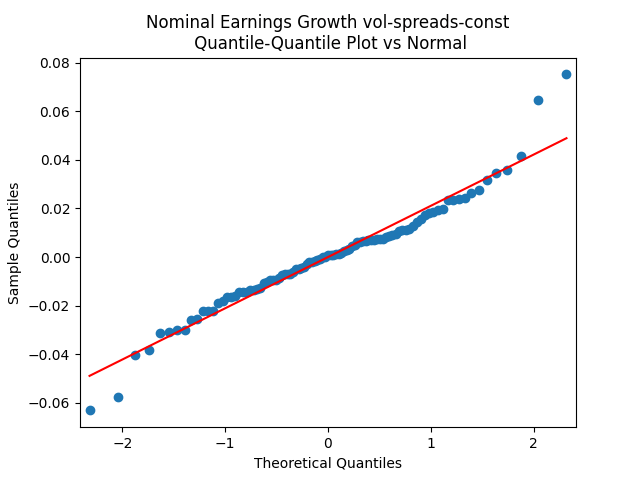

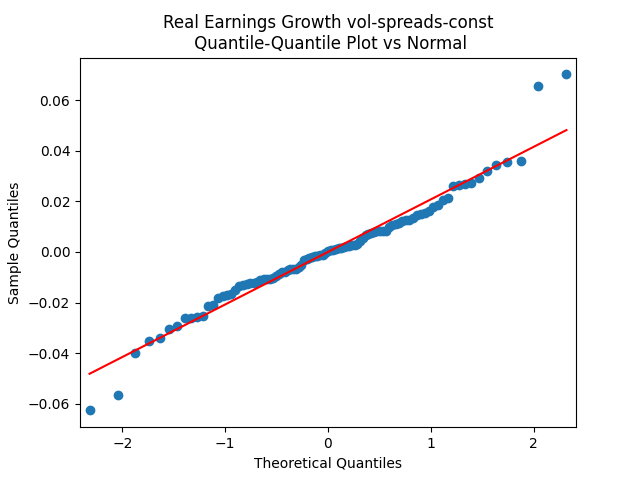

The quantile-quantile plot of earnings growth (nominal and real) versus the Gaussian distribution for Model 2:

The quantile-quantile plot of earnings growth (nominal and real) versus the Gaussian distribution for Model 3:

Conclusion: Unfortunately, residuals are independent identically distributed but not Gaussian, for each of the four models. Still, we need to pick one. Let us pick Model 2: Volatility is not significant, as shown by the Student test. Although it is not quite applicable, since residuals are not Gaussian! Let us write this equation after multiplication by the volatility:

Leave a comment